Alphabet’s Q1 2025 Earnings Report Scheduled for April 24

Alphabet (GOOGL) is scheduled to report its first-quarter 2025 results on April 24.

Projected Earnings and Revenue Growth

The Zacks Consensus Estimate for earnings for the first quarter of 2025 stands at $2.01 per share. This represents a minor decrease of one penny from estimates made 30 days prior, but it still indicates a year-over-year growth of 6.35%.

In terms of revenue, the consensus suggests that fourth-quarter earnings will reach $75.53 billion, reflecting a substantial 111.75% increase over the same quarter last year.

Strong Earnings Surprise Record

Alphabet has shown a notable track record of earnings surprises. Over the last four quarters, GOOGL’s results have consistently beaten the Zacks Consensus Estimate, boasting an average surprise of 11.57%. (Check the latest EPS estimates and surprises on Zacks earnings Calendar.)

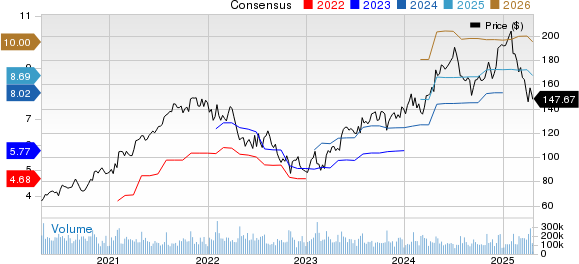

Alphabet Inc. Price and Consensus

Alphabet Inc. price-consensus-chart | Alphabet Inc. Quote

Analyzing the Factors for Alphabet’s Upcoming Quarter

The upcoming quarterly results for Alphabet are anticipated to benefit from robust performance in both search and cloud services. The company has notably expanded its capabilities in Generative AI (Gen AI), recognizing the growing demand for Large Language Models (LLMs) through its Gemini platform. In 2024, usage of Vertex surged by 20 times, and this trend is expected to continue in the forthcoming quarter.

Moreover, the integration of Gen AI into Google Search has enhanced user experiences, with new features like multi-search and visual exploration continuously improving search results. The AI-powered Circle to Search is now available on over 150 million Android devices, being used for shopping, text translation, and learning. This feature is particularly popular among younger users, contributing positively to search activity.

In the competitive cloud computing arena, Alphabet has maintained its position as the third-largest provider, following Amazon’s AMZN AWS and Microsoft’s MSFT Azure. The growing adoption of the Google Cloud Platform and Google Workspace is expected to support revenue growth within this segment.

Nonetheless, GOOGL is facing constraints related to capacity. Without new capacity coming online until 2025, variability in cloud revenues remains a concern, likely impacting Alphabet’s cloud earnings this quarter.

Stock Performance Analysis: GOOGL’s Year-to-Date Decline

Year to date, Alphabet’s shares have diminished by 22.1%. This performance is slightly better than the broader Zacks Internet Services industry and the Zacks Computer & Technology sector, which have declined 18.6% and 17.2%, respectively.

GOOGL Stock Performance

Image Source: Zacks Investment Research

Currently, GOOGL shares are considered overvalued, as indicated by a Value Score of C. The stock is trading at a forward 12-month Price/Sales ratio of 5.27X, higher than the industry average of 4.47X.

Current Price/Sales Ratio (F12M)

Image Source: Zacks Investment Research

From a technical perspective, GOOGL stock is displaying a bearish trend, currently trading below both its 50-day and 200-day moving averages.

Graph of GOOGL Trading Trends

Image Source: Zacks Investment Research

Future Prospects: Will AI and Wiz Elevate GOOGL?

Alphabet’s ongoing initiatives with AI and the anticipated integration of Wiz are positioned to enhance overall growth. The GOOGL-Wiz partnership aims to deliver security solutions across multi-cloud environments, addressing emerging AI threats and enhancing response strategies for enterprises. Wiz boasts a strong customer base, utilizing its security platform among giants like Amazon, Microsoft, and Oracle (ORCL).

The inclusion of Wiz into Google Cloud is expected to bolster its competitiveness against AWS and Azure. According to Statista, Amazon held a 30% share of the global cloud infrastructure market in Q4 2024, followed by Microsoft’s Azure with 21% and Google Cloud at 12%.

Additionally, GOOGL has announced an expansion in collaboration with Oracle. This includes an industry-first partner program and the upcoming support for Oracle Base Database Service on Google Cloud, now compatible with Oracle Exadata X11M, along with new services for U.S. Government Cloud clients. To meet the surge in customer demand, Oracle and Alphabet plan to expand their offerings into 11 new regions in the next 12 months.

Is Now the Time to Buy, Sell, or Hold GOOGL Stock?

Alphabet’s expanding Gen AI capabilities present potential growth opportunities as the company retains a strong foothold in the search engine market. However, current valuation levels and intense competition in the cloud sector may pose risks for investors considering GOOGL shares.

Alphabet holds a Zacks Rank #3 (Hold), suggesting it might be prudent for investors to wait for a more favorable entry point before committing to GOOGL stock. For those interested, you can see Zacks’ comprehensive list of #1 Rank (Strong Buy) stocks available today.

Discover Top Stocks Poised for Growth

These handpicked stocks have been highlighted by Zacks experts as the top picks to potentially double in value during 2024. Past recommendations have shown significant returns, soaring as high as +673.0%.

Most stocks featured in this report are currently on Wall Street’s radar, presenting a strong investment opportunity. See these 5 potential home runs >>

For the latest stock recommendations from Zacks Investment Research, download the 7 Best Stocks for the Next 30 Days by clicking here.

Companies mentioned include:

Amazon.com, Inc. (AMZN): Free Stock Analysis report

Microsoft Corporation (MSFT): Free Stock Analysis report

Oracle Corporation (ORCL): Free Stock Analysis report

Alphabet Inc. (GOOGL): Free Stock Analysis report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.