In the unpredictable world of investments, uncovering a company selling at a bargain price is just the beginning of the journey to a potentially fruitful investment. Pfizer Inc. (PFE), a pharmaceutical giant, has languished in the doldrums for quite some time due to lackluster growth. The positive financial impact from its COVID-19 vaccines, Comirnaty and Paxlovid, is waning in the post-pandemic era. Last November, despite recognizing Pfizer’s undervaluation, the catalyst that could propel PFE stock to greater heights remained elusive.

A previous analysis noted the decline in Pfizer’s revenue and its failure to outperform market expectations. This underperformance has reflected in the stock price. However, recent developments have hinted at a potential turnaround.

The downtrend in earnings revisions since April 2022 has been a concern, with 20 negative revisions for Fiscal 2023 estimates against zero upward revisions in the last 90 days. However, the anticipation of Pfizer authorizing a share buyback program is generating optimism about future stock performance.

The Case for Share Buybacks Gains Strength

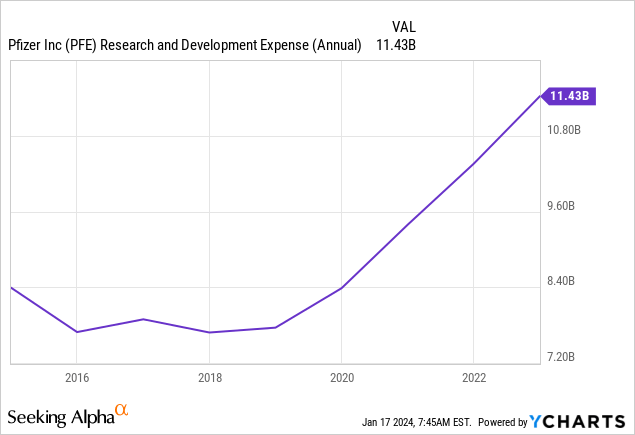

Pfizer’s last share repurchase was a $2 billion expenditure in early 2022. The company has been allocating its considerable cash from COVID-19 vaccine sales to acquisitions and research and development (R&D) efforts, with notable deals including the $43 billion acquisition of Seagen to expand cancer research and the $11.6 billion acquisition of Biohaven. R&D expenses have surged, signaling Pfizer’s commitment to new drug research and development.

Exhibit 1: Pfizer’s annual R&D expenditure

As 2024 unfolds, Pfizer is intensely focused on streamlining its cost structure while efficiently integrating newly acquired entities. CEO Albert Bourla has clearly delineated the company’s 2024 objectives, centered on enhancing efficiency, maximizing recent investments, and reducing debt.

Speaking at the J.P. Morgan Healthcare Conference last week, CEO Bourla disclosed four key priorities for 2024:

- Integrating Seagen into Pfizer’s business.

- Maximizing the performance of recently launched products.

- Improving operating margins through cost adjustments.

- Implementing a shareholder-friendly capital allocation decision framework.

Bourla emphasized the importance of capital allocation, highlighting dividend growth, debt reduction, investment for the business, and share buybacks as key priorities.

The CEO acknowledged the company’s accelerated business investments in recent years, hinting at a potential shift towards share buybacks. He stated, “In essence, you should expect 2024, after all the changes in the setup that we did in year ’23, to be a year of execution.”

Pfizer ended the last quarter with over $44 billion in cash and short-term investments against long-term total debt of $62 billion, emphasizing its strong cash generation. In the past 12 months, the company has raked in over $12 billion in operating cash flows.

The Silver Lining in Turnaround Prospects

Despite recent setbacks, Pfizer remains a compelling investment prospect. The company holds potential blockbuster drugs in its pipeline. Marstacimab, designed to treat a rare genetic blood disorder, could seize a significant market share.

Additionally, clinical trials for other promising drugs are underway. Pfizer’s expertise and extensive resources position it favorably to navigate through the complexities of drug development and regulatory approval processes.

The ongoing challenges and setbacks faced by Pfizer are reminiscent of past stumbling blocks encountered by successful companies. History has shown that periods of adversity can often be preludes to renewed vigor and success.

As Pfizer charts its course for 2024, investors are eyeing the possibility of a share buyback program as a potential catalyst for stock price appreciation. If successful, the buyback program could serve as a testament to Pfizer’s commitment to enhancing shareholder value and igniting fresh enthusiasm in the market.

Pfizer’s Resilience: A Closer Look at Its Future and CEO’s Confidence

Recently, the pharmaceutical giant Pfizer has been under the uninhibited gaze of investors, as it prepares for upcoming patent expiries in the U.S. The bittersweet symphony of the impending expiration, lauded for its inevitability, is not lost in the annals of history as Pfizer battles to maintain its allure and grasp a position that’s impervious to the menacing winds of change. Hemophilia, ABRYSVO for the prevention of RSV in infants, and Elrexfio for multiple myeloma have been stalwart contenders in Pfizer’s product portfolio, seamlessly gracing the narratives of blockbuster drugs. However, the tides of change are unforgiving, and the impending patent expiries serve as a clarion call for investors to be ever-vigilant in their pursuits.

Navigating the Patent Expiries

The impending patent expiries have cast a shadow of uncertainty over Pfizer, triggering a fervent vigilance among investors. The company stands at a crossroads, teetering between the obsolescence of once-profitable drugs and the promising allure of a burgeoning pipeline. The dueling forces of loss and opportunity beckon, paving the way for a strategic rejig that promises to redefine Pfizer’s trajectory in the years to come.

Leveraging the Scale Advantage

In the saga of corporate prowess, Pfizer stands distinct with its scale advantages, bestowing upon it the rare luxury of resilience. Unlike many of its peers in the biotech realm, the company revels in the opportunity to seize multiple shots at the goal, a privilege that is seldom bestowed upon its counterparts. Pfizer’s ability to tap into these advantages, fortified by a formidable track record in astute acquisitions, affords a potent shield against the adversities that loom on the horizon.

Parsing Through the Conservative Expectations

Pfizer’s expectations for 2024 are shrouded in a veil of conservatism, a plausible stance following the tumultuous fallout from its inability to meet lofty benchmarks in 2023. The echoes of uncertainty reverberate through the corridors of Pfizer as CEO Albert Bourla cautiously treads the path, apprehensive of overestimation. As the company gingerly navigates through the labyrinth of projections, the looming question remains – will Pfizer’s subdued forecast for Covid-related revenue stand the test of time, or will the unfolding events tip the scales in an unforeseen direction?

A Bet of Confidence from the Top

In a bold display of confidence, Pfizer’s CEO, Albert Bourla, has doubled down on the company’s future, epitomizing his unwavering faith with an unprecedented symbolic gesture. The declaration of vesting his entire pension in Pfizer stock speaks volumes, placing him “all in” with an unmistakable fervor that is often rare in the upper echelons of corporate leadership. As shareholders witness this resolute affirmation, the stage is set for a narrative brimming with potential and fortitude.

A Time for Patient Accumulation

As the pendulum of opportunity swings to and fro, an air of anticipation ensues, beckoning investors to contemplate their allegiances and long-term prospects. The allure of accumulating Pfizer stock, accompanied by a seasoned wisdom and an unwavering gaze on the future, augurs well for those who heed the signs of change. The tantalizing prospects of a potential share buyback program, yet to unravel its full potential, serve as an enticing prospect for investors who are poised to embark on a journey propelled by foresight and patience.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.