The Jewel of the Seas

Star Bulk Carriers Corp. (NASDAQ:SBLK) has cemented its position as a premier bulk carrier company with its fleet of 127 vessels, ranging from Ultaramax to Capesize. What further sets them apart is their fleet’s average age of 11 years and the fact that 94% of their ships are equipped with scrubbers. The recent collaboration with Eagle Bulk Shipping Inc. (EGLE) is set to elevate their standing even more, resulting in a combined fleet of 169 vessels, 97% of which will be scrubber-equipped.

The financials speak volumes about SBLK’s stability with $297 million in cash, total debt of $886 million, and $846 million in long-term debt. The impressive 42% gross margin, 23% EBITDA margin, and 11.3% ROE are a testament to their financial prudence. Moreover, with a 7.51% yield TTM, Star Bulk proves to be an enticing investment, especially given its modest valuation metrics.

Sailing the Seas: Supply Dynamics and Global Impact

In the realm of shipping, the supply side operates at a languid pace, akin to the gradual stride of a tortoise. The scarcity of shipyard capacity, the surge in aging ships, and the meager 8.1% order book for bulk carriers signal a looming period of limited fleet growth. The historical low order book reflects a dearth of new vessels, echoing the age-old tale of restrained supply paving the way for value creation.

The Panama Canal, a nautical crucible, bears immense significance in the global trade network. The dwindling water levels in the Gatun Lake, its financial artery, could pose a challenge by elongating shipping routes, thereby inflating demand, particularly for the transportation of Brazilian iron ore exports to the Far East.

With 15% of the iron exports destined for Asian shores, the pinch of a prolonged drought in the Panama Canal could amplify the ton-miles of demand, further galvanizing the prospects of bulk carriers like Star Bulk.

Forging New Horizons: The SBLK-EGLE Merger

Star Bulk’s merger with Eagle Bulk Shipping Inc. signifies a quantum leap in their voyage to dominance. The merger, set on an NAV basis, will result in the combined entity holding 71% and 21% stake for SBLK and EGLE shareholders, respectively. Not only does this merger augur a potent alliance, but it also offers an attractive 17% premium, underpinning the financial synergy entwined in this collaboration.

SBLK and EGLE Merger: A Maritime Powerhouse in the Making

The consolidation of SBLK and EGLE will birth a formidable force in the maritime industry, ushering in a new phase characterized by unmatched fleets. As the entities join hands, investors are set to witness the rise of a titan in the seas.

The Fleet Fusion

The merger will culminate in a company boasting one of the most enviable fleets, with SBLK poised to benefit from enhanced exposure to smaller bulkers such as Ultramax and Supramax, courtesy of EGLE’s 52 vessels at an average age of 10 years, a substantial 90% of which are equipped with scrubbers.

The pro-forma fleet, post-merger, will comprise 169 vessels, emphasizing effectiveness with an overwhelming 97% of the fleet incorporating scrubbers.

Robust Financial Performance

SBLK and EGLE have consistently delivered excellent results while maintaining prudent leverage, a trend well-evidenced in their EBITDA margin, Debt/Equity, and ROE as per the accompanying chart.

Insight into 3Q23

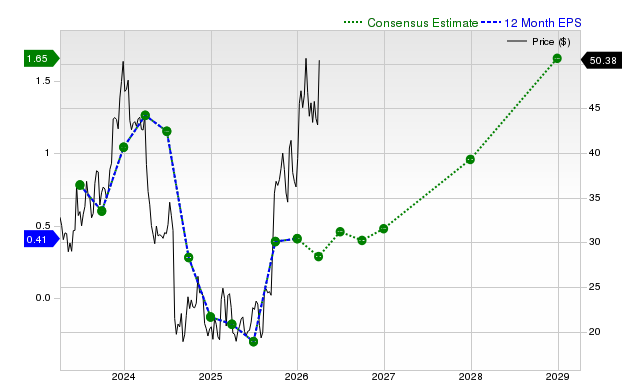

During the third quarter of 2023, SBLK recorded a net income of $44 million, translating to $0.46 EPS. The company also declared dividends amounting to $0.22 per share, signaling a robust financial standing.

Moreover, the average TCE stood at $15,068, with OPEX at $4,851. Notably, net cash and G&A expenses were recorded at $1,024 per day.

Strategic Business Moves

In a proactive move, SBLK divested 12 ships in the early months of 2023, realizing a handsome $272.5 million in gross proceeds, subsequently utilized for share buybacks.

Additionally, the company sealed two firm and two option contracts for 4 Kamsarmax vessels in October 2023, with scheduled deliveries set for 2025-2026, underlining its forward-looking approach.

Strategic Market Positioning

SBLK’s astute fleet coverage, as indicated in the detailed chart provided, is a testament to its shrewd positioning within the industry. With nearly two-thirds of its fleet securely fixed at $17,203 per day, the company holds a favorable position to capitalize on potential market shifts.

Foreseeing a situation where the Panama Canal might face obstructions, SBLK’s lower coverage of its Newcstlemax and Capesize vessels grants it a distinct advantage. In the event of increased demand for larger vessels, the company stands to realize higher day rates, reflecting its strategic prescience.

Financial Metrics Unveiled

Laying bare its solvency and liquidity metrics, SBLK stands firm, having significantly streamlined its balance sheet by reducing its debts, currently boasting $297 million in cash, with total debt and long-term debt amounting to $886 million and $846 million, respectively.

Fueling its robust liquidity metrics, the company posted $363 million in operating cash flow LTM and $230 million in operating income LTM, further bolstered by a net interest expense of $56.6 million.

Debt Structure

The detailed breakdown of SBLK’s current debt structure unveils a company that has navigated its financial obligations with deftness, entering strategic loan agreements to optimize its debt portfolio for sustained growth and stability.

In all, SBLK reaffirms its financial prowess, setting itself apart as a leader among its peers, a feat underscored by its robust gross profit.

Seaspan Corporation: Weathering the Storm in the Shipping Industry

Seaspan Corporation, a prominent player in the shipping industry, has demonstrated its mettle with strong financial metrics amid turbulent market conditions. The company’s recent performance, highlighted by robust EBITDA margins and Return on Equity (ROE), underscores its resilience in the face of sector-wide challenges.

SBLK, with a 42% gross margin, 23% EBITDA margin, and 11.3% ROE, has shown its ability to navigate industry headwinds. On the other hand, GOGL, with a younger fleet averaging 7.0 years in age, and EGLE, with a smaller fleet focusing on Supramax and Ultramax ships, have also displayed their unique positions, resulting in different margins and returns.

Assessment of Valuation and Price Action

To determine Seaspan Corporation’s value, investors are using P/NAV and relative valuation metrics. The company’s average fleet age of eleven years has been factored into the valuation, with 5% annual depreciation employed to estimate the cost of an 11-year-old ship.

- Ultramax/Supramax 11 years old, $22.9 million

- Panamax/Kamsarmax 11 years old, $21.9 million

- Newcastlemax/Capesize 11 years old, $33.3 million

- Current Assets: $495 million

- Total Liabilities: $1,359 million

- Seaspan Corporation market cap: $1,750 million

With SBLK’s Net Asset Value (NAV) calculated at $2,405 million, the P/NAV ratio is at 72%. This implies that for every dollar of net assets, investors are paying $0.72 at the current price. Comparison with industry peers such as Golden Ocean Group Limited (GOGL), EGLE, and Diana Shipping Inc. (DSX) demonstrates varied valuation metrics.

Seaspan Corporation trades at 2.56 EV/Sales, 6.72 EV/EBITDA, and 1.07 P/BV, positioning it midway amongst its counterparts. By comparison, GOGL emerges as the most expensive with 3.95 EV/Sales, 11.26 EV/EBITDA, and 1.08 P/TBV.

Analyzing price action, it’s notable that SBLK’s price is above the 20-month moving average, with local support at $16. The prevailing market conditions seem conducive for long positions, bolstered by favorable macro tailwinds and supportive price action.

Perspectives on Investment

Amidst prevalent sentiments favoring shorting shipping stocks and the underestimation of the Red Sea crisis, Seaspan Corporation’s low financial risk and robust solvency and liquidity metrics set it apart in the industry. With a flexible revenue structure leveraging time charters and voyage charters, the company has reportedly displayed superior margins compared to its prime competitors, GOGL and EGLE.

An attractive dividend yield of 7.51% further underscores SBLK’s solid position in the market. The planned merger with EGLE is expected to further enrich the company and create a formidable bulk carrier entity with a young and diversified fleet. In light of these factors, the macroeconomic environment, and a compelling value proposition, an affirmative sentiment toward taking a long position in Seaspan Corporation is gaining ground among investors.