In the backdrop of the impending 2024 U.S. presidential election, the financial markets are rife with anticipation as investors brace for potential policy alterations that could send tremors across the trading landscape. Amidst the prevailing spotlight on electric vehicle (EV) stocks and steel producers, the understated yet potent candidate for post-election prosperity hails none other than Nasdaq, Inc (NDAQ), the unbridled force propelling the esteemed Nasdaq Stock Market.

Highlighted by Bank of America Securities’ discerning analyst Craig Siegenthaler, the resurgence of IPO listings in the election aftermath could herald a windfall for the exchange operator. However, in a compelling maneuver, as asserted by the analyst in his recent dual upgrade of the stock, Nasdaq remains undervalued as it continues to masquerade as a cut-price exchange operator, even as its trading business merely accounts for 19% of its revenue.

The Lucidity of Nasdaq Stock

Anchored in New York and entwined in the financial fabric since its inception in 1971, Nasdaq, Inc. (NDAQ) stands tall as a tech titan boasting a formidable market cap of $41.2 billion. Revered as the world’s pioneering electronic stock market, Nasdaq orchestrates trading and clearing services across various asset classes.

Operating through three pivotal segments, Nasdaq’s Capital Access Platforms arm peddles and disseminates real-time market data and analytics, while its Financial Technology wing showcases tools such as Verafin for fraud detection and AxiomSL for risk management. The Market Services division steers the ship for the legacy exchange and marketplace activities.

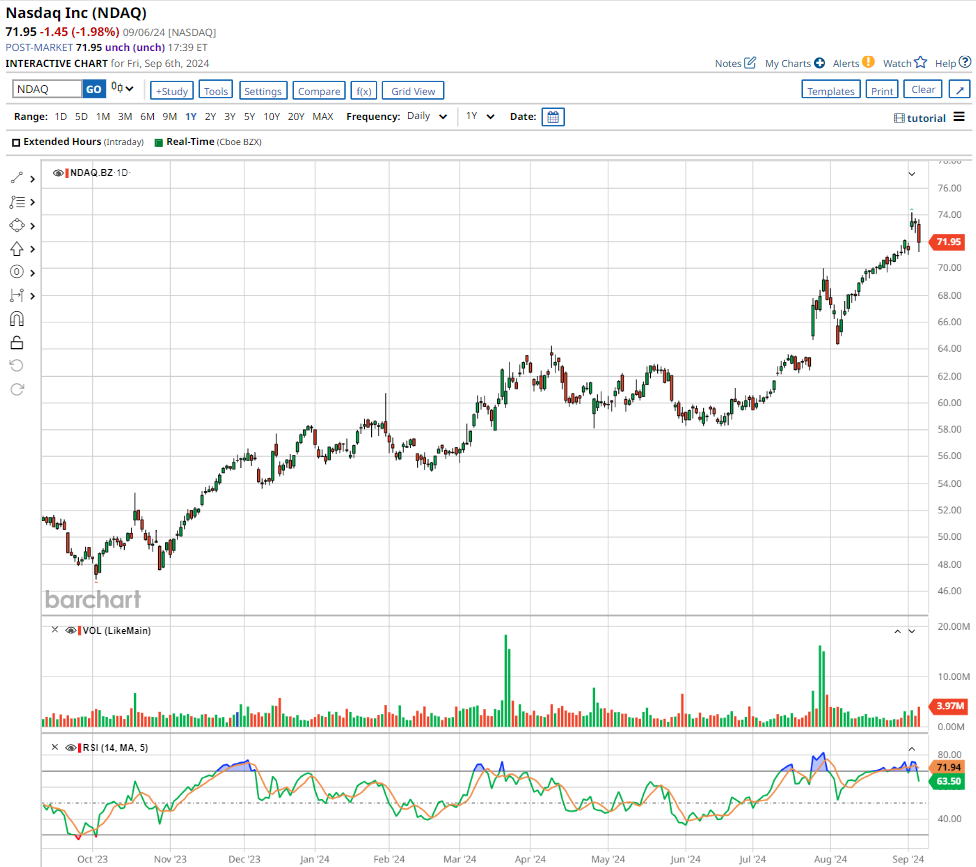

Over the bygone 52 weeks, NDAQ has galloped ahead by 39.5%, including a recent sprint of nearly 21% over the last three months alone. The stock soared to an unprecedented zenith of $74.17 on September 4.

Traded at 26x forward earnings, NDAQ’s stock is comparably valued to peers like Intercontinental Exchange, Inc. (ICE) – a pricing facade that belies the intrinsic value of Nasdaq’s operational model, as underscored by BofA’s Siegenthaler. With the lion’s share of revenue stemming from its high-growth FinTech and Capital Access Platforms domains, the analyst prophesizes an imminent re-evaluation of NDAQ stock.

The Melodious Rhythm of Nasdaq’s Dividend Journey

In the second quarter, Nasdaq rewarded shareholders with a $138 million dividend payout alongside a $58 million stock repurchase, while simultaneously extinguishing a $174 million term loan. As of June 30, $1.8 billion lay untapped under the ongoing buyback mandate.

Bearing testimony to Nasdaq’s dedication to shareholders is its streak of eleven consecutive dividend hikes. On July 25, Nasdaq’s board sanctioned a quarterly dividend of $0.24 per share, slated for disbursement to shareholders on September 27.

The annualized dividend of $0.96 per share translates to a 1.34% forward dividend yield. Furthermore, with a modest 33.2% dividend payout ratio, Nasdaq adeptly balances rewarding shareholders while stockpiling ample earnings to fuel its growth trajectory.

Nasdaq’s Ascent Post-Q2 Earnings Triumph

NDAQ stock surged by 7.2% on July 25 following a formidable display in its fiscal Q2 earnings report that left Wall Street awe-struck. Witnessing a 25% year-on-year surge, revenue skyrocketed to $1.16 billion, although adjusted EPS dipped by a marginal 3% to $0.69, edging past estimations by a noteworthy 7.8%. Solutions revenue catapulted by 34% to $901 million during the quarter.

In a strategic move, Nasdaq’s acquisition of Adenza for a staggering $10.5 billion in 2023 metamorphosed its FinTech division into a vigilante combatting fraud and regulatory transgressions. As dividends materialized, the unit’s revenue soared by an astounding 79% – a commendable feat even excluding Adenza’s impact. This meteoric rise outpaced Nasdaq’s mid-term growth prognosis of 10% to 14%, significantly underscoring the precision of Nasdaq’s strategic blueprint.

Securing its 42nd consecutive quarter as the preferred launchpad for U.S. companies going public, Nasdaq flaunted a commanding 72% success rate among eligible operational entities in Q2, shepherding 31 IPOs that raked in excess of $3 billion.

Capital influx from operational cash flows amounted to a stout $460 million, propelling Nasdaq’s deleveraging endeavor. With a robust $440 million nest egg in cash and cash equivalents by June 30, Nasdaq stands fortified in its financial position.

Leading financial pundits tracking Nasdaq envisage a 2.8% year-on-year decline in profits to $2.74 per share for fiscal 2024, poised for an upswing to $3.10 in fiscal 2025.

Decoding Analyst Prognostications for NDAQ Stock

On September 4, BofA unfurled an exclusive double upgrade for Nasdaq stock, catapulting it from an “Underperform” stance to a resounding “Buy” endorsement. Commending the exchange and market intelligence stalwart’s expansive moat, analyst Siegenthaler lauds the towering growth prospects within its software and informational services realms.

“After navigating two years of modest single-digit EPS growth in 2022-2023, we anticipate a surge to 10%-15% EPS growth in 2025-26,” penned Siegenthaler in a note extended to clientele.

Redolent of burgeoning optimism, Siegenthaler revised NDAQ’s price target to an all-time Street pinnacle of $90, anchored on a forward earnings multiplier of 25x, soaring from the erstwhile 15x benchmark. This projection heralds an anticipated upswing of 25.4% from the closing bell on Tuesday.

Across the broader spectrum, NDAQ holds an overarching consensus of a “Moderate Buy” rating. Of the seventeen analysts tracking the stock, eight extol a “Strong Buy” narrative, while two advocate a “Moderate Buy” sentiment. The remainder of the aficionados, numbering seven, accentuate a “Hold” viewpoint.

Following the grandiloquent pronouncement by BofA, the discerning masses have now propagated a unanimous zilch “Sell” ratings for NDAQ.

As of the publication date, Sristi Suman Jayaswal does not hold any positions (either directly or indirectly) in any of the securities mentioned herein. All insights and data encapsulated in this piece are strictly meant for informational purposes. Please refer to the Barchart Disclosure Policy for further information.

The reflections and opinions delineated here are the sole viewpoints and beliefs of the author and may not necessarily mirror those of Nasdaq, Inc.