Over the years, Netflix (NASDAQ:NFLX) has shown impressive adaptability in the ever-evolving entertainment industry, constantly innovating to meet the changing demands of its customer base. From their humble beginnings of mailing DVD movie discs to their current dominance in the streaming market, Netflix has consistently delivered above-average growth, surpassing even the most skeptical expectations.

However, as the share price approaches $500, there are concerns that it may be overreaching, particularly if a potential recession in 2024-25 could dampen growth rates. This scenario has not been factored into current analyst estimates, leaving room for a possible downside. This contrasts with the overly pessimistic outlook in the middle of 2022.

Reflecting on the fluctuations in Netflix ratings over the years, the current price point of $500 raises concerns. The analyst, having previously taken a contrarian position by purchasing shares at around $200 in April 2022, now sees the current valuation as on the higher end of the spectrum.

Hence, the analyst has downgraded their rating from Hold to Sell, citing concerns about the impact of rising interest rates in 2023 coupled with a potential recession in streaming demand in 2024. The proposed target price range is now set at $350 to $400 within the next 12 months.

Excessive Valuation

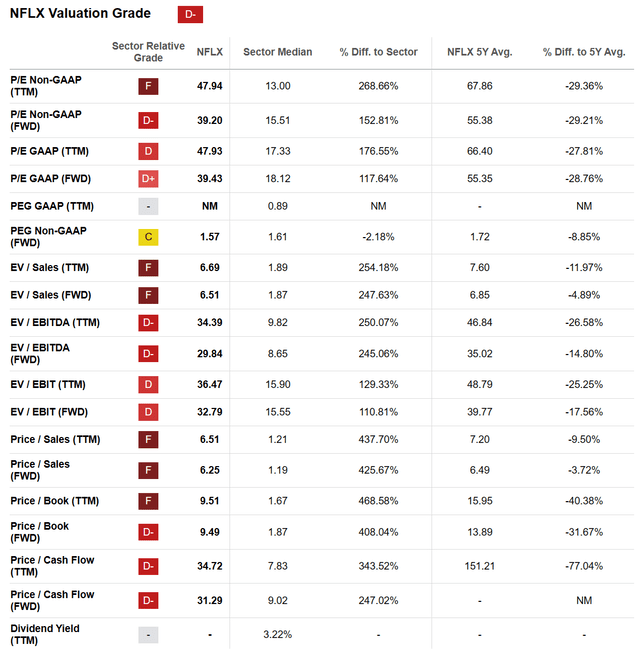

Examining the fundamental valuation picture reveals a conflicting scenario. While the valuation on earnings, sales, cash flow, and book value is lower than five years ago, it is substantially higher than in Q2 2022. The current valuation appears excessive, especially when compared to other streaming-focused film/TV companies.

Looking ahead, concerns arise regarding the enterprise valuation on forward core-EBITDA, seen as too high compared to similar companies in the streaming industry. The current multiple of 23x is notably expensive, maintaining a consistent premium to peers since late 2021.

Furthermore, the earnings and free cash flow yields are markedly lower compared to risk-free Treasury bills and notes. The relative earnings yield of Netflix stands at a negative -2.6%, the lowest reading since late 2005, posing substantial investment risks, particularly in the event of a potential recession and bear market.

Notably, Seeking Alpha’s Quant Valuation Grade for January 2024 stands at a low “D-“, highlighting the lack of a bargain in Netflix shares. This accounts for the necessity of a soft or non-existent landing in the general economy to maintain sales and earnings growth and support the current stock price of $500.

Technical Trading Upside Exhaustion?

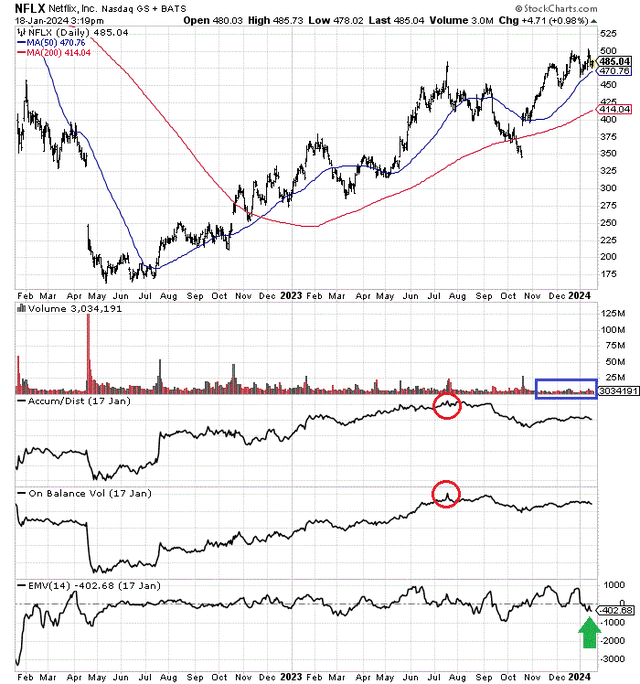

For long-term investors, Netflix has delivered significant profits over the past decade. Yet, for those who entered the market between late 2018 and early 2022, the gains have been less substantial. The recent market movement from May 2022 may be a rebound retracement of the substantial loss incurred from the November price peak around $700 per share.

Assessing the State of Netflix Stock and Strategic Recommendations

The recent trends in Netflix stock have given rise to apprehension about its future performance. With the ups and downs in play, it’s essential to evaluate the situation shrewdly to make informed investment decisions.

At a closer look, the 52-week highs of November to the present have been underpinned by diminishing buying interest, and volume has dwindled since the end of November. These market dynamics call for a prudent understanding of the implications on the stock’s future trajectory.

Additionally, metrics such as the Accumulation/Distribution Line and On Balance Volume peaked in July and have failed to confirm the recent upswing in prices. The implications of these non-confirmations on the bull trend are certainly disconcerting to investors.

Another critical indicator, the 14-day Ease of Movement indicator, points to limited selling volume in January, potentially signaling an impending significant shift in short-term price movements.

Cumulatively, these momentum signals indicate the possibility of a significant reversal in Netflix shares, suggesting cautious optimism amid the recent high trades of the New Year.

Strategic Considerations

In the quest to shore up its future prospects, Netflix could consider strategic acquisitions as a means to bolster its position in the market.

One compelling opportunity could be the potential acquisition of Paramount/CBS (PARA) (PARAA) assets. Amidst swirling rumors of Paramount being up for sale in 2024, a strategic move by Netflix to acquire these assets could be a game-changer.

To facilitate such a monumental acquisition, funding could be driven by a mix of equity and cash. Leveraging its current equity base, Netflix could feasibly pursue a transformative buyout, further consolidating its position in the streaming industry.

In contemplating the potential for Netflix’s stock to reach new heights, one must also consider the broader economic landscape. Envisaging a scenario of robust economic growth coupled with a favorable inflation and interest rate environment could pave the way for potential upside in Netflix shares.

Conversely, in a more pessimistic outlook with economic headwinds, the stock could face significant downside pressures. This duality of potential outcomes underscores the need for cautious deliberation in evaluating Netflix’s future trajectory.

Evaluating the Prospects

Assessing the potential risks and rewards, it becomes evident that a balanced outlook is necessary in navigating the dynamics of Netflix stock in the current market environment.

While contemplating the potential for significant gains, it is equally important to contemplate the potential downside risks, especially in the backdrop of prevailing economic uncertainties.

With the prospects of Netflix’s stock finely poised between optimism and caution, the imperative for informed decision-making looms large for investors.

All in all, the current signals suggest a mixed outlook for Netflix, necessitating a balanced and well-considered approach to investment decisions.

Ultimately, in light of the prevailing market dynamics, the prudent course of action would be to carefully weigh the risks and rewards associated with investing in Netflix at the present juncture.

In conclusion, navigating the intricate landscape of Netflix stock demands a judicious and balanced approach that takes into account both the potential upsides and downsides in the current market environment.

As always, consulting with a registered and experienced investment advisor is crucial before making any investment decisions, ensuring a diligent and informed investment strategy.