The revealing journey of a financial analyst

I embarked on my venture as an analyst at Seeking Alpha in 2021, armed with a modest yet growing knowledge of finance, complemented by my experience in logistics and data analytics. As I delved into analyzing companies in the shipping sector and expanded my research horizons across diverse industries, my insights evolved.

Now, let me share my thoughts on the overlooked global supply chain predicament that seems to evade the market’s attention, evident from the recent all-time high. The current state of global logistics may unfold into a surprising resurgence of inflation, one that the capital markets seem to underestimate or perhaps deliberately ignore.

A glimpse into today’s market expectations

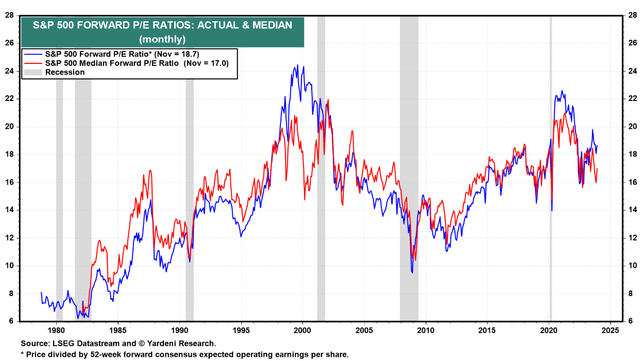

According to Yardeni Research data, the S&P 500 index (SPX) (NYSEARCA:SPY) (SP500) is presently trading at 18.7 times its 2024 earnings, approximately 11% below its 2021 peak, yet slightly surpassing its pre-2008 average. This infers that the index is trading at equitable levels.

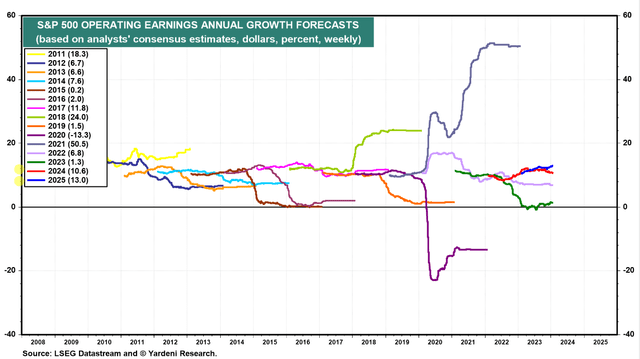

However, “equitable” does not signify that Mr. Market perceives a dearth of growth potential. Anticipations lean towards the continuation of the restoration of operating corporate earnings growth this year by 10.6% across the broad market. Consequently, if the current FWD multiple retains its “equitable” stance, the anticipated return for FY2024 should settle in the low teens.

Scrutinizing the index of small and mid-cap companies – Russell 2000 (IWM) – it persists at a substantial discount relative to historical averages. Accounting for the enhanced recovery in earnings, propelled by their preceding sharper decline, the projected return for this index could dwarf the return of SPY this year.

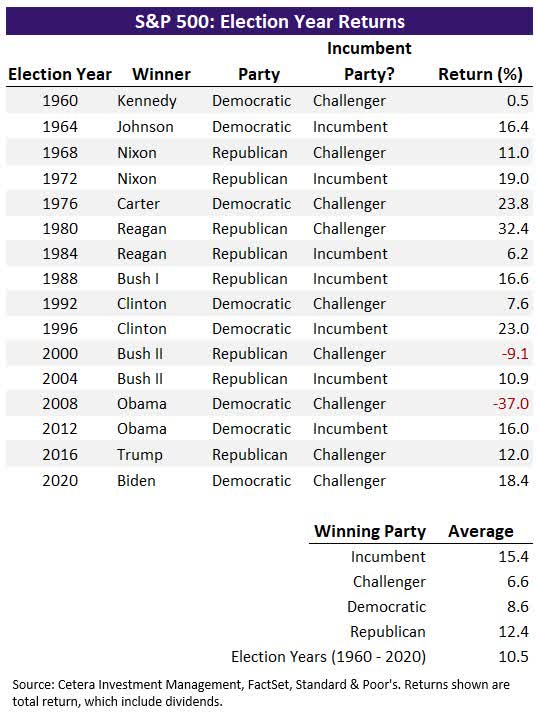

The market in 2024 will be significantly swayed by fluctuating interest rates (awaiting a downturn, but with differing viewpoints on its initiation: spring, summer, or even fall) and the forthcoming US presidential elections. Historically, the market exhibited volatility prior to the elections. Yet, it’s not inherently ominous: the S&P 500 yielded a positive total return in 14 of the last 16 election years, averaging a return of 10.5%, as per Cetera Investment Management:

Overall, things appear more than promising for SPY post its robust performance last year. However, these sentiments merely echo the consensus view. What kind of black swan am I alluding to in the article’s title?

The return of another shipping crisis and its inflationary implications

The Houthis, known formally as Ansar Allah or “Supporters of God,” emerged in the early 1990s as a militia advocating for the rights of the Zaydi branch of Shiite Islam. Gaining traction during the 2011 Arab Spring protests, they subsequently seized Yemen’s capital, Sanaa, in 2014, intensifying conflicts with Saudi Arabia and precipitating a multifaceted crisis. This crisis, deemed the world’s most substantial humanitarian crisis by the U.N., has plunged Yemen into dire straits.

Despite lacking international recognition as Yemen’s lawful government, the Houthis wield control over substantial swathes of the country, including the strategically vital Bab el-Mandeb Strait. Besides their opposition to U.S. and Israeli influence in the Middle East, the group faces accusations of receiving military and financial backing from Iran and Hezbollah, allegations consistently refuted by Iranian and Hezbollah authorities.

The Houthi assaults on vessels traversing the Red Sea commenced late last year. The militants asserted that these attacks in the Red Sea were retaliatory actions amid the ongoing Gaza Strip conflict.

A few weeks later, this Red Sea predicament appears to exert a more significant influence on shipping than the early pandemic:

Sea-Intelligence analyzed current vessel delays vis-a-vis delays over the past years in a report for clients. The data delineates that the prolonged transit around the Cape of Good Hope, as vessels divert from the Red Sea, is already impacting the availability of vessels to retrieve containers from ports more significantly than during the pandemic. In industry parlance, this phenomenon is termed “vessel capacity.”

The vessel capacity decrease ranks as the second most substantial in recent years, as per Alan Murphy, CEO of Sea-Intelligence. The sole event with a more pronounced impact than the Red Sea crisis was the “Ever Given,” the colossal cargo ship that lodged in the Suez Canal for six days in March 2021.

Source: CNBC

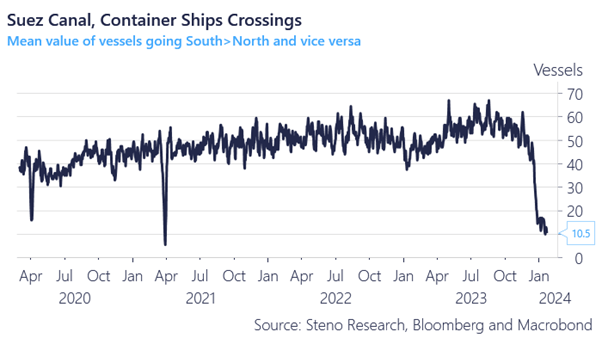

Looking at current statistics on the median number of ships traversing the Suez Canal, a staggering decline to levels last recorded in the first half of 2021 is observable:

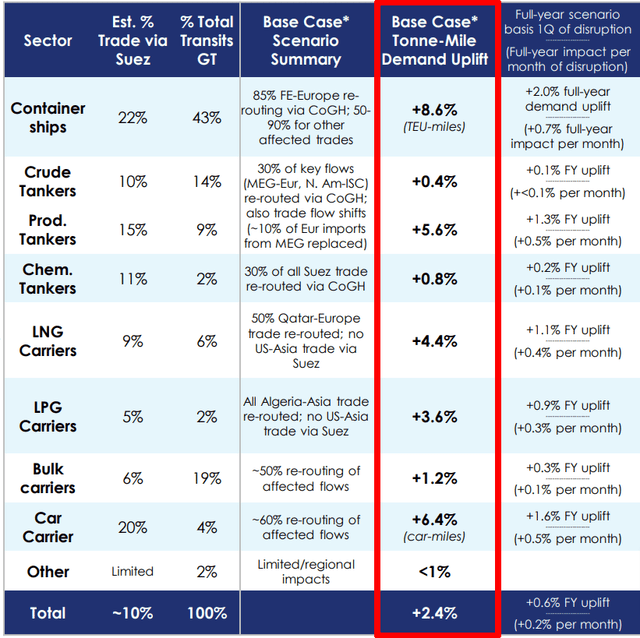

Operators are compelled to seek alternate routes to bypass perilous areas, primarily navigating through the Cape of Good Hope. Clarkson’s assessments reveal a sharp upsurge in tonne-mile demand for this rerouting:

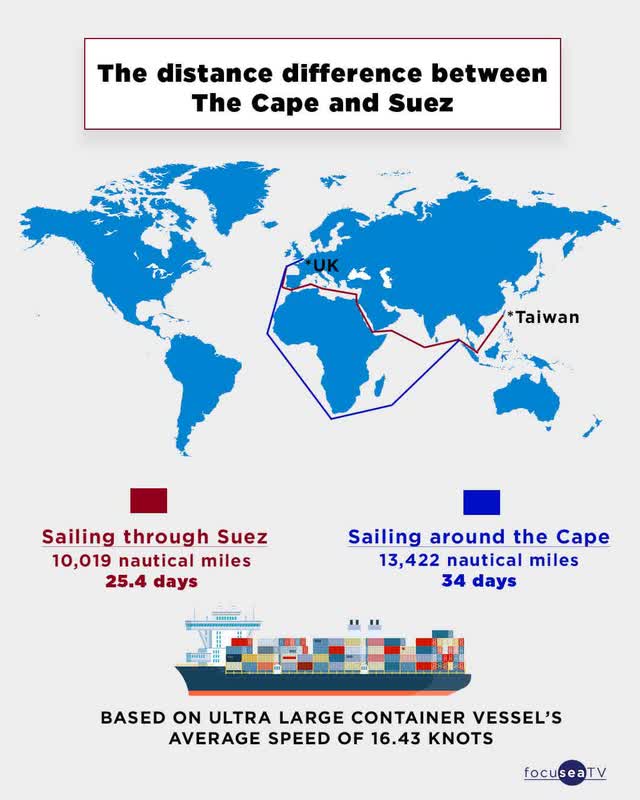

To comprehend the difference in transit time: ships now cover approximately 34% more distance at the same average speed (using a ULCV as an example):

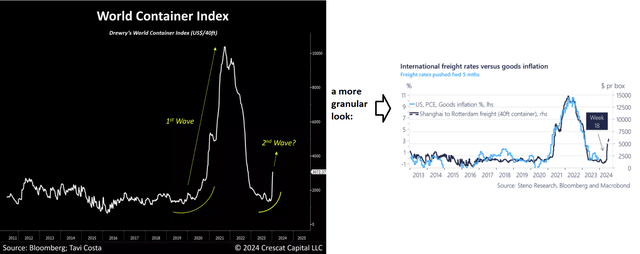

The Resurgence of Inflation and Its Impact on Freight Costs

The surge in transportation costs is reverberating through the economy, fueling inflationary pressures, and challenging conventional wisdom. While conventional metrics and forecasts suggest a decline in inflation, the current landscape tells a different story.

Inflation, as an economic gauge, extends beyond mere transportation costs. A seemingly innocuous surge in freight expenses permeates all aspects of economic interaction. The correlation between inflation and escalating freight costs is unmistakable, underpinning the gravity of the situation.

Private sector projections paint a sanguine picture, anticipating a sub-2.5% inflation rate by 2024. However, astute market participants are questioning the veracity of such cheerful expectations.

Source: Inflation Outlook For 2024 – Forbes Advisor

The prevailing market sentiment, evidenced by an 86.1% likelihood of the Fed slashing interest rates in May, may not align with reality. The repercussions of burgeoning inflation on consumer purchasing power and corporate profitability are cause for concern.

Navigating the Unforeseen

Distinguishing the present conundrum from the pandemic era unveils a critical nuance – the resurgence of vessel capacity. Historically, vessel capacity dwindles around the Chinese New Year, but the current scenario diverges. Abundant vessel availability counters the scarcity witnessed during the peak of COVID-induced disruptions, potentially assuaging the perturbation in global supply chains.

Industry reports indicate that approximately 10% of the global fleet lies dormant. Leveraging this surplus capacity presents an opportunity to redress the vessel availability asymmetry, offering respite for a beleaguered global supply chain.

Key Insights

Navigating the current geopolitical landscape’s impact on future inflation dynamics remains uncertain. Nonetheless, the incongruous market trends since mid-2023, given the palpable threat of resurging inflation, defy logic. While the stock market continues to exhibit fair valuation and individual companies promise growth, a prudent investment strategy demands a balanced portfolio that guards against unforeseen upheavals.

Indiscriminate divestment due to prevailing risks appears imprudent. However, exercising caution in portfolio allocation to avert an unwarranted equity overweighting is prudent amidst looming inflationary threats.

Safeguarding against this unforeseen black swan event is imperative, as we traverse these volatile times.

Good luck with your investments!