January saw more than 50 million retired workers bringing home an average monthly Social Security benefit of $1,909. While not making retirees wealthy, the benefits are instrumental in lifting over 15 million seniors aged 65 and over out of poverty annually.

An overwhelming majority of retirees rely on their monthly payout to make ends meet. Surveys over the past two decades have consistently shown that 80-90% of current retirees need their Social Security benefit to cover their expenses in some capacity.

Given the pivotal role of Social Security for aging Americans, the most anticipated event each year is the reveal of the cost-of-living adjustment (COLA) by the Social Security Administration (SSA).

Image source: Getty Images.

Understanding Social Security’s COLA Calculation

Social Security’s cost-of-living adjustment aims to maintain purchasing power for beneficiaries in the face of inflation. Before 1975, Congress arbitrarily passed COLAs, with the first one being passed in 1950. Since 1975, the COLA has been annual, calculated using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

The CPI-W tracks eight major spending categories and various subcategories, allowing it to derive a single figure monthly, facilitating easy comparison of price movements. Notably, Social Security’s COLA only considers CPI-W readings from the third quarter.

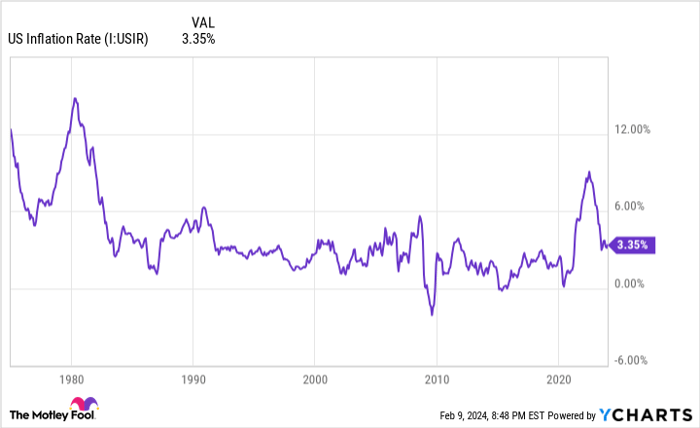

An elevated inflation rate has lifted Social Security’s COLA for three consecutive years. US Inflation Rate data by YCharts.

Potential for a Silver Lining in Social Security’s 2025 COLA

While we are some distance away from the crucial period, clues from non-calculation months suggest a potentially positive outcome for Social Security recipients.

Despite a decline in aggregate inflation rates, shelter, a major component of both the CPI-W and CPI-U, has remained persistently high. The soaring unadjusted 12-month inflation rate for shelter in December, at 6.2% for the CPI-U, indicates a possible higher COLA for 2025.

If the 2025 COLA reaches around 3%, as it hypothetically could, the average retired-worker benefit might rise by close to $60 per month in the upcoming year.

Image source: Getty Images.

Possible Downside to Social Security’s 2025 COLA

While a potential above-average COLA in 2025 would be welcome after a period of lackluster adjustments, the persistently high inflation rate for shelter could erode the purchasing power for retired workers, even with a higher-than-average COLA.

Historically, the purchasing power of a Social Security dollar has been declining, with studies showing a 36% drop since 2000. The current CPI-W fails to adequately reflect the expenses that matter most to retired workers, such as shelter and medical care, exacerbating this decline.

Lawmakers on both sides agree that the CPI-W is inadequate, but finding a bipartisan solution has been challenging, adding little hope for reversing this purchasing power loss anytime soon.

The $22,924 Social Security bonus most retirees overlook

If you’re like most Americans, you’re behind on your retirement savings, but “Social Security secrets” could provide a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more per year! Discover how to maximize your Social Security benefits here.

View the “Social Security secrets”

The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.