Stock Market Experiences Unprecedented Volatility Amid Tariff Changes

We are currently experiencing one of the most turbulent stock market climates in modern history.

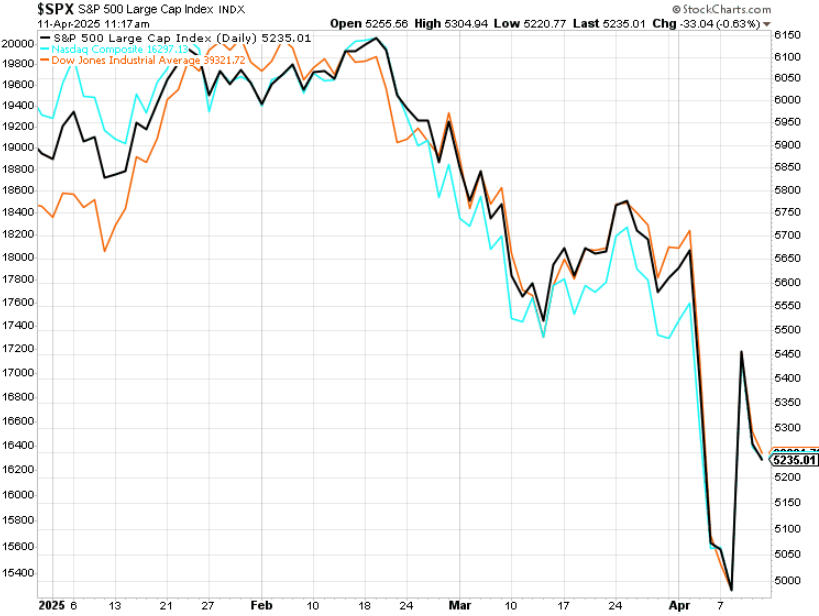

- From late February into early March, the market dropped 10% in just 20 trading days—marking one of the fastest corrections ever recorded.

- Following President Trump’s “Liberation Day” tariff announcement, the market fell another 10% in just two days; an occurrence that has only happened a handful of times in the past century.

- This was succeeded by a historic 8% rally due to news of a 90-day pause on tariffs, resulting in some of the biggest single-day gains on record.

- However, the market quickly reversed, plunging more than 3.5% the very next day as traders labelled the tariff pause as “signal over substance.”

- Simultaneously, the volatility index (VIX)—often referred to as the market’s fear gauge—has more than doubled, reaching levels seen only twice before in history: during the 2008 financial crisis and the 2020 COVID-19 lockdowns.

This situation is far from an ordinary market pullback; the term “whiplash” aptly describes the current scenario.

This upheaval aligns us with a rare historical precedent. Such erratic price movements have only occurred four other times in recent history: during the Great Depression, the onset of World War II, the 2008 global financial crisis, and the COVID-19 crash in 2020.

Today’s stock market turmoil echoes significant historical downturns.

But are we truly on the verge of a crisis resembling those times?

An Examination of Historical Context

The erratic price action in the market is sending a clear signal: “Prepare for a major event.”

However, it doesn’t seem to parallel the Great Depression closely. While the 1930s crash was exacerbated by the Smoot-Hawley tariff that raised average tariff rates from 13.5% to nearly 20%, triggering a global trade war, there are stark differences today.

In the ’30s, unemployment rates soared above 20%, banks frequently failed, and industrial production collapsed, all without the backing of a central authority equipped to stabilize the financial system.

Today, the unemployment rate hovers around 4%, banks are in relatively stable condition, and the U.S. Federal Reserve has substantial liquidity resources at hand. The economy, although experiencing slowdowns, is not in freefall.

Thus, it’s unlikely we are facing a scenario akin to 1930s America.

Much like the previous case, parallels to World War II also seem unfounded.

While global geopolitical tensions are indeed high—with a fraught U.S.-China dynamic and ongoing conflicts in the Middle East and Ukraine—there has been no indication of an imminent world-war-scale military escalation.

Concerns about global stability are real, but they are different from the conditions seen in 1939.

When we consider the 2008 financial crisis, the circumstances were distinctly different. At that time, the financial system was compromised, burdened with toxic assets and plummeting liquidity.

Currently, there are no indications of major financial institution collapses, nor is there a sudden loss of trust in lending practices.

This situation can be characterized as a policy-driven, market-instigated panic.

Current Market Dynamics

Turning to the recent COVID-19 pandemic, the current climate bears little resemblance to that crisis.

We are not experiencing sudden lockdowns, border closures, or immediate freezing of global supply chains as we did previously.

Instead, people continue to work, live, and travel.

While COVID-19 represented a black swan health crisis, today’s situation is rooted in real but exaggerated fears surrounding tariffs and their broader economic impacts.

We must acknowledge that these tariffs can be disruptive and harmful; however, they are not devastating.

According to Bloomberg Economics, even if reciprocal tariffs are fully enacted, the maximum average U.S. tariff rate would rise to about ~27% (compared to 2.5% last year). Fed modeling estimates this could lead to a 3.4% reduction in GDP.

This figure is certainly significant, but not catastrophic.

In contrast, the 2008 financial crisis resulted in an over 8% drop in U.S. GDP, with a similar impact during the COVID-19 downturn.

Even recognizing today’s tariffs may lead to a decline, it would only represent a fraction of those historical losses. Furthermore, we anticipate these measures will not remain in place permanently.

A Shift in Market Sentiment

Recently, President Trump announced a 90-day pause on reciprocal tariffs for all nations except China.

While the market reacted with skepticism regarding the lack of specifics, and the average tariff rate saw only a slight decrease from 26.85% to 26.25%, the broader implication is noteworthy.

We believe the most significant change lies in the sentiment shift—from escalation towards negotiation.

Since…

Trade Talks Begin: Market Optimism Builds for Stock Recovery

The pause in international trade discussions has illuminated a budding opportunity for investors. Here are some key updates:

- 70 countries have reportedly approached the White House for trade negotiations.

- 20 nations have submitted formal proposals.

- Two trade agreements are nearing completion.

- Former President Trump expressed confidence that the U.S. will finalize a deal with China.

With the initial tough rhetoric subsiding, negotiations are in progress. Once these agreements are set, the stock market could surge.

Reflection on Market Conditions from February

A look back at the stock market in mid-February reveals a strong economic backdrop. Prior to the onset of the trade war, equities had hit all-time highs, with the S&P 500 reaching 6150. Consumer sentiment was robust as inflation eased to 2.8% from 3.0%, and the AI Boom was accelerating, driving corporate earnings to stabilize with year-over-year growth of 17.8%—the highest since Q4 2021.

The market was not on the brink of collapse; it was in a phase of mid-cycle expansion. Though tariffs muddied the outlook, easing these tensions may reveal the original bullish thesis.

This presents a unique investment opportunity.

Navigating Today’s Stock Market

Although we anticipate further fluctuations, it’s clear that the stock market remains volatile. However, waiting indefinitely is not advisable. A 12-month investment horizon could reward those who buy stocks now, despite short-term uncertainty.

We believe that in a year, as the dust settles around trade agreements and the AI boom progresses, stocks will be significantly higher.

To navigate this turbulent market, consider a measured reentry strategy:

- Nibble on dips

- Focus on quality

- Buy high-conviction stocks

- Exercise patience

This approach will help investors succeed amid volatility.

Looking Ahead: Long-Term Market Fundamentals

This is not a repeat of historical market crashes such as 1930, 2008, or 2020. The current market environment is influenced by temporary headlines and volatile price actions, but the fundamentals are not signaling a collapse. Instead, they indicate challenges that are manageable.

The trade war’s impact will be mitigated through negotiations on tariffs, and the Federal Reserve may introduce cuts. Importantly, long-term market drivers—like AI, innovation, and productivity—remain active.

As Warren Buffett advises, this is a time to be greedy when others are fearful.

Rather than attempting to “catch the falling knife,” our focus is on riding the recovery. Once the market stabilizes, significant growth is projected.

When the moment arrives to buy the dip, stocks linked to AI 2.0 may offer paramount opportunities. This next generation of AI, capable of interacting with real-world environments, is at the forefront of industry interest.

The search for investment opportunities in humanoid robots is intensifying as technology companies recognize its potential. We have identified a strategic way to capitalize on this aspect of the AI evolution.

Learn more about our top AI 2.0 investment choice.

As of the publication date, Luke Lango does not hold any positions in the securities mentioned in this article.

Any questions or comments about this report? Reach out at [email protected].