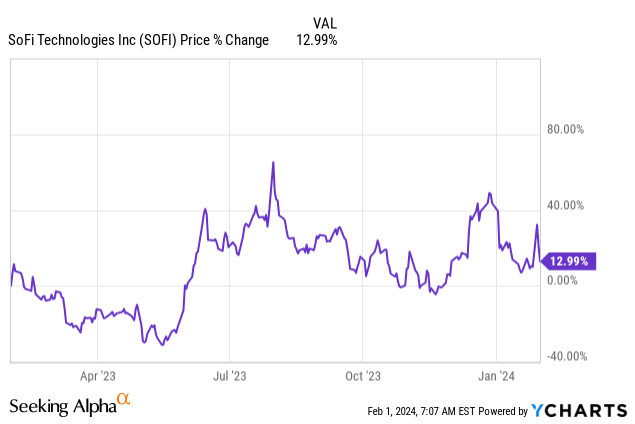

Shares of SoFi (NASDAQ:SOFI) soared more than 20% after the digital personal finance company submitted its earnings sheet for the fourth-quarter on Monday that showed both a significant EPS and top line beat. SoFi surrendered 15 percentage points of the upsurge on Tuesday and Wednesday, however.

The most notable take-aways from SoFi’s fourth-quarter earnings report were that the company’s revenue growth momentum accelerated and that the short term EPS outlook for SoFi is extremely favorable. The company expects consistent GAAP profitability in FY 2024 and with student loan payments resuming, I believe shares of SoFi have considerable upside revaluation potential!

Reaffirming confidence

I rated shares of SoFi a strong buy — SoFi Is Back — after the company’s third-quarter earnings due to an improving adjusted EBITDA

outlook in the context of resuming student loan payments (which turned out to be correct). SoFi also saw accelerating revenue growth and strong customer acquisition in the fourth-quarter which greatly exceeded my expectations. The guidance for FY 2024 looks impressive as well. I believe shares have continual upside potential as the market understands that SoFi offers both profitability and top line growth.

Impressive milestones and top line growth

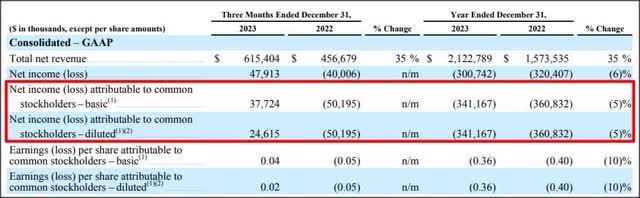

SoFi surpassed estimates for its fourth-quarter producing GAAP earnings of $0.02 per-share, beating the $0.00 per-share consensus. The top line also came in ahead of consensus expectations, beating the average prediction by $23M.

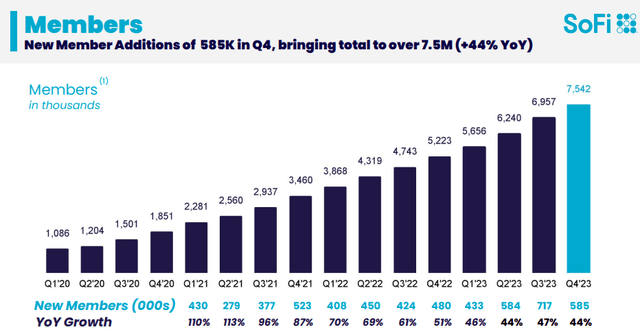

The personal finance platform had a great quarter in terms of customer acquisition as well: SoFi attracted 585k new customers to its platform in Q4’23 which marked a growth rate of 44% year over year and the firm ended FY 2023 with 7.5M accounts in its ecosystem. Although the growth rate, on a sequential basis, dropped 3 PP, the rate of customer acquisition was impressive and caused SoFi to report a 35% upsurge in revenues to $615.4M in Q4’23. SoFi generated 27% top line growth in Q3’23 so the Fintech benefited from an 8 PP acceleration in its top line quarter over

quarter.

Better than expected customer acquisition caused SoFi to crush my year-end account estimate of 7M by more than half a million, indicating that despite my already “optimistic” assumptions, growth at SoFi is even stronger than I projected. Because of the strength in customer acquisition and considering current momentum in account additions, I project that SoFi could grow to ~10M customer accounts by the end of this year.

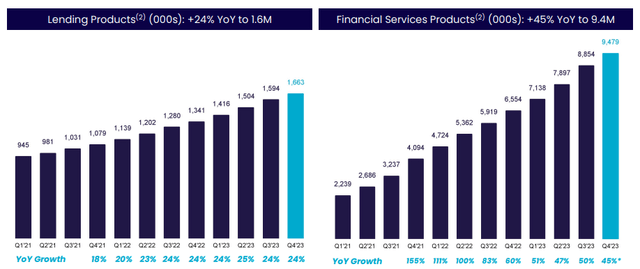

SoFi’s growth was chiefly driven by its Financial Services product category in Q4’23 which saw, in terms of products available on the SoFi platform, 45% year over year growth. This growth was almost twice as high as growth in Lending products (+24% Y/Y). Financial Services include insurance, investing and banking products, like Checking or Savings accounts. I expect, given the strength of grow in the FS category, that SoFi’s management will continue to prioritize investments in Financial Services in FY 2024 and beyond.

Surging profitability and financial success

SoFi’s adjusted EBITDA soared 85% Q/Q in the fourth-quarter to a quarterly record of $181M, driven by two major factors: 1. Strong growth in Financial Services, and 2. A rebound in originations in the student loan origination business (discussed below). SoFi’s demonstrated upside momentum in adjusted EBITDA as well as the fact that the Fintech is now GAAP profitable caused a major 20%+ stock rally on Monday that unfortunately faltered on Tuesday and Wednesday.

SoFi said that it would strive to achieve GAAP profitability for the first time ever in the fourth-quarter (something that a lot of naysayers didn’t believe was possible 1 or 2 years ago) and the company achieved its goal: the personal finance company reported a GAAP profit of $24.6M in Q4’23, showing a swing of $74.8M relative to the fourth-quarter of last year.

Resurgence in student loan originations

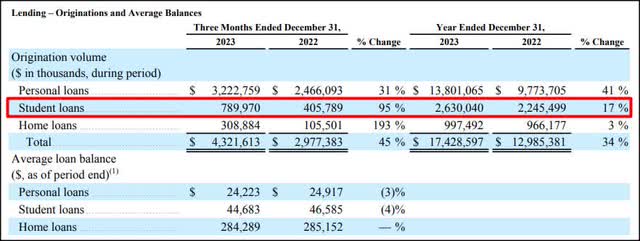

Although SoFi’s broad momentum can be traced back chiefly to its customer acquisition momentum and aggressive product growth in the Financial Services category, SoFi benefited from a huge turnaround in its student loan origination business as well. The student loan payment moratorium ran out in the fourth-quarter, resulting in a reinvigoration of the student origination segment.

Student loan originations soared 95% year over year in Q4’23 to $790.0M as student loan borrowers were once again required to make loan payments after a more than 3-year pause due to COVID-19. Personal loans replaced student loans as the primary driver of origination growth last year: student loan originations dropped off 48% year over year in FY 2022, but saw a decent rebound in FY 2023 (+17% Y/Y). Since student loan payments just resumed, I expect continual upside momentum in the coming quarters for this origination segment.

SoFi’s Impressive Growth Projections and Investment Potential

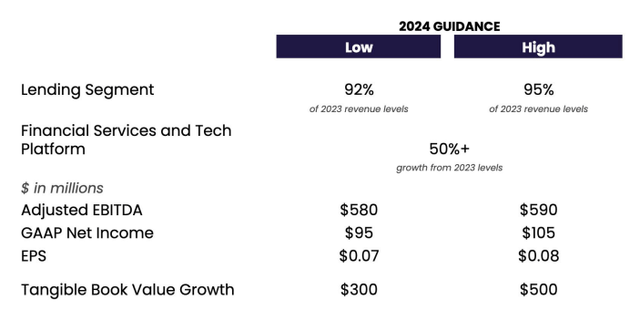

SoFi has set a lofty bar by releasing its guidance for FY 2024. The company’s outlook for the current fiscal year, particularly in the Financial Services category, forecasts a remarkable 50% segment top-line surge. This promising projection hints at a prospective $100M in GAAP profits, firmly establishing SoFi’s profitability.

Guidance for FY 2024

SoFi’s outlook for the current fiscal year is impressive as the company seeks to double down on its momentum in Financial Services… which is expected to lead to a 50% segment top line jump. SoFi also expects to generate $100M, at the mid-point, in GAAP profits this year which implies a $440M+ swing in profitability between FY 2023 and FY 2024. Since SoFi has now achieved enough scale to be profitable, I see strong earnings surprise potential for the personal finance company this year.

SoFi’s Valuation and Upside Potential

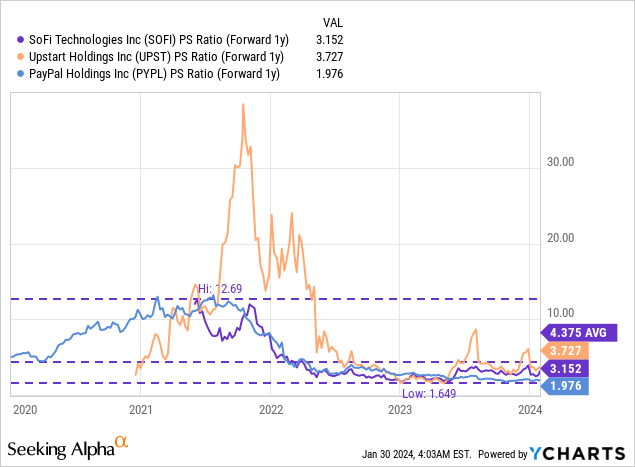

I believe SoFi has achieved a pivotal milestone by attaining profitability. The company’s anticipated expansion in profitability for FY 2024, especially driven by the Financial Services category, positions it for substantial growth. With estimated revenues expected to reach $2.7B in the current year and approximate $3.5B in the following year, a 4X revenue multiplier suggests a fair value market cap of $14.0B.

SoFi’s fair value is currently correlated to its customer acquisition strength and EBITDA momentum. Comparatively, a 4X P/S ratio appears reasonable given SoFi’s historical valuation and the trading ratios seen in the industry.

Risks with SoFi

The risk associated with investing in SoFi has notably diminished following the latest earnings report for the fourth quarter. Having exhibited profitable operations at scale, SoFi has addressed a significant portion of the concerns influencing its valuation in 2023. However, sustained momentum in customer acquisition, healthy GAAP income, and continued growth in the crucial Financial Services category remain critical factors to monitor.

Final Thoughts

SoFi’s latest earnings update effectively refutes the skeptics, indicating strong momentum with robust customer acquisition, accelerating top-line growth, and a promising financial outlook. The company’s commitment to expanding the Financial Services category demonstrates a clear growth strategy. Looking ahead, there is potential for a significant revaluation of SoFi’s shares if the company continues executing its growth plan with precision.