Textron Inc. TXT, with its soaring earnings estimates and robust backlog, shines bright in the Aerospace Defense sector.

Discover the compelling factors that paint this Zacks Rank #2 (Buy) stock as a compelling addition to your investment arsenal.

### Reasons to Invest

Growth Trajectory & Historical Performance

Over the last 60 days, the Zacks Consensus Estimate for TXT’s 2024 earnings per share (EPS) leaped by 8.66% to $6.27. Anticipated total revenues for 2024 rest at $14.64 billion, signaling a 6.99% year-over-year growth.

Textron has demonstrated a remarkable (three to five years) earnings growth rate of 10.12%, punctuated by an average earnings surprise of 13.53% in the past four quarters.

Strong Fundamentals

With a current ROE of 16.05%, surpassing the industry norm of 10.51%, TXT showcases its adeptness at optimizing funds for superior returns—outperforming its industry peers in the process.

Growing Backlog and Investment

Textron’s thriving order book, boasting a $14 billion backlog by the close of 2023’s fourth quarter, underpins its stable position. Within the Aviation segment, a $7.2 billion backlog reflects a $782 million upswing from the previous year, driven by robust demand for innovative products dominating the global aviation industry.

The company’s planned capital outlay of $425 million for 2024 marks a resilient 5.7% increment from 2023’s $402 million.

Stability and Finance

As of the end of the fourth quarter of 2023, Textron boasts a solid times interest earned (TIE) ratio of 15.1. This robust ratio signifies its capacity to fulfill interest obligations without strain in the immediate future.

Moreover, TXT’s current ratio, resting at 1.92 by year-end 2023, ensures the company’s ability to address its short-term liabilities without impediments.

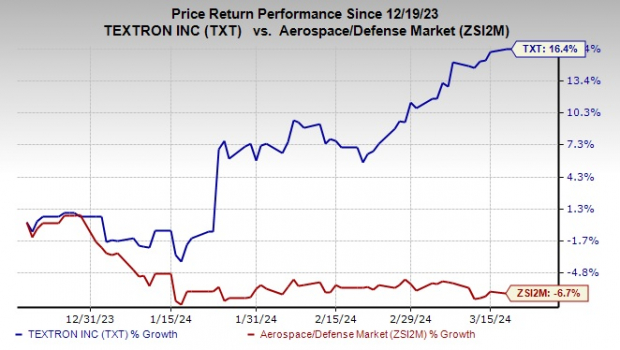

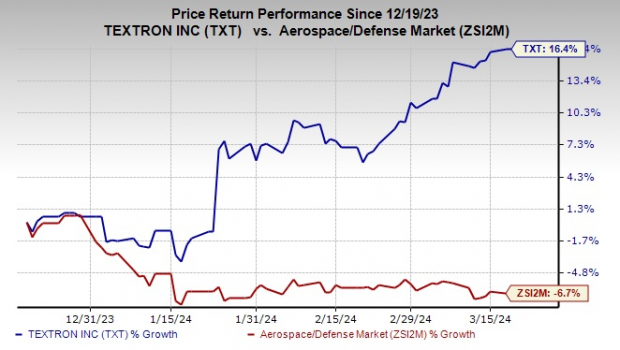

Financial Performance

Over the past quarter, TXT shares appreciated by a noteworthy 16.4%, shining in stark contrast to the aerospace defense industry’s average 6.7% decline.

Image Source: Zacks Investment Research

### Consider Other Compelling Options

Exploring Alternatives

Other standout selections within the sector include Leidos LDOS, Spire SPIR, and Safran SAFRY, each currently bearing a Zacks Rank #2. Peruse the comprehensive list of Zacks #1 Rank (Strong Buy) stocks here.

Leidos anticipates a long-term earnings growth rate of 8.12%, with a 2024 EPS consensus of $7.75, signaling a 6.16% increase year-over-year.

Spire has showcased an average earnings surprise of 28.01% in recent quarters, while its 2024 EPS consensus of a loss of 9 cents points to a remarkable 95.93% year-over-year surge.

With a long-term earnings growth rate pegged at 30.22%, Safran’s 2024 EPS consensus of $1.88 hints at a 48.03% uptick from the previous year.

### Don’t Miss Out on the Opportunity

Ready to Explore Further?

Stake your claim in the oil industry’s resurging landscape with Zacks Investment Research’s latest report on the Oil Market on Fire. Uncover four under-the-radar oil and gas stocks primed for substantial growth in the imminent months here.

Want to stay in-the-know with Zacks Investment Research’s latest findings? Download your copy of the 7 Best Stocks for the Next 30 Days report today here.

Textron Inc. (TXT) : Free Stock Analysis Report

Safran SA (SAFRY) : Free Stock Analysis Report

Leidos Holdings, Inc. (LDOS) : Free Stock Analysis Report

Spire Global, Inc. (SPIR) : Free Stock Analysis Report

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.