Micron Technology has emerged as a key player in the AI market, outperforming major competitors like NVIDIA Corporation over the past year. The company, led by Sanjay Mehrotra, recently joined the trillion-dollar market-cap club and is capitalizing on the rising demand for high-bandwidth memory (HBM) chips used in AI infrastructure. Micron projects revenues of $33.5 billion for fiscal Q3 2026, a significant increase from $23.86 billion in fiscal Q2 2026, with an expected gross margin of 81%.

Meanwhile, Sandisk Corporation has also been making strides, with anticipated revenues of $7.75 to $8.25 billion for fiscal Q4 2026, up from $5.95 billion in Q3. Sandisk has reported a non-GAAP earnings per share of $23.41 for Q3 and expects between $30 to $33 for Q4, reflecting strong growth momentum driven by demand for memory products in AI-powered data centers.

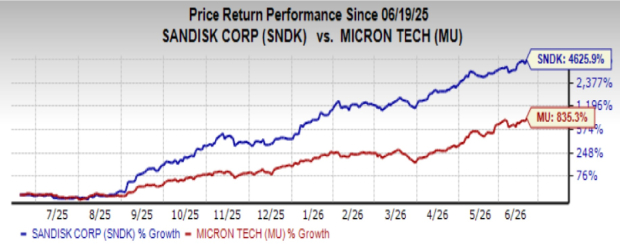

Sandisk’s forecasted earnings growth rate for the current year stands at an impressive 2096.7%, significantly above Micron’s expected 626.5% growth. Both companies are positioned to benefit from ongoing supply constraints in their respective memory chip markets.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.