Mighty NIKE Inc., also known as NKE, recently unveiled its third-quarter fiscal 2024 performance, surpassing both the top and bottom-line predictions outlined by Zacks Consensus. A delightful surprise echoed through the investor community as revenues witnessed a year-over-year upswing. The impetus behind these positive results lies in the stellar retail sales across Nike Direct, reinforcing the efficacy of the company’s overarching business strategy, revolutionary product advancements, and resolute digital foothold.

The Q3 fiscal 2024 earnings per share (EPS) stood at 98 cents, marking a slight 3% dip from the previous year. Nevertheless, this figure soared past the Zacks Consensus Estimate of 69 cents per share, showcasing NIKE’s robust financial fundamentals.

The conglomerate behind the Swoosh brand showcased a 1% growth in revenues, reaching a pinnacle of $12,429 million, a figure that gracefully outpaced the Zacks Consensus Estimate of $12,272 million. Delving deeper, on a currency-neutral basis, revenues depicted a modest yet noteworthy uptick year over year.

The NIKE Direct sales witnessed a slight uptick both in reported and currency-neutral aspects, clocking in at $5.4 billion. This growth spurt was a direct consequence of amplified foot traffic both in brick-and-mortar stores and the online sphere. The numbers further revealed a 3% slump in NIKE Digital on a reported basis, juxtaposed against a 4% decline on a currency-neutral basis. Wholesale revenues took a healthy leap of 3%, climbing to $6.6 billion.

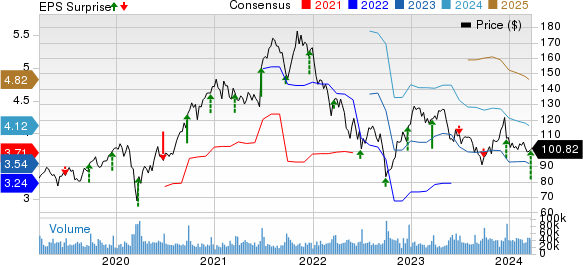

NIKE, Inc. Price Performance and Earnings Surprise

Witness the Resplendent Journey of NIKE, Inc. through its Price and Earnings Journey.

Investors cheered as the stock of this Zacks Rank #3 (Hold) entity surged by 12.1% in the last six months, gracefully outpacing the 9% growth within the industry.

Exploring the Operational Segments

The NIKE Brand reveled in revenues amounting to $11.9 billion, showcasing a commendable 2% uptick both on reported and currency-neutral grounds. This glorious feat was mainly fueled by the remarkable upsurge in North America, Greater China, and APLA, albeit offset by contractions in EMEA.

An in-depth analysis predicted a minuscule 0.2% dip year over year in the total NIKE Brand revenues for the fiscal Q3, largely orchestrated by a 1.3% decline in Direct-to-Consumer activities and a modest 0.8% rise in wholesale operations.

Tracing the regional trajectory, revenues within North America witnessed a commendable 3% rise year over year, tallying up to $5.6 billion. The NIKE Direct enterprise shone, unveiling a 2% surge in this region, including a 1% climb at Nike Digital and an exuberant 3% spike at Nike Stores. Wholesale sales mirrored this exuberance by ascending 5%.

On the contrary, EMEA bore the brunt of a 4% decline in revenues, dwindling to $3.6 billion. The Wholesale business nosedived by 8% year over year during this quarter. NIKE Direct revenues for this segment faced a 4% downturn, juxtaposed against a 6% increase at Nike Stores and a distressing 10% drop at Nike Digital.

Moving eastward to Greater China, revenues staged a resilient 6% ascent in the fiscal Q3, reaching $1.9 billion. NIKE Direct witnessed a marginal 1% dip, while NIKE Digital revenues plummeted by 13% year over year, juxtaposed against a 6% surge at Nike Stores. Wholesale revenues soared by a whopping 12%, spearheaded by robust sell-through rates. The retail partners experienced a double-digit upswing in sales year over year.

A similar pattern unfolded in APLA, with NIKE revenues ascending by a respectable 4% year over year, closing in at $1.8 billion. NIKE Direct burgeoned by 4% on a currency-neutral basis, majorly propelled by an ebullient 18% growth in NIKE Stores, tempered only by a 6% decline in Nike Digital.

Conversely, the Converse brand grappled with a 19% plunge on reported grounds and a 20% nosedive on a currency-neutral front, capping off at $495 million. This downturn was chiefly led by a soft performance in North America and Europe.

Scrutinizing Costs and Margins

The gross profit scaled up by a commendable 4% year over year, reaching $5.6 billion, and the gross margin exuberantly expanded by 150 basis points (bps) to 44.8%. Expectations revolving around the gross margin approaching a 160 bps expansion to 44.9% were largely met. This uptick in gross margin drew strength from well-orchestrated pricing strategies, reduced ocean freight and logistics expenses, albeit partly subjugated by escalated input costs and restructuring charges.

Selling and administrative expenses embraced a 7% upsurge, tallying up to $4.2 billion, notably surpassing the anticipated 3.9% mark by reaching $4.1 billion.

The demand-creation expenses surged by a noteworthy 10% year over year to $1 billion, driven by a surge in marketing outlays. Operating overhead expenditures ticked up by 6% year over year to $3.2 billion, primarily spurred by restructuring charges, albeit partially cushioned by wage-related costs.

An astute model forecasted Demand Creation expenses to hover around the $1 billion mark, signifying a 9.6% year-over-year surge. As for Operating overhead expenses, projections hinted at a 2.1% uptick landing at $3.1 billion.

Peeking into the Balance Sheet and Investor-Friendly Moves

At the close of the quarter, the cash and cash equivalents vaulted to $9 billion, basking in a remarkable 29% growth rate from the preceding year. Short-term investments witnessed a downward spiral by 58% year over year, settling at $1.6 billion. Long-term debt (excluding current maturities) etched in at $8.9 billion; meanwhile, shareholders’ equity fortified to $14.2 billion as of Feb 29, 2024.

On the inventory front, the figures disclosed an impressive 13% downturn year over year, reflecting a marked improvement.

During Q3 fiscal 2024, the entity showered its stakeholders with $1.4 billion, of which $866 million was dedicated to share repurchases, and $562 million to dividends. The spirited share repurchases witnessed the retirement of 7.9 million shares during the third fiscal quarter as part of the colossal $18-billion share repurchase initiative bestowed upon the company’s future in June 2022. By the close of Feb 29, 2024, NIKE had spiritedly repurchased 73.8 million shares under this compelling program, invoking a total expenditure of $8 billion.

Envisioning the Future: Outlook Ahead

Management crafts a sage projection for Q4 revenues, hinting at a modest uptick. This forecast reflects a spurt in shipment timing benefits during the reported quarter, moderated by restrained digital growth ensuing from franchise lifecycle management. The looming shadows of a stronger U.S. dollar forecast a single-point adverse impact on reported revenues during the fourth quarter onwards.

The guidance spots restructuring charges of about $450 million in the second half, with an approximate expenditure of $403 million incurred during the third quarter. This ripples through the SG&A by inducing a 15 bps impact on the full-year gross margin. Management anticipates Q4 gross margins to ascend by roughly 150-180 bps. This positive trajectory stems from strategic price hikes, diminished ocean freight rates, stooped product input costs, and supply-chain efficacy, albeit marred by escalated markdowns, decreased benefits from the channel mix due to franchise lifecycle management, and aggravated foreign exchange volatilities.

Elaborating on the forthcoming fiscal 2024 terrain, both revenues and earnings are poised to carve a growth path, embellished with higher operating margins, sans the influence of the restructuring charges. However, the initial half might witness a minor recession in revenues. The gross margin holds a promise to expand by 120 bps in fiscal 2024, out of which 50 bps are earmarked to combat currency headwinds. SG&A expenses are predicted to experience a low-single-digit surge inclusive of restructuring charges. Sans these charges, SG&A is expected to mirror a roughly flat trajectory.

Spotlight on Consumer Discretionary Aces

Amidst the conglomerate’s glowing success, a few beacons stand apart in the consumer discretionary realm, including the likes of G-III Apparel Group (GIII), Crocs (CROX), and lululemon athletica (LULU).

GIII Apparel commands a Zacks Rank #1 (Strong Buy) currently. Peruse through the treasure trove of Zacks #1 Rank stocks hovering on the horizon.

GIII Apparel boasts a staggering four-quarter earnings surprise averaging 541.8%. The Zacks Consensus forecasts a bright future, further underscoring the prowess of these promising picks.

Unveiling Bullish Future Prospects for GIII and Fellow Retail Giants

GIII Forecasted to Surge: The Numbers Speak Volumes

An exciting forecast has surfaced regarding G-III Apparel Group, LTD. indicating an impressive 33% surge in Earnings Per Share for fiscal 2024 compared to the year-ago figures. This prediction signifies a promising trajectory for the company, hinting at robust growth.

Crocs and Lululemon Athletica: Riding the Positive Waves

Crocs, carrying a Zacks Rank #2 (Buy), has been making waves in the market with a remarkable four-quarter earnings surprise of 17.4% on average. The Zacks Consensus Estimate for Crocs in 2023 paints a bright picture, with anticipated sales and EPS growth standing at 11.4% and 8.6% respectively.

Another retail giant, lululemon athletica, known for its yoga-inspired athletic apparel, proudly holds a Zacks Rank of 2. The company has exhibited consistent growth trends, with their sales and EPS for the current financial year projected to rise by 18.2% and 22.8% respectively from the previous year.

Unveiling the “Single Best Pick to Double”

Zacks experts have unveiled a potential stock gem poised for tremendous growth in the upcoming months. This investment prospect is described as a “watershed medical breakthrough,” nurturing a range of projects focused on diseases related to the liver, lungs, and blood. Delving into this opportunity presents a chance to capitalize on its emergence from bear market conditions.

The growth potential of this stock has the power to rival or even surpass the explosive surges witnessed in recent times by companies like Boston Beer Company and NVIDIA, solidifying its status as a potentially lucrative investment option.

For insightful stock analysis and a glimpse into the top-performing stocks, analysts recommend diving into the shares of NIKE, Inc., lululemon athletica inc., Crocs, Inc., and G-III Apparel Group, LTD. for a comprehensive understanding of the retail landscape.

As investors seek the latest recommendations and market insights, platforms such as Zacks Investment Research provide a wealth of resources to guide them in making informed decisions for their portfolio.

It’s clear that the retail sector is abuzz with excitement as these giants pave the way for substantial growth and profitability. With favorable forecasts and strong market positions, GIII and its counterparts are set to create ripples in the financial realm, drawing investors towards promising opportunities for wealth creation and portfolio diversification.

The views expressed by Zacks Investment Research signify a valuable standpoint in the fast-paced world of finance, shedding light on the potential growth trajectories for investors seeking lucrative prospects in the retail sector.