PayPal Surpasses Earnings Expectations in Q3 2024, Boosts Future Guidance

Strong Quarterly Performance Leading to Increased Investor Confidence

PayPal Holdings PYPL reported third-quarter 2024 non-GAAP earnings of $1.20 per share, exceeding the Zacks Consensus Estimate by 11.11% and marking a 22.4% rise compared to the previous year.

PYPL has consistently beaten earnings estimates in all four previous quarters, showcasing solid performance.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Net revenues reached $7.847 billion, showing a 6% year-over-year increase on both a forex-neutral basis and a reported basis. However, this missed the consensus estimate by 0.20%.

Transaction margin stood at $3.7 billion, up over 8% on a reported basis and more than 6% excluding interest on customer balances. This growth was driven by higher interest income, branded checkout services, Venmo, Braintree, and improvements in tech-led risk/loss management.

PayPal Holdings, Inc. Price, Consensus and EPS Surprise

PayPal Holdings, Inc. price-consensus-eps-surprise-chart | PayPal Holdings, Inc. Quote

Following a strong performance in the third quarter, PYPL raised its 2024 non-GAAP earnings guidance, a positive sign for investors. Year-to-date, PayPal shares have increased by 28.2%, outpacing the Zacks Computer & Technology sector’s return of 27.6%.

PYPL Outperforms Sector YTD

Image Source: Zacks Investment Research

Before we look into PYPL’s investment outlook, let’s review its quarterly results.

PYPL’s Revenues Rise Driven by High Payment Volume

For the quarter, total payment volume hit $422.641 billion, marking a 9% year-over-year increase, both on a spot-rate and forex-neutral basis. This figure exceeded the Zacks Consensus Estimate by 0.31%.

Transaction revenues amounted to $7.067 billion, constituting 90.1% of net revenues, reflecting a 6.2% increase year-over-year. Meanwhile, Value-Added Services revenues reached $780 million, or 9.9% of net revenues, a rise of 2.1% from the previous year.

In the U.S., revenues totaled $4.518 billion, representing 58% of net revenues, also up 6% year-over-year. International revenues were $3.329 billion, accounting for 42% of net revenues, which is a 5% year-over-year increase on a reported basis and 6% when adjusted for foreign exchange impacts.

PayPal recorded a 1% increase in total active accounts, bringing the total to 432 million for the quarter, which outperformed the Zacks Consensus Estimate by 0.48%.

Total payment transactions reached 6.631 billion, a 6% increase year-over-year, although this figure fell short of expectations by 4.22%.

Each active account facilitated approximately 61.4 million transactions, an increase of 9% compared to a year prior.

Operating expenses for PYPL were $6.456 billion in Q3 2024, showing a 3.3% increase year-over-year. As a percentage of net revenues, this figure declined by 200 basis points year-over-year to 82.3%.

The transaction expense rate was recorded at 0.91%, down from 0.93% from the previous year. The transaction margin improved by 120 basis points to 46.6% and the non-GAAP operating margin grew by 200 basis points to 19%.

PYPL Maintains a Strong Balance Sheet

As of September 30, 2024, PayPal reported cash, cash equivalents, and investments totaling $16.2 billion. Long-term debt stood at $9.976 billion.

Cash generated from operations was $1.614 billion, while free cash flow tallied $1.54 billion in the third quarter.

The company returned $1.8 billion to shareholders through share repurchases.

PayPal Increases FY24 Earnings Guidance

For the full year 2024, PayPal now expects non-GAAP earnings to grow in the high teens, an increase from the previous low to mid-teens guidance for 2023.

The Zacks Consensus Estimate for earnings is currently at $4.44 per share, indicating a 12.94% decline compared to 2023’s figure. Meanwhile, the consensus for revenues stands at $31.93 billion, suggesting a 7.27% growth from 2023.

PayPal anticipates transaction margin dollar growth in the mid-single digits for 2024.

In the fourth quarter of 2024, the company expects low-single-digit revenue growth. The Zacks Consensus Estimate for revenues is set at $8.49 billion, reflecting a 5.76% year-over-year growth.

Non-GAAP earnings are projected to see a low to mid-single-digit decrease year-over-year. The Zacks Consensus Estimate for earnings is $1.10 per share, a decline of 25.68% from the year-ago quarter.

Strengthened Portfolio and Partner Collaborations Propel PYPL’s Future

PayPal’s strong portfolio enhances its relationships with both merchants and consumers. Its two-sided platform fosters direct connections and financial relationships.

The launch of Fastlane, designed to improve the guest checkout experience by allowing purchases to be completed with just one click, signifies innovation, currently available in the United States. This initiative utilizes the company’s extensive payment expertise to enhance the customer’s checkout experience.

Growing partnerships are also benefiting PayPal. Collaborations with Apple AAPL and Alphabet GOOGL to integrate the Venmo debit card with Apple Pay and Google Pay are significant developments.

PayPal remains a leading payment method for advertisers and consumers worldwide, particularly within Meta Platforms’ META suite of apps. Creators and developers have adopted Hyperwallet, while Braintree supports credit card processing for META.

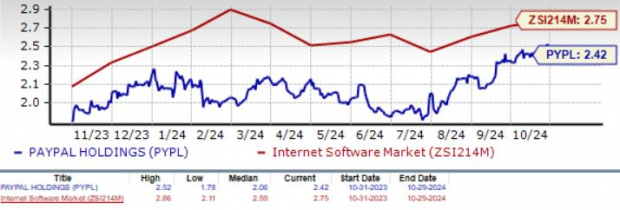

PayPal Shares Currently Offer a Discount

Presently, PayPal trades at a forward Price/Sales ratio of 2.42X, below the industry average of 2.75X, signifying potential opportunities for investors.

PYPL’s Value Score of B may attract further attention.

Price/Sales Ratio (F12M)

Image Source: Zacks Investment Research

Conclusion

As demand for peer-to-peer payments and digital wallets continues to rise, PayPal presents compelling long-term growth prospects for investors already holding shares. However, the company faces short-term challenges due to a tough economic environment and a slowdown in consumer spending, thereby making it a riskier option according to its Growth Score of D.

Currently holding a Zacks Rank of #3 (Hold), investors may want to wait for a better entry point into the stock. Check out the complete list of today’s Zacks #1 Rank (Strong Buy) stocks.

Zacks Identifies Top Semiconductor Stock

It’s only 1/9,000th the size of NVIDIA, which soared over +800% since our initial recommendation. While NVIDIA remains strong, our new top chip stock has significant room for growth.

With robust earnings growth and an expanding customer base, it’s well positioned to meet the soaring demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to grow from $452 billion in 2021 to $803 billion by 2028.

Want the latest recommendations from Zacks Investment Research? Download the report on 5 Stocks Set to Double for free.

Apple Inc. (AAPL): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL): Free Stock Analysis Report

Meta Platforms, Inc. (META): Free Stock Analysis Report

To access this article on Zacks.com, click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.