PayPal Set to Report Q1 2025 Earnings on April 29

PayPal (PYPL) is scheduled to report its earnings for the first quarter of 2025 on April 29. The company anticipates flat to low single-digit revenue growth on a currency-neutral basis for the upcoming quarter. Non-GAAP earnings are projected between $1.15 and $1.17 per share, indicating a year-over-year increase of 6 to 8%.

Revenue and Earnings Projections

The Zacks Consensus Estimate for first-quarter revenue is set at $7.83 billion, representing a 1.64% increase compared to the prior year’s figure. Meanwhile, the consensus estimate for earnings sits at $1.15 per share, down by one penny over the last month, suggesting a decline of 17.86% relative to the same quarter last year.

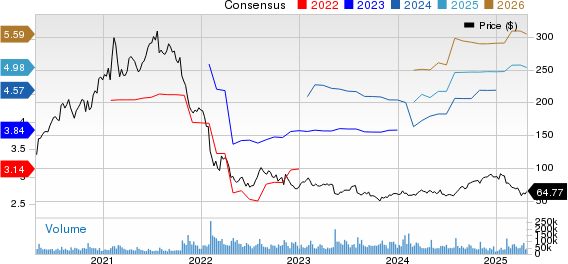

PayPal Holdings, Inc. Price and Consensus

PayPal Holdings, Inc. price-consensus-chart | PayPal Holdings, Inc. Quote

In the past four quarters, PayPal has consistently surpassed the Zacks Consensus Estimate, boasting an average surprise of 14.26%.

Expectations for Q1 Results

PayPal’s first-quarter performance is expected to demonstrate strength from its diverse portfolio. Notably, Fastlane improves the guest checkout experience, allowing users to complete purchases in just one click. Additionally, robust monetization efforts with Venmo are anticipated to contribute to Total Payments Volume during this reporting period.

The firm’s extensive partnerships with major companies such as Amazon (AMZN), Shopify (SHOP), Apple, Alphabet, and Meta Platforms (META) have significantly influenced its performance. Recent integrations, like adding PayPal and Venmo credit or debit cards to Apple Wallet, are also expected to yield positive results.

Furthermore, PayPal now acts as an additional processor for Shopify Payments in the U.S., streamlining operations for business owners. Collaborations with Amazon also allow PayPal Checkout to reach Small and Medium Businesses (SMBs). Integrations with Apple Pay and Google Pay enhance the Venmo debit card’s usability, driving consumer adoption.

PayPal remains a leading payment choice for both advertisers and consumers across the Meta Platforms apps. Moreover, services such as Hyperwallet for creators and developers, alongside Braintree for credit card processing at META, bolster PayPal’s market position.

In late 2024, PayPal introduced FX-as-a-service to automate currency conversion, already in use with Meta Platforms. The rollout of network tokens for automated billing is live with merchants including Instacart, Mint Mobile, and Poshmark. Such expansions are expected to enhance transaction margins financially. Recently launched initiatives like PayPal Everywhere increase the adoption of debit cards and open new consumer spending categories.

Stock Performance Comparison

Despite these positive developments, PayPal shares have declined 23.8% year-to-date, lagging behind the Zacks Business Service sector, which fell by 2.8%, and the Zacks Internet Software Industry’s dip of 0.8%.

PYPL Stock Performance

Image Source: Zacks Investment Research

The Value Score for PayPal indicates it is currently undervalued, with a rating of B. The forward 12-month Price/Sales ratio stands at 1.91x, below the industry average of 6.33x.

Price/Sales (P/S) Ratio

Image Source: Zacks Investment Research

Long-Term Growth Potential

PayPal’s robust portfolio continues to strengthen its relationships with merchants and consumers. The two-sided platform fosters direct connections with both parties. Investments in branded checkout improvements, person-to-person (P2P) capabilities, and Venmo are translating into a growing number of active accounts.

The expected surge in Fastlane adoption is projected to further increase transaction volumes as PayPal establishes partnerships with companies like NBCUniversal, Roku, and StockX. Management aims for a minimum of 5% growth in transaction margins (excluding interest on customer balances) in 2025, with projections of high-single-digit growth by 2027 and long-term expectations exceeding 10%.

Investment Outlook for PayPal

With the rising demand for peer-to-peer payments and digital wallets, PayPal remains a promising investment for those who currently hold the stock. However, the company faces challenges in the near term due to factors like macroeconomic headwinds, unfavorable currency fluctuations, and tepid consumer spending.

Currently, PayPal holds a Zacks Rank #3 (Hold), suggesting that investors may want to wait for a more opportune entry point into the stock.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.