Global PC Market Sees Growth Amid Tariff Uncertainties in 2025

The global PC market kicked off 2025 with strong first-quarter shipments reflecting a year-over-year increase of 4.9%, amounting to 63.2 million units, as reported by International Data Corporation (“IDC”). This growth signifies the sixth consecutive quarter of positive momentum. Nevertheless, the industry’s near-term outlook remains highly unpredictable due to new U.S. tariff policies, ongoing inflation concerns, and fluctuating PC upgrade cycles.

Boosted Shipments Anticipate New Tariffs

Though first-quarter shipment data portrays a robust PC market, much of this growth stems from vendors and buyers strategically stockpiling inventory in anticipation of new tariffs announced by the U.S. government in early April. According to IDC, these tariffs are anticipated to directly affect hardware imports from China, potentially increasing costs for suppliers and consumers alike in the upcoming quarters.

IDCs insights indicate that many players within the PC supply chain opted to accelerate shipments in the first quarter, aiming to sidestep additional tariff pressures. This uncharacteristic surge may have inflated the first-quarter results, leading to uncertainty regarding how the rest of the year might unfold once the full effects of the tariffs become evident.

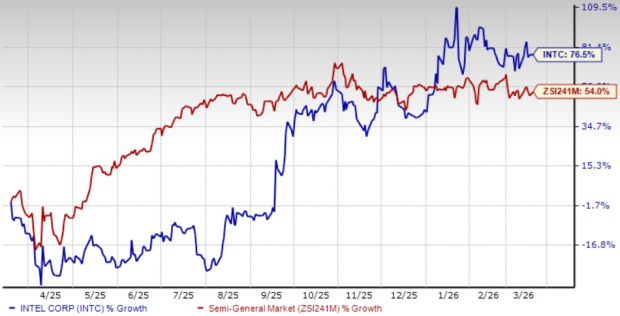

5-Year Return Trends in Mini Computers

5-Year Return Trends in Mini Computers

Steady Commercial Demand Persists

Despite the inflated first-quarter results due to pre-tariff stockpiling, indicators suggest that key drivers of PC demand remain stable, particularly in the commercial segment. Two structural factors seem to support demand for commercial PCs.

Firstly, businesses are likely to refresh their PCs ahead of the impending end of Microsoft’s Windows 10 support in October 2025. Secondly, there is a growing interest in PCs that come equipped with on-device AI capabilities, which may significantly boost demand for the sector.

Ongoing trends have been instrumental in maintaining strong demand throughout the first quarter. Even if consumer confidence weakens due to rising prices, the enterprise refresh cycle alongside innovations in AI-enabled devices could provide some degree of stability for PC manufacturers.

Vendor Performance and Market Share Insights

Among leading vendors, Lenovo (LNVGY) sustained its market dominance with 15.2 million shipments and a market share of 24.1%, up from 22.8% during the same period last year. HP Inc. (HPQ) followed with 12.8 million shipments, showing a modest year-over-year increase, while Dell Technologies (DELL) posted a smaller uptick of 3%, reaching 9.6 million units, achieving market shares of 20.2% and 15.1%, respectively.

Apple (AAPL) distinguished itself with the highest year-over-year growth among leading players, reporting a 14.1% increase, culminating in first-quarter shipments of 5.5 million units and a market share of 8.7%.

ASUS also gained attention with an 11.1% increase in shipments, leading to a 6.3% market share. In contrast, smaller manufacturers classified as “Others” experienced a collective decline of 3.6%, revealing a consolidation of market share towards larger, more robust competitors.

Future Outlook for the PC Industry

The announcement of new U.S. tariffs on April 2 has fostered an atmosphere of uncertainty in the industry. Although companies have yet to respond fully, Ryan Reith, IDC’s group vice president of Worldwide Device Trackers, suggests that strategic shifts are imminent. Vendors may consider options such as relocating production, adjusting inventory levels, or seeking trade exemptions. Reith believes that regardless of the path chosen, cost increases are likely to be passed on to both consumers and enterprise buyers.

This scenario raises the possibility of delayed purchases in subsequent quarters. If hardware prices escalate and economic sentiment continues to weaken, even a vigorous commercial refresh cycle may struggle to maintain demand at the high levels seen in the first quarter.

Conclusion: Navigating Market Volatility

The PC market displayed strong initial activity in 2025, but the overarching circumstances suggest instability. The pre-tariff inventory adjustments inflated first-quarter metrics and may obscure future performance. Stakeholders should brace for an increased degree of uncertainty as the impending effects of tariffs take hold, particularly in the face of rising inflation and broader economic concerns.

Currently, HP, Dell, and Lenovo each carry a Zacks Rank #3 (Hold). In contrast, Apple holds a Zacks Rank #4 (Sell).

5 Stocks with Potential to Double

Each stock has been chosen by a Zacks expert as a top pick, projected to gain 100% or more in 2024. While not every recommendation can achieve such success, previous selections have shown substantial gains, including +143.0%, +175.9%, +498.3%, and +673.0%.

Most stocks featured in this report remain under the radar of Wall Street, presenting an excellent entry point for investors. Today, explore these 5 potential high-return opportunities >>

For the latest analyses from Zacks Investment Research, you can download the “7 Best Stocks for the Next 30 Days.” Click to access this free report.

Apple Inc. (AAPL): Free Stock Analysis report

HP Inc. (HPQ): Free Stock Analysis report

Dell Technologies Inc. (DELL): Free Stock Analysis report

Lenovo Group Ltd. (LNVGY): Free Stock Analysis report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.