The market is abuzz with the promise of artificial intelligence (AI), propelling stocks to new heights. In this AI-driven narrative, Nvidia (NASDAQ: NVDA) shines brightly as the leading protagonist.

Nvidia’s pioneering work in compute networking is revolutionizing AI applications, spanning machine learning, generative AI, and large language models (LLMs). As the cornerstone of cutting-edge AI systems, Nvidia has captured investors’ hearts, driving its shares up by an astonishing 265% in the past year.

As Nvidia flirts with its recent all-time high, some investors may harbor doubts about jumping on the bandwagon. But here’s the scoop – with Nvidia’s strategic moves and long-term growth prospects, now might just be the perfect time to dive into the stock.

A Swift Ascent

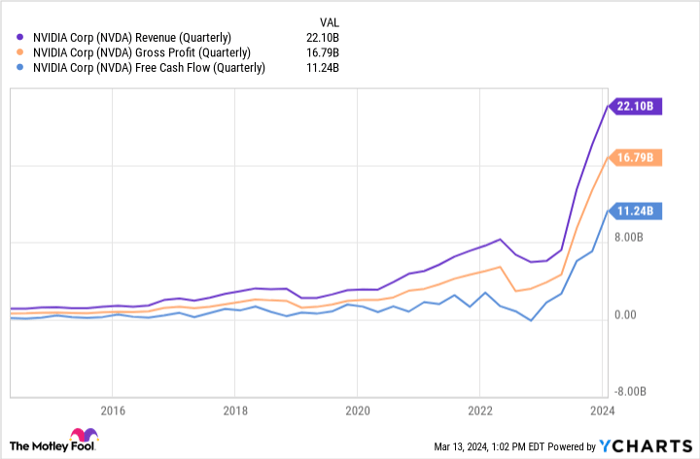

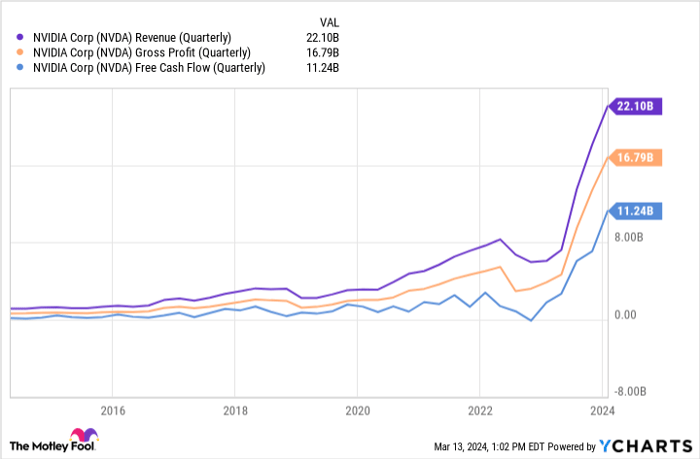

Let’s take a glance at Nvidia’s quarterly revenues, gross profits, and free cash flows over the last decade.

NVDA Revenue (Quarterly) data by YCharts.

Nvidia not only boasts soaring sales figures but also commands a dominant position in the graphics processing unit (GPU) and data center realm, granting it unmatched pricing leverage. This has significantly bolstered profit margins, translating to substantial bottom-line growth.

In 2023, Nvidia catapulted its free cash flow sixfold, catching the eye of a broader investor base. Consequently, a staggering $1 trillion has been grafted onto Nvidia’s market cap in under two months, underscoring its meteoric rise.

![]()

![]()

Image source: Getty Images.

Nvidia’s Deep Pockets and Strategic Spending

Fueled by an exceptional performance in 2023, Nvidia has doubled its cash reserves to a formidable $26 billion. While this is impressive, what I find more encouraging is Nvidia’s judicious capital allocation.

The company is venturing into AI software applications with investments in SoundHound AI for voice recognition technology and Databricks for data analytics. Despite its hardware focus, Nvidia is quietly expanding into enterprise software, with a software services segment hitting a $1 billion annual revenue run rate — a noteworthy achievement yet still dwarfed by its $47 billion compute networking business.

Nvidia’s participation in a funding round for Figure AI, alongside key players like Microsoft, OpenAI, Intel, and Jeff Bezos, heralds exciting prospects. Figure AI is crafting humanoid robots for various industries, opening doors for Nvidia to contribute significantly from both hardware and software angles.

An Expensive Stock with Premium Potential

Following Nvidia’s stock surge, its valuation metrics have stretched quite a bit. Shares trade at 77 times trailing-12-month earnings, with a forward P/E ratio of 37 – nearly double the S&P 500’s. Despite this ultra-premium valuation, I perceive Nvidia as a compelling play for long-term investors.

Given the robust tailwinds propelling AI budgets, Nvidia’s expertise in both hardware and software, along with its strategic investments, I believe the company’s journey has just begun. Employing dollar-cost averaging to gradually accumulate Nvidia shares can be a prudent strategy, balancing risk while positioning for the long-term gains of both Nvidia and the AI domain.

Is It Time to Invest $1,000 in Nvidia?

Before diving into Nvidia stock, consider this:

The Motley Fool Stock Advisor analyst team has pinpointed what they deem the 10 best stocks for investors to snag, excluding Nvidia. These chosen 10 stocks hold the promise of significant returns in the forthcoming years.

Stock Advisor furnishes investors with a roadmap to success, including portfolio-building guidance, analyst updates, and bi-monthly stock picks that have outperformed the S&P 500 by threefold since 2002*.

Explore the 10 stocks

*Stock Advisor returns as of March 11, 2024

Adam Spatacco holds positions in Microsoft and Nvidia. The Motley Fool holds positions in and endorses Microsoft and Nvidia. The Motley Fool recommends Intel and suggests options like long calls on Intel and Microsoft, as well as short calls on Microsoft and Intel. The Motley Fool upholds a disclosure policy.

The opinions expressed are solely those of the author and do not reflect the views of Nasdaq, Inc.