Humana’s Recent Decline and Future Potential

Humana (NYSE: HUM) currently trades at $350 per share, down 30% from its peak of over $500 in September 2022. Despite the fall, optimism surrounds the potential for the stock to rebound. The decrease in stock value can be primarily linked to a cautious guidance for 2024 and 2025. Revisiting the longer term, HUM stock has dipped by 15% since early January 2021, in contrast to the S&P 500’s 40% rise over the same period. The stock’s performance has seen fluctuations, with a 13% increase in 2021, a 10% rise in 2022, and an 11% decline in 2023.

The Challenge of Outperforming the Market

Outperforming the S&P 500 consistently has proven challenging for many stocks, including giants in the Health Care sector, as well as top players like GOOG, TSLA, and MSFT. The Trefis High Quality (HQ) Portfolio stands out as it has surpassed the S&P 500 year after year. The HQ Portfolio’s stable performance presents a compelling case for a balanced investment approach.

Considering the current economic uncertainty with soaring oil prices and elevated interest rates, the question arises: will HUM follow the pattern of underperformance witnessed in 2021 and 2023, or is a resurgence on the horizon? From a valuation perspective, HUM stock appears undervalued at $350, trading at 0.4x revenues compared to the 0.6x average over the last five years.

Weathering Economic Storms: Lessons from Historical Context

2022 Inflation Shock:

Reflecting on the tumultuous market conditions of 2022, Humana’s performance during the recent inflation shock paints a picture of resilience. In contrast, revisiting the 2007-2008 financial crisis sheds light on the stock’s ability to weather economic storms. During the crisis, HUM stock fell from $71 in September 2007 to $24 in March 2009 before staging a remarkable recovery to around $44 in early 2010, marking an 85% surge.

Fundamentals and Financial Resilience

Humana’s financials demonstrate strong growth, with revenues reaching $106 billion in 2023, up from $83 billion in 2021, driven by robust Medicare premium growth. Despite marginal fluctuations in operating margins and net income, Humana’s sound cash flow position, with a net debt positive balance, positions it well to meet its obligations during economic uncertainties.

The Road Ahead for Investors

As the Federal Reserve’s measures aim to stabilize inflation and rate cuts loom on the horizon, the outlook for HUM stock appears promising. With potential for upward movement once recession fears subside, Humana stands to benefit. Despite short-term apprehensions, Humana’s anticipated growth in Medicare Advantage membership offers a glimmer of hope for investors deliberating on the stock.

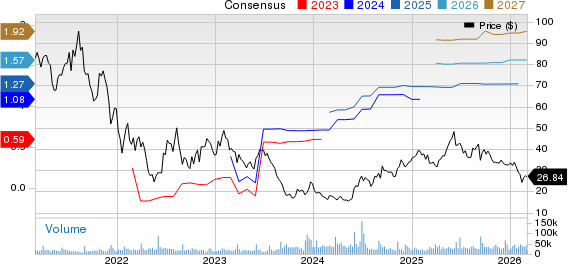

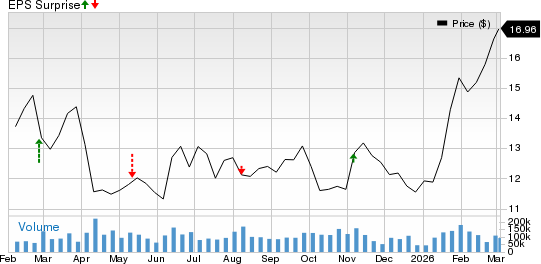

Humana Faces Challenges with Reduced EPS Estimates Despite Consistent Stock Performance

In the unpredictable world of stock performance, Humana has been a steady player, despite facing a recent setback in its estimated earnings per share (EPS). While the company maintained a strong position with an estimate of $16 adjusted EPS for 2024, this figure is a far cry from the $26 reported in 2023 and falls significantly below the consensus estimate of $29 per share. The primary culprit behind this decline can be traced back to the escalating medical costs ratio, which ballooned to 90.5% in Q4 of 2023 from 87.1% in the same quarter of the previous year. Unfortunately, Humana anticipates that this trend will persist throughout 2024.

A Stock Exchange Roller-Coaster

Despite these challenges, Humana’s stock is currently trading at 22 times the anticipated 2024 earnings, in line with its average valuation over the past three years. However, a more optimistic picture emerges when we shift our focus to the estimated earnings for 2025, which stand at $25, bringing the price-to-earnings ratio down to a more attractive 14x. Although the current scenario seems gloomy, there is a glimmer of hope on the horizon.

Weathering the Storm

It appears that much of the pessimism surrounding Humana’s future prospects has already been factored into its stock price. The potential for a turnaround lies in the hands of the company itself – if Humana manages to surpass its earnings projections or improve its medical cost ratio in comparison to the current guidance, investors could witness a surge in the stock’s value. In the volatile world of stocks, the slightest hint of positive news can send prices soaring.

Peer into the Crystal Ball

While Humana strives to navigate these turbulent waters, it is beneficial to scrutinize how the company’s performance stacks up against its peers. By evaluating metrics such as returns, investors can gain valuable insights into the company’s standing within the industry. Comparison with industry peers offers a broader perspective that extends beyond individual company performance.

| Returns | Mar 2024 MTD | 2024 YTD | 2017-24 Total |

| HUM Return | 0% | -23% | 72% |

| S&P 500 Return | 2% | 9% | 131% |

| Trefis Reinforced Value Portfolio | -1% | 3% | 635% |

[1] Returns as of 3/20/2024

[2] Cumulative total returns since the end of 2016

As Humana moves forward, investors should keep a watchful eye on how the company’s performance unfolds in comparison to industry benchmarks. The journey ahead may be riddled with obstacles, but for the savvy investor, every dip in the roller-coaster ride presents an opportunity for growth.

Invest with Trefis for market-beating portfolios and comprehensive price estimates to steer your investment journey in the right direction.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.