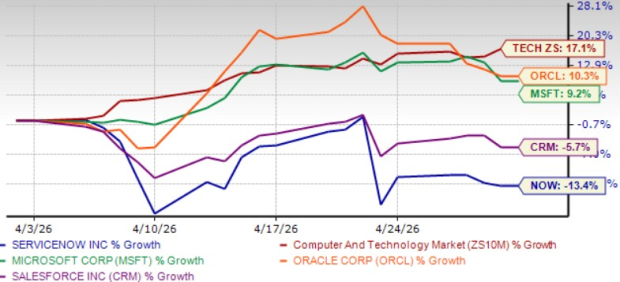

**ServiceNow (NOW) experienced a 13.4% decline in share value over the last month, significantly underperforming the Zacks Computer and Technology sector’s 17.1% return. This drop is attributed to macroeconomic and geopolitical challenges, particularly the delayed closing of several large on-premise deals in the Middle East, which has impacted first-quarter 2026 subscription revenue growth, projected at 22% year-over-year.**

**For the second quarter of 2026, ServiceNow anticipates subscription revenues between $3.815 billion and $3.820 billion, indicating year-over-year growth of 21-21.5%. The company’s 2026 revenue guidance has been raised to between $15.735 billion and $15.775 billion, reflecting a 20.5-21% growth rate. However, the subscription gross margin is facing headwinds from acquisitions, with significant contributions expected from AI-driven solutions, which are projected to generate approximately $1.5 billion in revenue.**

**Despite these growth strategies, ServiceNow’s shares currently trade at a premium, with a forward price/sales ratio of 5.35. Analysts project a steady consensus estimate of $4.14 earnings per share for 2026, suggesting a 17.95% growth compared to 2025. Investors are advised to adopt a cautious stance, as geopolitical challenges and competition remain significant concerns.**

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.