Snowflake SNOW is set to report its first-quarter fiscal 2025 results on May 22.

The Zacks Consensus Estimate for the top line is pegged at $786.95 million, suggesting year-over-year growth of 26.19%.

The consensus mark for the bottom line is pegged at 17 cents per share, up by a penny over the past 30 days, indicating 13.33% year-over-year growth.

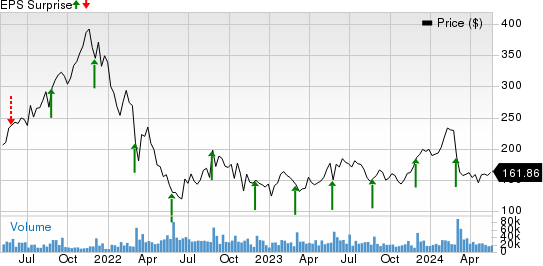

The company’s earnings beat the Zacks Consensus Estimate in the trailing four quarters, the average surprise being 129.25%.

Snowflake shares have declined 29.7% since the fourth-quarter earnings release (Feb 28, 2024) against the broader Zacks Computer & Technology sector’s return of 7.1%.

Snowflake Inc. Price and EPS Surprise

Snowflake Inc. price-eps-surprise | Snowflake Inc. Quote

Nevertheless, we believe that Snowflake shares are attractive at the current level due to an innovative portfolio, a strong partner base and an expanding clientele.

Snowflake currently has a Zacks Rank #2 (Buy) with a Growth Score of A, a combination that offers a good investment opportunity, per the Zacks proprietary methodology. A Momentum Score of B makes SNOW further attractive to investors. You can find the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Strong Portfolio Aids Prospects Amid Challenging Conditions

SNOW has been suffering from challenging macroeconomic conditions, including persistent inflation, which have hurt its customer spending patterns. Although bookings grew meaningfully in the fiscal fourth quarter, reflecting an improved macroeconomic environment, the consumption trend is expected to have been sluggish.

However, Snowflake has been riding on an expanding portfolio. Snowpark is expected to contribute 3% to product revenues in fiscal 2025. Product revenues are expected to be $3.25 billion, indicating 22% year-over-year growth for fiscal 2025.

The growing adoption of Snowpark by data scientists and engineers is expected to have aided the company’s top-line growth in the to-be-reported quarter. For first-quarter 2025, Snowflake expects revenues between $745 million and $750 million, implying year-over-year growth between 26% and 27%.

Newly introduced solutions, including Cortex, a new fully-managed service making AI simple and secure, Streamlit in Snowflake, Snowpark ML Modeling API, and Cortex ML functions, are expected to have benefited top-line growth. SNOW has an innovative portfolio that includes Document AI and Cortex, which are expected to be in public preview soon, strengthens growth prospects.

An expanding partner base, which includes the likes of Mistral AI, NVIDIA NVDA, Microsoft MSFT, Amazon AMZN, ServiceNow, Cognizant and Dell Technologies, has been driving Snowflake’s growth trajectory.

Snowflake’s partnership with Microsoft enabled product integrations across AI, low code/no code application development, data governance and more. Snowflake-Microsoft integration is empowering data scientists and developers with industry-leading AI solutions, building integrations between the Data Cloud and Azure ML, and leveraging integrations with Azure OpenAI and Microsoft Cognitive Services.

Snowflake-NVIDIA partnered to help businesses harness their data for Generative AI based on the NVIDIA NeMo platform for developing large language models and NVIDIA GPU-accelerated computing.

Moreover, this March, Snowflake inked an expanded collaboration with NVIDIA that brings together the full-stack NVIDIA accelerated platform with the trusted data foundation and secure AI of Snowflake’s Data Cloud.

Additionally, Snowflake’s achievement of FedRAMP high authorization on the AWS GovCloud now enables it to handle sensitive and classified data for the Federal Government. This accomplishment enhances Snowflake’s credibility in serving government entities.

In fourth-quarter fiscal 2024, Snowflake added 83 customers, with product revenues exceeding $5 million in the trailing 12 months, increasing from 75 customers in the third quarter. The trend is expected to have continued in the fiscal first quarter.

However, higher investments in AI-related initiatives are expected to drive the cost of revenues. Increased consumption-based commissions worth roughly $30 million are expected to hurt profits in fiscal 2025.

Conclusion

Snowflake’s strong portfolio, with the growing adoption of solutions like Snowpark, significantly boosts its prospects. Despite macroeconomic headwinds, we believe that an expanding partner base enhances its attractiveness to investors.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Snowflake Inc. (SNOW) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.