Starbucks Surprises with Quarterly Earnings but Faces Challenges Ahead

Starbucks Corporation (SBUX) achieved better-than-anticipated results for the first quarter of fiscal 2025, with both earnings and net revenues exceeding the Zacks Consensus Estimate. Despite this positive outcome, there was a decline in the bottom line compared to last year, and revenues remained largely flat.

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

Performance Breakdown: Earnings, Revenues, and Comparisons

During the first fiscal quarter, Starbucks reported earnings per share (EPS) of 69 cents, surpassing the Zacks Consensus Estimate by 4.6%. However, this figure marks a decline of 23% from the 90 cents per share reported in the same quarter last year.

Net revenues totaled $9.398 billion, exceeding the consensus forecast of $9.3 billion by 1%. Last year during the same quarter, the net revenues were slightly higher at $9.425 billion.

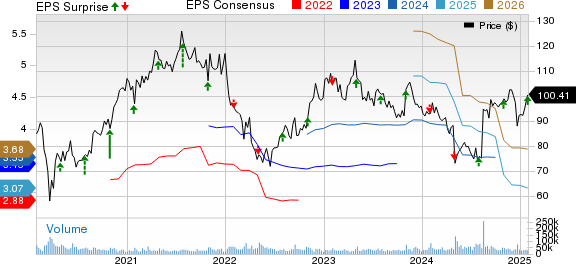

Starbucks Corporation Price, Consensus, and EPS Surprise

Starbucks Corporation price-consensus-eps-surprise-chart | Starbucks Corporation Quote

In terms of comparable store sales, the company saw a 4% decline year over year, a trend driven by a 6% drop in comparable transactions, even with a positive 3% rise in average ticket size. Starbucks opened 377 new stores globally, raising its total to 40,576 stores by the end of the quarter.

Operating Margins Reflect Pressure

For the quarter, Starbucks experienced a contraction in operating margin by 390 basis points (bps), landing at 11.9%. This decline was primarily due to increased operational costs associated with investments in the “Back to Starbucks” initiative and higher store operating expenses. Despite this challenge, some relief came from annualized pricing strategies and improved supply chain efficiencies.

When adjusted for constant currency, the operating margin decreased by 380 bps compared to the previous year.

Segment Performance Analysis

Starbucks categorizes its operations into three reportable segments: North America, International, and Channel Development.

North America: The segment recorded net revenues of $7.072 billion, down 1% year over year. Comparable store sales fell 4%, contrasting with a 5% increase in the prior year. The average transaction count declined by 8%, while the change in ticket size grew by 4% year over year. The operating margin shrank by 470 bps to 16.7%, below our projection of 16.3% for this quarter.

International: This segment’s net revenues reached $1.871 billion, experiencing a slight increase of 1% from the previous year. Comparable store sales also declined by 4%, with both transactions and ticket sizes decreasing by 2%. The operating margin fell by 40 bps to 12.7%, impacted by heightened promotional costs and strategic investments in store partner compensation. This result was short of our anticipated 13.7% margin for the quarter.

In China, comparable sales dropped by 6%, significantly down from a 10% increase seen in the prior year, largely due to a decrease in transactions and ticket sizes.

Channel Development: Net revenues in this sector dipped by 3% to $436.3 million, a result of reduced contributions from the Global Coffee Alliance and lower sales of ready-to-drink beverages. However, the segment’s operating margin improved by 90 bps to 47.7%, helped by a favorable product mix and reduced costs, though higher expenses in the North American Coffee Partnership weighed on overall performance.

Financial Position of Starbucks

As of the end of the fiscal first quarter, Starbucks held $3.671 billion in cash and cash equivalents, an increase from $3.286 billion at the end of fiscal 2024. Long-term debt slightly decreased to $14.312 billion from $14.319 billion as of September 2024, with the current portion of long-term debt remaining stable at $1.249 billion.

Starbucks announced a quarterly cash dividend of 61 cents per share, payable on February 28, 2025, to shareholders of record as of February 14.

Updates on Loyalty and Future Guidance

The Starbucks Rewards program reported 34.6 million active members in the U.S. over the past 90 days, reflecting a 2% increase from the previous quarter and a 1% rise year over year.

Guidance for Fiscal 2025

On October 22, 2024, Starbucks suspended its fiscal 2025 guidance but provided insight during the earnings call. The company anticipates lower EPS for the second quarter due to seasonal trends, organizational changes, and increased investments. Nevertheless, they expect an improvement in EPS in the latter half of fiscal 2025.

Starbucks also projects an increase in general and administrative expenses in the second quarter, which is attributable to several factors, including organizational restructuring costs.

Investors’ Outlook and Stock Performance

Currently, Starbucks holds a Zacks Rank #4 (Sell).

Fastenal and Darden Restaurants Face Mixed Results in Latest Earnings Reports

Fastenal Company (FAST) missed earnings and net sales expectations for the fourth quarter of 2024. Although their revenue increased compared to the previous year, profits remained unchanged.

Sales growth was largely driven by the expansion of Onsite locations, which serve customers directly at their facilities, and the increasing use of digital platforms. However, FAST encountered major obstacles, including a sluggish manufacturing market throughout 2024. A decline in demand for fasteners, which are crucial to its business, also limited growth. Despite these challenges, the company’s commitment to strategic initiatives such as digital transformation and customer service enhancements is expected to strengthen its market position over the long term.

Darden Restaurants, Inc. (DRI) revealed second-quarter fiscal 2025 results that showed a dip in earnings versus estimates, while revenues surpassed expectations. Both revenue and earnings improved compared to the same period last year.

During the quarter, sales increased by 6% from last year. This growth came from a same-restaurant sales boost of 2.4%, along with contributions from 103 Chuy’s restaurants and 39 new establishments. For fiscal 2025, same-restaurant sales are projected to grow by 1.5% year over year, with expected earnings per share (EPS) from continuing operations estimated between $9.40 and $9.60.

Spotlight on Chipotle: A Strong Contender

Chipotle Mexican Grill, Inc. (CMG) currently holds a Zacks Rank of #2 (Buy). The company is poised to achieve an impressive earnings growth of 14.3% in the fourth quarter of 2024. Chipotle has outperformed earnings estimates in each of the last four quarters, recording an average surprise of 9.8%.

Top Stock Picks for the Coming Month

Recently released: Experts have identified 7 select stocks from a group of 220 Zacks Rank #1 (Strong Buy) investments, labeling these as the “Most Likely for Early Price Pops.”

Since 1988, this comprehensive list has outperformed the market by more than double, generating an annual average gain of +24.3%. These carefully chosen stocks deserve your attention right away.

Fastenal Company (FAST): Get Your Free Stock Analysis Report

Starbucks Corporation (SBUX): Get Your Free Stock Analysis Report

Chipotle Mexican Grill, Inc. (CMG): Get Your Free Stock Analysis Report

Darden Restaurants, Inc. (DRI): Get Your Free Stock Analysis Report

Read more about this report on Zacks.com.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.