![]()

![]()

Palantir Technologies Inc. (NYSE:PLTR) has shifted from its enigmatic past to an era of commercial expansion that encompasses potential roaring growth. Known for years as a clandestine government contractor, Palantir’s recent foray into mainstream commercial success has ignited a wave of prosperity.

With its domination in the AI software and services market, Palantir is poised for an upswing in both growth and profitability. Despite a 100% increase in its stock over the last year, the widely anticipated “Nvidia moment” for Palantir hasn’t materialized just yet. Nevertheless, the stock is teetering on the cusp of significant advancement, destined to ascend further in the intermediate and long term.

Anticipated Technical Breakout

After an outstanding performance in the last quarter, Palantir appears to be on a trajectory for a potential breakout. As we witness the continuation of its upward momentum in Q4, the stock has made a remarkable after-hours surge, ultimately eclipsing the $20 threshold by over 21%. This substantial achievement significantly raises the likelihood of Palantir revisiting the pivotal $20-$22 range and potentially catapulting further to $25 or beyond.

The technical indicators, including the CCI, RSI, and full stochastic, are showing a shift towards heightened bullish momentum, pointing towards an imminent uptick in the stock’s trajectory. Furthermore, a sequence of ascending peaks and troughs signifies an impending breakthrough. The confluence of technical and fundamental tailwinds ingeniously positions Palantir’s stock, residing between the 50 and 200-day MAs, for an auspicious ascent.

Approaching the Nvidia Moment

Unveiling the Nvidia Moment

The “Nvidia moment” characterizes the instance when a company forecasts significantly stronger-than-expected sales and profitability, propelled by an unprecedented surge in demand for AI-related products and services. Notably, Nvidia, almost a year ago, amplified its revenues by approximately 50% above consensus estimates, triggering a remarkable rally in its stock, which has since tripled.

Recently, Super Micro Computer, Inc. (SMCI) experienced its own “Nvidia moment,” pre-announcing stellar guidance that promptly fueled a sensational 100% surge in its stock within weeks. As an AI-driven optimization software frontrunner, Palantir, with its escalating commercial clientele and revenues, stands on the brink of its own paradigm-shifting “Nvidia moment” – an event with immense potential to propel its stock to unforeseen heights.

Palantir’s AIP Platform

Palantir’s Accelerating Innovation Platform (AIP) is a comprehensive AI platform that revolutionizes enterprise operations, offering AIP boot camps that rapidly propel enterprises from inception to pragmatic applications, resolving immediate business challenges. Empowered by Ontology, the heart of AIP integrates AI with enterprise data, logic, and action, enabling seamless decision-making. From secure LLM access to end-user applications, AIP furnishes an integrated framework, breathing life into full-spectrum AI and optimizing daily decision-making processes.

AIP Solutions and Services Encompass:

- Semantic Data Layer.

- Dynamic Logic Layer.

- Kinetic Action Layer.

- Granular AI Guardrails.

- AIP Logic.

- AIP Scenarios.

- AIP Automate.

- Vector Management.

- AIP Tool Factory.

- Feedback-Driven AI Ops.

- AIP Application Suite.

- APIs, SDKs, & More.

Palantir’s all-encompassing solutions and services, catering to organizations worldwide, position it as a prime candidate for long-term investment and solidify its standing as a buy-and-hold entity for the forthcoming decade.

Continuous Improvement in Results

In Q4, Palantir reported non-GAAP EPS of eight cents, in line with estimates, and revenues of $608.35 million, surpassing expectations by $5.55 million.

Promising 2024 Projections Include:

- Anticipated revenues of $2.652-$2.668 billion.

- US commercial revenue exceeding $640 million, representing a growth rate of at least 40%.

- Adjusted income from operations of $834-$850 million.

- Adjusted free cash flow of $800 million-$1 billion.

- GAAP operating income in each quarter of the year.

- GAAP net income in each quarter of the year.

Palantir’s Profit Growth and Future Prospects

Palantir Technologies Inc. has seen its U.S. commercial revenues surge by a staggering 70% year-over-year in the last quarter, with overall commercial revenues increasing by 32% compared to the previous year. This trend indicates that U.S. companies are at the forefront of leveraging Palantir’s solutions compared to their European and international counterparts. With such buoyant commercial growth, future quarters are likely to witness a further spike in international commercial growth.

In Q4 of last year, Palantir sealed 103 deals worth $1 million or more, marking a substantial 100% increase from the prior year’s Q4. The U.S. commercial customer count also saw robust growth, expanding by 55% year-over-year and 22% quarter-over-quarter. Over the last three years, the U.S. commercial count has grown an impressive 13-fold. Moreover, Palantir reported its fifth consecutive quarter of adjusted operating margins and GAAP profitability.

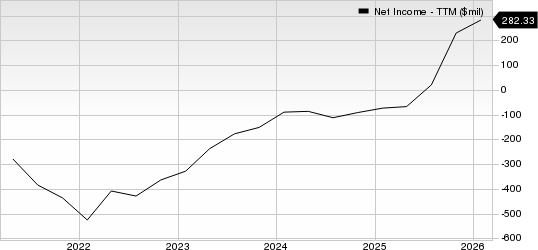

Palantir is Becoming More Profitable

Palantir’s net income has made a significant leap from a loss of $124 million in Q3 2022 to a gain of $93.4 million in the last quarter. This remarkable achievement occurred despite a relatively sluggish economic environment compounded by the challenges of a high-interest rate scenario. Nevertheless, numerous firms are turning to Palantir to streamline their operations. As economic conditions improve and the Federal Reserve adopts a more accommodative monetary policy, Palantir’s growth potential could accelerate even further.

Operating Margin is Surging

Palantir’s GAAP operating income surged to $65.8 million in the last quarter, showcasing a GAAP operating margin of 11%, which is up 1,500 basis points year-over-year. This upward trajectory suggests that Palantir is becoming increasingly profitable with scale and is likely to continue enhancing its profitability in subsequent quarters. The company’s gross margin also exhibited a robust performance, reaching 84% in the last quarter, showing an increase from 82% both quarter-over-quarter and year-over-year. This enhancement underscores Palantir’s exceptionally high potential for profitability and improving profitability with scale.

Profitability Could Increase More Than Expected

Palantir’s earnings per share (EPS) skyrocketed by over 300% in the past year, a feat achieved in a high-interest rate and relatively slow economic environment. Despite the firm’s burgeoning commercial business growth and rapidly expanding profitability, the consensus estimate currently stands at only 19% EPS growth for the current year. However, it is important to note that this $0.29 consensus EPS estimate seems markedly conservative, and it is conceivable that Palantir could attain significantly higher profitability this year, prompting upward earnings revisions in the subsequent quarters.

I’m convinced that Palantir has the potential to achieve at least $0.35 in EPS this year, in line with the higher-end estimates. This projection suggests an EPS growth rate of 40% for this year, setting the stage for a 35% EPS growth estimate for 2025, indicative of reaching approximately $0.47 in EPS next year. Consequently, based on conservative estimates, Palantir may be trading at a forward price-to-earnings (P/E) ratio of around 40, a seemingly modest valuation for a dominant market leader like Palantir positioned advantageously in the industry.

| Year | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Revenue (Bs) | $2.87 | $3.64 | $4.6 | $5.7 | $7.1 | $8.8 | $10.7 |

| Revenue growth | 29% | 27% | 26% | 25% | 24% | 23% | 22% |

| EPS | $0.35 | $0.47 | $0.61 | $0.78 | $0.99 | $1.24 | $1.55 |

| EPS growth | 40% | 35% | 30% | 28% | 27% | 25% | 25% |

| Forward P/E | 60 | 58 | 56 | 55 | 54 | 52 | 50 |

| Stock price | $28 | $35 | $44 | $54 | $67 | $81 | $99 |

Source: The Financial Prophet

Employing relatively conservative estimates considering Palantir’s market-leading position and potential in the AI space, it is plausible that we could witness higher revenue and EPS growth, leading to a more substantial multiple expansion and an augmented stock price in the forthcoming years. Under this “base-case” scenario forecast, it is conceivable that Palantir’s stock price could appreciate by as much as fivefold over the next several years, reaching a crescendo by 2030.

Risks to Palantir

Notwithstanding my optimistic assessment, Palantir is not immune to risks. A potential risk entails a slower-than-expected economic recovery and protracted periods of elevated interest rates. Furthermore, there is a risk of a subdued demand for Palantir’s services, particularly from foreign companies and the government sector. Palantir’s government segment has noticeably decelerated, and continued contractions could exert downward pressure on the stock. Additionally, the specter of competition looms, with other companies vying to encroach upon Palantir’s territory. Any deviation in profitability from the projected trajectory could impede the pace of share appreciation. Hence, prospective investors should carefully scrutinize these and other risks before considering an investment in Palantir.