Service Corporation International (SCI) has found success through increased revenues in its Cemetery segment and strategic capital investments. These moves have fortified the company, yet Funeral unit sales lag. The waning impact of rising deaths, along with high interest rates, may hinder bottom-line growth in 2024.

For 2024, SCI projects EPS, excluding special items, within $3.50-$3.80, compared to the $3.47 reported in 2023. Although management foresees a return to the typical earnings per share growth range of 8%-12% in 2025.

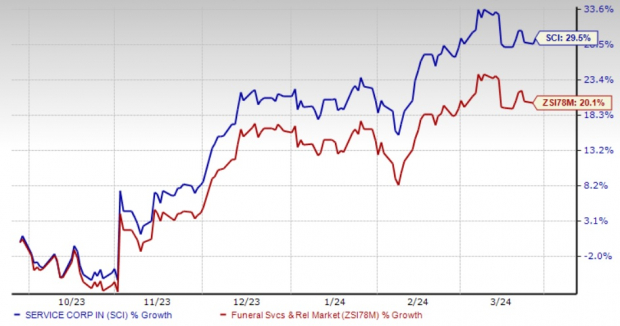

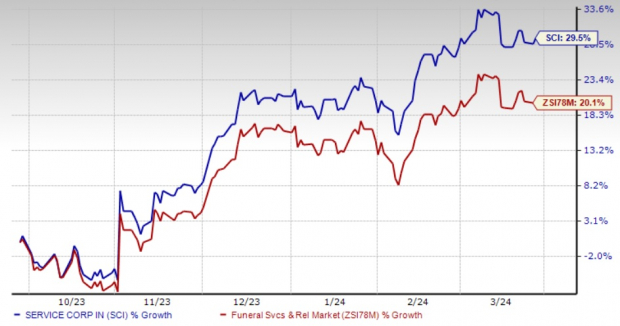

The stock of this Zacks Rank #3 (Hold) company has surged by 29.5% over the past six months, surpassing the industry growth of 20.1%.

Strengths at Play

Service Corporation remains committed to bolstering its network through capital investments. The company is modernizing its funeral locations, updating venues for a contemporary feel. Additionally, management is diversifying its cemetery inventory to cater to both casketed and cremation consumers, creating a broad customer base

During 2023, SCI spent $631.8 million on capital expenditures, focusing on cemetery development and digital investments among others. The management highlighted a robust acquisition pipeline during its fourth-quarter earnings call. By constructing new funeral home facilities and cemeteries in high-growth areas, SCI is expanding its market share.

Image Source: Zacks Investment Research

The company expects total maintenance capital expenditures of $325 million for 2024, covering investments in facilities, cemetery projects, digital initiatives, and corporate ventures. Additionally, $75-$125 million is earmarked for acquisitions in 2024.

SCI has witnessed a continuous uptick in Cemetery revenues. The fourth quarter of 2023 saw consolidated Cemetery revenues hit $482.6 million, up from $447.5 million a year earlier. Comparable cemetery revenues rose by 7.7%, mainly driven by a $31.5 million growth in core revenues.

Core revenues surged due to the rise in total recognized preneed revenues, offset by a slight dip in at-need revenues. Comparable preneed cemetery sales production increased by 9.4%, propelled by robust large sales activity and higher core production sales average.

These factors position SCI well for growth despite short-term concerns.

Current Hurdles

In the fourth quarter, Funeral revenues for SCI stood at $573.2 million, down from $580.2 million in the previous year. The decline can be attributed to lower core revenues resulting from reduced at-need revenues. Total comparable funeral revenues dropped by 2.2%, primarily due to a fall in core funeral revenues.

The diminishing impact of heightened deaths, including those from the pandemic, affects funeral numbers and at-need cemetery revenues, slightly curbing the anticipated growth in preneed cemetery sales production. Moreover, the prevailing higher interest rates, especially in the initial months of the year, may hinder SCI’s earnings growth outlook for 2024.

Sturdy Consumer Staple Contenders

The Chef’s Warehouse (CHEF), a specialty food product distributor and a Zacks Rank #2 (Buy), boasts a trailing four-quarter earnings surprise of 3.2%. The Zacks Consensus Estimate implies sales and earnings growth of 8.7% and 4.7%, respectively.

Vital Farms Inc., offering pasture-raised foods, currently holds a Zacks Rank #2. With a trailing four-quarter average earnings surprise of 155.4%, estimates suggest sales and earnings growth of 18.6% and 35.6%.

Utz Brands Inc., a salty snack manufacturer with a Zacks Rank #2, reports an average trailing four-quarter earnings surprise of 2.6%. Earnings are expected to grow by 15.8% this fiscal year.