The Untold Story of Perion Network

Perion Network (NASDAQ:PERI) is a global tech leader in the digital marketing industry, propelling businesses to connect with their target audiences more effectively in the digital sphere. The company operates two streams of revenue: Display advertising and Search advertising. To add context, display advertising includes visually captivating elements like images and videos, akin to digital billboards, while search advertising strategically positions text or visual ads within search engine results, ensuring businesses command a prominent presence amidst user searches, driving potential customers to their offerings.

By the end of 2022, display advertising accounted for 56% of PERI’s total revenue, with search advertising constituting the rest. Notably, the majority of its revenue springs from the United States, with 86% and 89% of search and display advertising revenue being generated in North America in 2022, respectively.

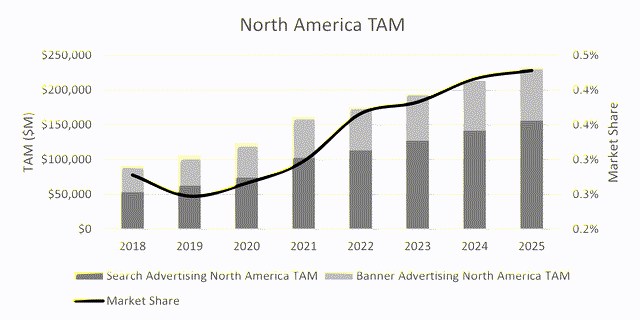

Notably, PERI operates in two colossal markets that hold massive long-term opportunities. As illustrated in Figure 1 below, the North American search and display advertising markets saw an 18% CAGR from 2019-2022, reaching nearly $175 billion, with PERI representing less than a half percent of the total market. Looking ahead, the industry is expected to continue strong growth, soaring to approximately $232 billion by 2025, marking a ~10% CAGR from 2022 levels. Given the market’s enormity and PERI’s robust competitive positioning, it’s highly probable that PERI will continue to gain market share in the coming years.

Despite its shares being flat over the past year, in stark contrast to the S&P 500’s 23% surge, PERI’s solid fundamental profile suggests an opportune entry point for investors. Especially if the Fed moves to lower interest rates in 2024, potentially freeing up capital for advertising. At current valuation levels, PERI presents a compelling investment opportunity, promising significant potential for share appreciation in the near and distant future. We peg PERI with a Buy rating and a price target of $46, implying a ~62% upside from its current share price.

Trailblazing Financial Performance

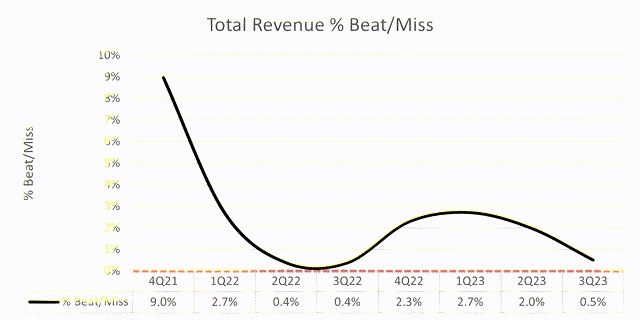

Perion Network consistently delivers robust financial results, despite its recent share price performance. As showcased in Figure 2 below, in each of the past eight quarters, PERI has surpassed or met consensus expectations for its top-line, instilling confidence in the management’s strong visibility into its business. In 3Q23, PERI’s top-line surged 17% year-over-year, a commendable growth given the current macro environment.

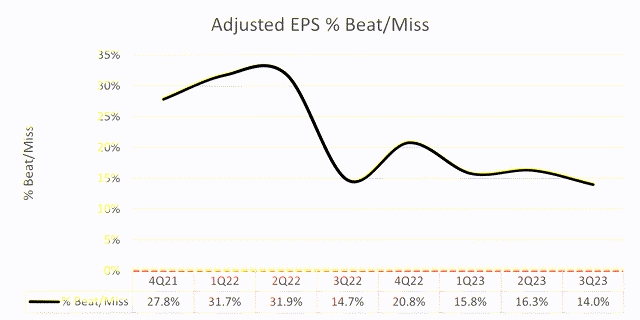

Furthermore, PERI’s bottom-line results have been even more impressive, consistently outperforming consensus estimates over the last eight quarters, evidenced in Figure 3 below. In 3Q23, PERI’s adjusted EPS soared 39% year-over-year, reaching $0.84, signaling the company’s poised position to further expand its earnings in the future, leveraging its business model and diversifying its revenue streams.

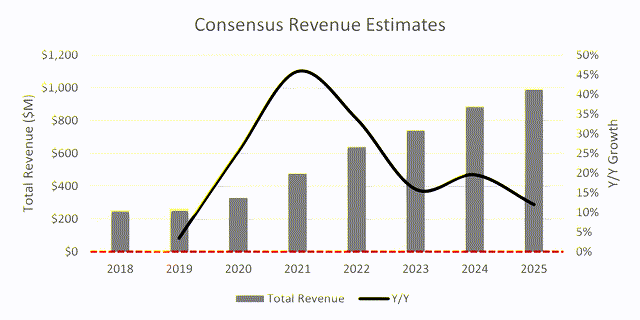

Outlined in Figure 4 below, we can see Perion Network’s historical revenue and consensus estimates through 2025. From 2019-2022, PERI’s revenue surged at a CAGR of 35%, and while future growth is expected to taper, estimates suggest that PERI will still expand its top-line at a CAGR of 16% from 2022-2025, a commendable growth given the competitive landscape and ongoing macro challenges.

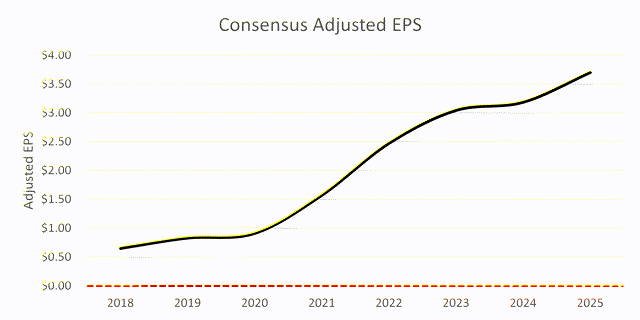

Similarly, depicted in Figure 5 below, PERI has experienced robust earnings growth over the years, with projections indicating a continuation of this trend in the future. From 2019-2022, PERI’s adjusted EPS surged at a CAGR of 44%, and expectations foresee an EPS expansion at a 14% CAGR through 2025. Despite macro headwinds, PERI has consistently demonstrated its ability to grow profitably. Furthermore, Perion Network is driving growth through innovation, exemplified by its recent offering – WAVE, a new advertising solution for dynamic audio ads powered by generative AI. This innovation is tailored to enhance personalization and engagement in the expanding U.S. digital audio ad market.

In light of the challenging macro backdrop, it’s worth noting PERI’s robust liquidity position, as demonstrated in Figure 6 below. The company holds $525M in cash and short-term investments and carries no long-term debt, signifying its remarkable financial fortitude.

Perion Network: A Diamond in the Rough for Investors

When evaluating companies for investment opportunities, it’s often a hunt for a diamond in the rough. In the case of Perion Network (PERI), it appears that we have found just that – a gleaming prospect that is both profitable and growing, presenting an enticing mix for investors, particularly those who are more risk averse.

Valuation & Estimates

Examining the numbers, it is evident that PERI is trading at a P/E of 9x currently, a significant 26% below its five-year average of 12.1x. Comparing PERI to its industry peers reveals that it is trading at roughly a 70% discount on a price-to-earnings basis. While some discount may be warranted due to its slower growth relative to its peers, we believe the current markdown is excessive, especially considering PERI’s strong net income margin profile compared to the competition.

Price Target Analysis

Estimating a 2025 adjusted EPS of $3.84, approximately 4% above consensus, we arrive at a price target of $46, representing a substantial 62% upside from current share price levels. Despite the discount necessary to reflect slower growth, this multiple is more than reasonable, given PERI’s historical trading and robust net margin profile.

A scenario analysis on price target outputs, based on different assumptions for EPS growth and the 2025 multiple, further supports the case for PERI’s potential.

Risks to Thesis

While PERI is positioned for strong growth and share price appreciation, we acknowledge some risks to the thesis. Market conditions deteriorating could potentially decrease available ad dollars, impacting PERI’s numbers for 2024 and 2025. Additionally, competition from tech behemoths like Alphabet (GOOGL) and Meta Platforms (META) raises the challenge of gaining additional market share over time, which could weigh on PERI’s stock price. Fortunately, PERI’s current profitability and growth set it apart from many young businesses in the space, affording confidence in its ability to sustain market share and experience solid share price appreciation in the future.

Final Thoughts

Given its expansive total addressable market, strong balance of profitability and growth, and attractive valuation, Perion Network emerges as a compelling buying opportunity in today’s market. With a diversified business model, focus on technological innovation, and robust execution, PERI’s resilience position makes it an attractive prospect for investors seeking stability and growth in the dynamic digital marketing industry. Therefore, we confidently assign Perion Network a Buy rating and set a $46 price target, suggesting over 60% upside potential from its current stock price.