ShockWave Medical, Inc. SWAV showcases a promising trajectory for growth, underpinned by its robust research and development (R&D) endeavors and emphasis on clinical exploration.

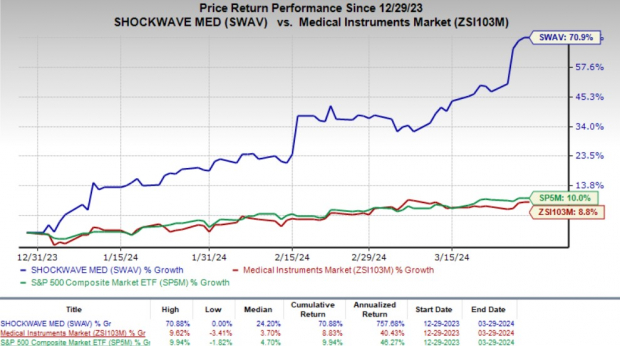

In a remarkable surge, the shares of this Zacks Rank #2 (Buy) entity have escalated by 70.9% year to date, dwarfing the industry’s 8.8% expansion. Concurrently, the S&P 500 Index has experienced a 10% uplift over the same period.

With a staggering market capitalization of $12.18 billion, this medical device titan remains steadfast in honing and commercializing products that aim to revolutionize the treatment of calcified cardiovascular disease.

Notably, ShockWave Medical boasts an earnings yield of 1.5%, which shines in comparison with the industry’s rate of 5.3%. The company has outstripped earnings estimates in three of the last four quarters, maintaining an impressive average surprise of 13.55%.

Image Source: Zacks Investment Research

The Driving Force Behind ShockWave Medical’s Triumph

SWAV channels resources into R&D initiatives to expedite the evolution of its Intravascular Lithotripsy (IVL) Technology, thereby enriching its product spectrum. During the fourth quarter of 2023, the company allocated $42.3 million towards R&D efforts, marking a substantial 78.4% leap from the prior-year quarter.

Projections for 2024 foresee revenue escalation of 25-27% year over year, reaching a substantial range of $910-$930 million.

Firm faith in its capacity to promptly craft innovative products underscores ShockWave Medical’s ethos. The company’s dynamic product innovation process, alongside the versatile nature and leveraging potential of its core technology, bolsters its R&D framework. In a notable breakthrough, SWAV disclosed favorable and consistent results pertaining to coronary IVL in both nodular and eccentric calcium settings in October.

Management exudes optimism regarding the enduring clinical endorsement and market penetration of IVL. With a robust demand for the C2+ device in global markets, the impending U.S. launch holds promise, fueled by the technology’s stellar performance in recent quarters.

Of particular note, the Centers for Medicare & Medicaid Services (“CMS”) have formally introduced enhanced Medicare Severity Diagnosis Related Group codes and payments for coronary IVL in the hospital inpatient sphere. These new coronary IVL-specific MS-DRGs carry higher remuneration when juxtaposed against the MS-DRG for alternative Percutaneous Coronary Intervention procedures.

Moreover, the CMS has instituted a Category I Current Procedural Terminology add-on code dedicated to procedures integrating coronary IVL. This novel categorization translates to a 20-30% upsurge in compensation for physicians spearheading coronary IVL procedures, auguring well for the uptake of ShockWave Medical’s products and buttressing top-line growth.

Simultaneously, the stock has been on an ascendant trajectory owing to speculations surrounding a potential acquisition from medical behemoth Johnson & Johnson. Such an offer could potentially include a premium on SWAV’s market price, heralding benefits for shareholders.

Challenges on the Horizon

Pertinent hurdles encompass limited commercialization expertise and the current array of approved or cleared products, posing a challenge in evaluating SWAV’s current operational framework and forecasting future financial growth.

Analyzing Projections

The Zacks Consensus Estimate for the company’s 2024 revenues stands at $920.9 million, signaling a 26.1% improvement from the preceding year’s reported figure. Concomitantly, the estimate for 2024 adjusted earnings per share rests at $4.89.

Exploring Alternative Investment Opportunities

Distinguished entities in the broader medical domain warrant attention, including DaVita Inc. (DVA), Cardinal Health, Inc. (CAH), and Integer Holdings Corporation (ITGR).

DaVita, bestowed with a Zacks Rank #1 (Strong Buy) currently, flaunts an anticipated long-term growth rate of 12.1%. The company surpassed earnings projections in all the preceding four quarters, delivering an aggregated surprise of 35.6%. DaVita’s shares have trended upward by 31.8% year to date, overshadowing the industry’s 9.9% surge.

Cardinal Health, holding a Zacks Rank of 2 presently, is poised for a projected long-term growth of 15.9%. The company surpassed earnings forecasts across the preceding four quarters, amassing an average surprise of 15.6%. Cardinal Health’s shares have witnessed an 11% appreciation year to date, surpassing the industry’s 7.3% hike.

Integer Holdings, securing a Zacks Rank of 2 at present, anticipates a long-term growth rate of 15%. The entity outshined earnings estimates in each of the trailing four quarters, delivering an average surprise of 11.5%. Integer Holdings’ shares have soared by 17.8% year to date, outperforming the industry’s 8.8% growth.

Wish to Discover More of Zacks’ Insights?

No joke.

Opportunities beckon with a mere $1 offering exclusive 30-day access to our array of picks. Thousands have seized this chance to explore our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators, and more, clinching profits from 162 positions with double- and triple-digit gains in 2023 alone.

Discover Stocks Now >>

Keen on the latest insights from Zacks Investment Research? Avail a complimentary download of 7 Best Stocks for the Next 30 Days. Click to access this free report here