A. O. Smith Corporation Shows Growth Potential Amid Challenges

A. O. Smith Corporation (AOS) is experiencing growth due to strategic acquisitions and a commitment to research and development (R&D). The company remains dedicated to rewarding shareholders through consistent dividends.

Based in Milwaukee, WI, A. O. Smith is a prominent manufacturer of water heating and treatment products for both commercial and residential use. The company focuses on delivering innovative, energy-efficient solutions globally.

Now let’s explore the key factors that could enhance A. O. Smith’s market standing.

Strategic Expansion Initiatives

AOS aims to strengthen its market presence by enhancing its product offerings through notable acquisitions. In November 2024, the company acquired the Pureit business from Unilever. This integration adds Pureit’s water treatment expertise and brand recognition, allowing A. O. Smith to broaden its offerings and solidify its position within India’s water treatment sector. The company projects that this acquisition will generate approximately $50 million in sales for 2025.

Additionally, in March 2024, A. O. Smith acquired Impact Water Products, a privately held company that further extends its water treatment reach in North America. This acquisition is expected to bolster its market strategy in the region.

Investments in Research and Development

A. O. Smith is focusing on long-term growth by making substantial investments in R&D and manufacturing efficiency. In 2024, the company completed a new gas tankless water heater manufacturing facility in Juarez, Mexico. This move aims to mitigate newly imposed tariffs by relocating production from China. Furthermore, in early 2025, A. O. Smith inaugurated a commercial R&D testing laboratory in Lebanon, TN, designed to enhance the production capacity of water heaters and boilers. These initiatives clearly illustrate A. O. Smith’s commitment to innovation and operational efficiency, positioning the company for success in a competitive landscape.

Shareholder Rewards

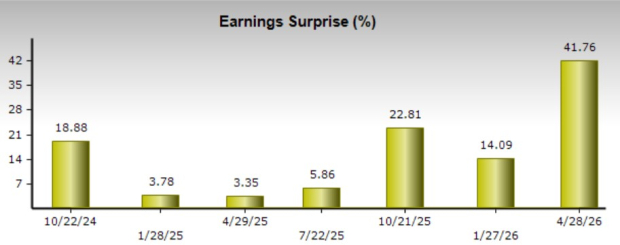

A. O. Smith continues to emphasize returning value to shareholders through share buybacks and dividends. In Q1 2025, the company distributed $49.2 million in dividends—an increase of 4% year over year—while repurchasing 1.8 million shares for $120.6 million. In October 2024, A. O. Smith raised its dividend by 6%, bringing it to 34 cents per share (an annual total of $1.36). As of the end of Q1, there were 5 million shares remaining under the existing buyback authorization. In January 2025, the board approved an additional buyback of 5 million shares, anticipating approximately $400 million in repurchases for 2025.

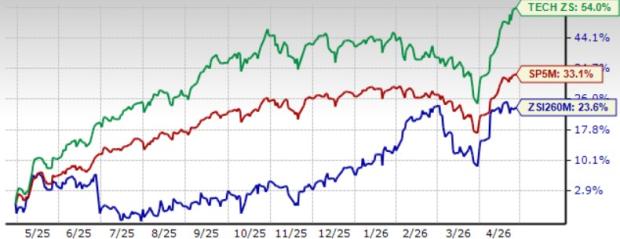

Shares of AOS have increased by 0.2% year-to-date, contrasting with the 3.5% decline in its industry.

Image Source: Zacks Investment Research

Potential Challenges for AOS

Business Pressures

A. O. Smith faces ongoing challenges within its segments. The Rest of the World division is grappling with decreased demand for residential water treatment systems and gas water heaters, particularly in China. In Q1 2025, this segment’s revenues remained flat year-over-year, with a 9% decline noted in Q4 2024. Similarly, the North America division saw a 7% drop in sales during the first quarter, raising concerns about order volumes for water heater products.

Foreign Exchange Risks

Operating internationally exposes A. O. Smith to geopolitical risks and unfavorable foreign currency fluctuations. A stronger U.S. dollar may compel the company to adjust prices or accept reduced profit margins outside the United States. For instance, adverse currency movements affected the Rest of the World segment, resulting in a $2 million revenue decline in Q1 2025 and a $13 million drop in 2024.

Stocks Worth Considering

Investors might want to explore the following companies with favorable rankings:

Crown Holdings, Inc. (CCK) holds a Zacks Rank #2 (Buy). The company has achieved a trailing four-quarter average earnings surprise of 16.3%. Over the last 60 days, the earnings consensus estimate for CCK in 2025 has increased by 3.8%.

AptarGroup, Inc. (ATR) also has a Zacks Rank of 2, and it reported a trailing four-quarter average earnings surprise of 7.3%. The earnings consensus estimate for ATR’s 2025 performance has risen by 4.3% over the past two months.

The Gorman-Rupp Company (GRC) carries a Zacks Rank of 2 and has a trailing four-quarter average earnings surprise of 2.4%. The earnings consensus estimate for GRC’s 2025 earnings has edged up by a penny in the last 60 days.

This article originally published on Zacks Investment Research.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.