Last month, the retail titan Walmart (NYSE: WMT) sent waves through the financial markets by announcing a rare event—a 3-for-1 stock split scheduled for Feb. 23. This move marked Walmart’s first split in over two decades, harking back to the days of Britney Spears’ “Baby One More Time” and the dazzling rise of the dot-com era.

Let’s delve into the intricacies of stock splits and why astute investors are giving Walmart’s latest maneuver a second look.

Decoding the Dynamics of Stock Splits

The mechanics of stock splits are elegantly simple: as the split ratio ascends, the share count follows suit, while the stock price descends proportionally. The upcoming 3-for-1 split will grant existing shareholders three times as many shares at a third of their former value.

It’s crucial to note that stock splits do not inherently shift a company’s value, as the increase in shares harmonizes with the decrease in share price. Yet, the aftermath of a split can spark heightened interest as the stock’s perceived affordability beckons a broader array of potential investors.

These post-split scenarios can beckon momentum traders to the scene. Although a swift profit may allure, it’s a perilous game that could have you clutching an empty bag. Potential Walmart investors are urged to gaze beyond the split’s allure and scrutinize the company’s long-term prospects steadfastly.

Image source: Getty Images.

Walmart’s Earnings Journey

For the quarter concluding on Jan. 31, Walmart unveiled an earnings per share (EPS) figure of $2.04, marking a modest 12% dip from the previous year. During the earnings call, management articulated strategies to ramp up earnings momentum, highlighting the brand’s evolution beyond traditional brick-and-mortar confines.

Specifically, the management spotlighted advertising and fulfillment services as lucrative domains outshining the standard retail landscape. Further, Walmart’s ongoing enhancements to stores and fulfillment centers could fuel synergies within its digital commerce spectrum.

The overarching ambition of the leadership is to propel “operating income faster than sales,” laying the groundwork for robust earnings growth in the long haul. Despite Walmart’s array of tantalizing catalysts, prudent investors should size up the stock’s valuation before leaping aboard.

Unpacking Valuation: Is Walmart a Diamond in the Rough?

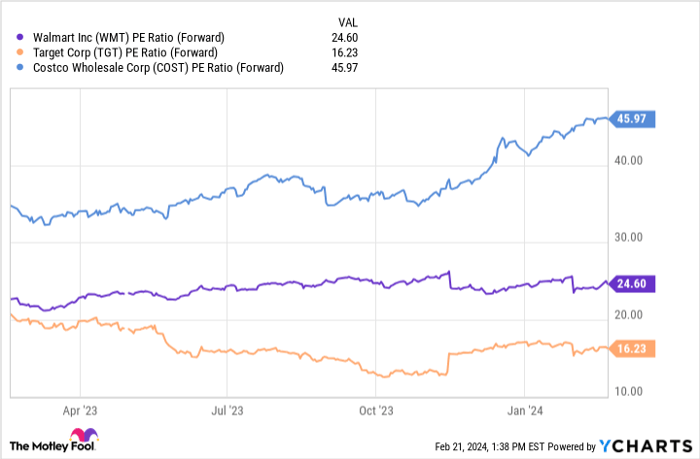

WMT PE Ratio (Forward) data by YCharts

The graph above elucidates Walmart’s forward price-to-earnings (P/E) ratio juxtaposed with peers like Costco Wholesale and Target. With a forward P/E of 24.6, Walmart stands midstream between its two counterparts, slightly eclipsing the S&P 500‘s corresponding figure of 22.9.

While Walmart’s laurels as a newly-minted Dividend King are noteworthy, the crux lies in its consistent generation of ample cash flow, channeled adeptly towards rewarding stakeholders.

Though not a steal at current valuations, myriad reasons beckon consideration for Walmart’s stock, particularly for dividend enthusiasts. All things considered, Walmart stands as a promising candidate to monitor closely. Proceed with caution, dear investors, as anticipating the post-split ebbs and flows may be prudent.

Should you partake in a $1,000 stint with Walmart’s shares today?

Before you cast your lot with Walmart, ponder this:

The Motley Fool Stock Advisor maestros have handpicked what they deem as the 10 ultimate stocks for investors today… and Walmart didn’t make the cut. These 10 contenders have the potential to yield mammoth returns in the foreseeable horizon.

Stock Advisor furnishes an easy playbook for investors, comprising tailored portfolio insights, regular analyst updates, and bimonthly stock suggestions. Since 2002, the Stock Advisor service has outperformed the S&P 500 by thricefold*.

Explore the top 10 stocks

*Stock Advisor returns as of February 20, 2024

John Mackey, erstwhile CEO of Whole Foods Market, an Amazon offshoot, steers The Motley Fool’s board of directors. Suzanne Frey, a luminary at Alphabet, also graces The Motley Fool’s board. Adam Spatacco holds stakes in Alphabet, Amazon, and Tesla. The Motley Fool endorses and maintains positions in Alphabet, Amazon, Costco Wholesale, Target, Tesla, and Walmart. The Motley Fool abides by a transparency policy.

The insights and opinions aired herein are the author’s own and may not mirror those of Nasdaq, Inc.