imaginima/E+ via Getty Images

Earnings Expectations

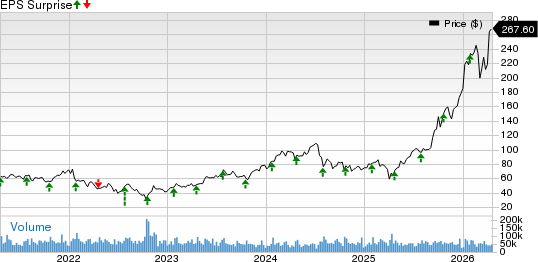

- Oilfield services provider SLB (NYSE:SLB) is scheduled to announce Q4 earnings results on Friday, January 19th, before market open.

- The consensus EPS estimate is $0.83 (+16.9% Y/Y) and the consensus revenue estimate is $8.94B (+13.2% Y/Y).

- Over the last 2 years, SLB has beaten EPS estimates 100% of the time and has beaten revenue estimates 63% of the time.

- Over the last 3 months, EPS estimates have seen 2 upward revisions and 16 downward. Revenue estimates have seen 13 upward revisions and 3 downward.

- The company on October 20 reported mixed Q3 results, topping consensus earnings estimates by a penny while total revenues came in roughly as expected.

- SLB has a Quant rating of “HOLD“, with a 3.09 rating score.

- SLB has an industry ranking of 13 out of 46 among oil and gas equipment and services stocks, as per SA’s Quant ranking.

- Wall Street rates the SLB stock “BUY” and Seeking Alpha authors rate it “HOLD“.

- In 2023, SLB stock rose 3%, while the S&P 500 Energy Sector Index fell 4.8%. The benchmark S&P 500 Index rose 24.2% for the year.

- Stock is down 7.5% so far this year as of Wednesday’s close.

Market Analysis and Predictions

Recent commentary on SLB includes a report by SA contributor Richard Durant, who stated that “even in the face of softening oil markets, Schlumberger’s business could continue to benefit from investments offshore and in international markets. Economic weakness in Europe and China, along with an end to OPEC supply cuts, pose threats to Schlumberger’s business though. Schlumberger appears fairly valued given near-term risks but should do well if economic conditions remain resilient.”

In a report on oilfield services providers, Goldman Sachs mentioned that going into Q4, it believes investors will be focused on reconciling lower 2024 activity expectations in international and offshore, management commentary on pricing power in North America pressure pumping and contract drilling, read-across from E&P customers on production expectations, and idiosyncratic drivers of estimate revisions. Goldman said it preferred SLB for international exposure.

“Overall, we expect North America activity to be down ~9% y/y and international and offshore to continue to grow at 10-11% in 2024,” they added.