Before becoming the owner of the NFL’s Carolina Panthers and MLS’s Charlotte FC, David Tepper made his name (and money) through Appaloosa Management, a global hedge fund he founded. Tepper, whose net worth is around $20 billion, is one of the top 100 richest people in the world. Needless to say, he’s had success in the investing world.

Given Tepper’s success, it makes sense that investors would look to his and his hedge fund’s investments to gain tips. While the average investor and billionaire hedge fund managers don’t have the same risk tolerance or investment goals, there’s nothing wrong with looking to them for inspiration.

Tepper’s portfolio is fairly concentrated, with almost a third being held in three “Magnificent Seven” stocks. If investors want solid businesses with long-term sustainability, they need look no further.

1. Amazon

Amazon (NASDAQ: AMZN) became a household name because of its e-commerce business, but it has since branched out and become a major player in a handful of industries.

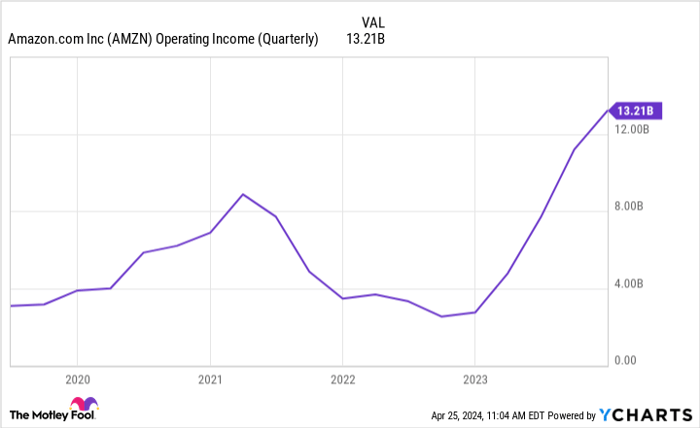

For a while, Amazon’s e-commerce business was unprofitable and used mainly as a revenue generator. It’s still Amazon’s biggest revenue source, but it has recently become profitable. In the fourth quarter, Amazon’s North American segment made around $6.5 billion in operating profits, an impressive turnaround from the $240 million it lost in Q4 2022. Its international segment lost $419 million, which isn’t ideal, but it still leaves Amazon profitable in its non-Amazon Web Services (AWS) businesses.

AMZN Operating Income (Quarterly) data by YCharts

There’s still room for growth in e-commerce, but much of Amazon’s growth will rely on its cloud service, AWS. Although AWS growth slowed recently, 13% year-over-year (YOY) growth isn’t too shabby for Amazon’s biggest profit-maker. AWS has a commanding market share in global cloud services but has lost a little ground over the past year. Still, its market share is 31%, which leads Microsoft‘s (NASDAQ: MSFT) Azure (a 24% share) and Alphabet’s Google Cloud (11%).

In the long term, Amazon stands to benefit from the organic growth of cloud services and e-commerce. However, the company has also shown that it’s willing to make investments in new industries. Take its $13.7 billion Whole Foods purchase and healthcare ambitions, for example. Investors can count on the company not getting complacent.

2. Microsoft

There are diverse tech businesses, and then there’s Microsoft, the poster child for casting a wide net of businesses.

Microsoft didn’t become the world’s most valuable public company by accident; it’s taken years of impressive business growth and a boost from AI mania. The latter may also carry the company through its next phases of growth.

Microsoft’s strategic partnership with OpenAI — which gives it exclusive licenses to OpenAI’s large language models (LLMs) — could be exactly what it needs to further strengthen its hold on office software. From Office (Excel, Word, PowerPoint, etc.) to Azure to Teams, Microsoft is almost unavoidable in the corporate world.

Microsoft’s abundance of corporate clients gives it an edge in ensuring its longevity and shielding against economic and market downturns. When times get hard, consumers can easily forego the newest smartphones or online shopping, and businesses can cut back on their advertising. It’s much harder for companies to stop using Office software, migrate their data off the cloud, or jump ship from established communication platforms like Teams.

With Microsoft, investors can be confident they’re investing in a company built for sustained growth over the long haul.

3. Meta Platforms

Facebook creator Meta Platforms (NASDAQ: META) continues to be one of the premier cash cow businesses, earning around $36.5 billion in revenue in Q1, up 27% YOY.

Averaging 3.24 billion family daily active people in March 2024 (up 7% YOY), Facebook shows why it continues to be a go-to for many of the top advertisers globally. Meta has capitalized on this, increasing its family average revenue per person from $9.47 in Q1 2023 to $11.20 in Q1 2024.

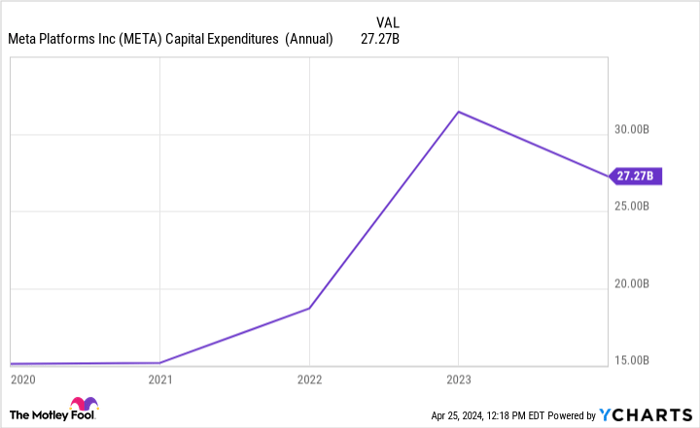

Despite the growth in key metrics, Meta’s stock plummeted after releasing its latest earnings, dropping as much as 15% on the same day. Much of this is because of the company’s spending plan going forward, which mostly surrounds its AI infrastructure. Meta said it plans to spend $35 billion to $40 billion this year, up from the prior $30 billion to $37 billion estimate.

META Capital Expenditures (Annual) data by YCharts

Investors may not agree with the spending plan, but their reaction seems overreactive. The good news, though, is that its lower valuation makes it a more compelling entry point.

Investors should also appreciate Meta’s new dividend of $0.50 per share. The dividend yield isn’t enough to please most income-seeking investors, but it’s an incentive that can encourage investors’ patience as Meta works on its AI plans.

Should you invest $1,000 in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of April 22, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Stefon Walters has positions in Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.