AppLovin Corporation: A Rising Star in AI and Ad Tech

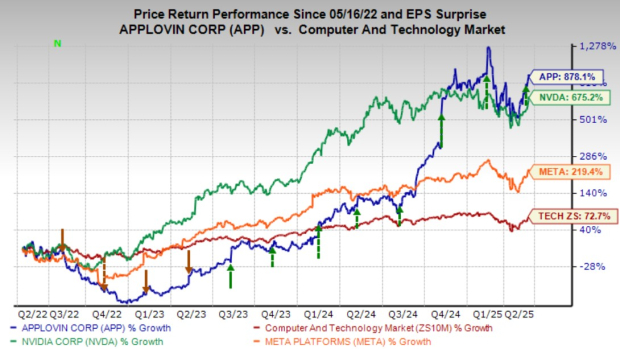

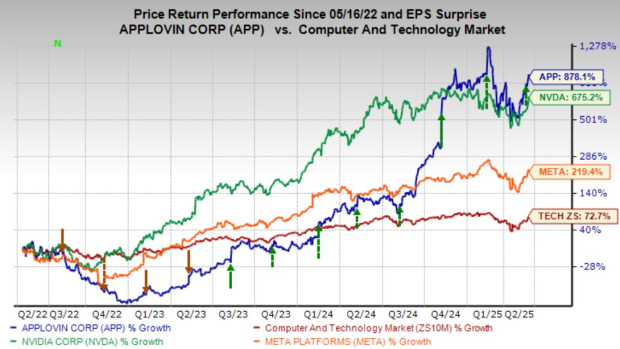

AppLovin Corporation APP has increased by 880% over three years, outpacing Nvidia and other leading stocks on Wall Street.

On May 7, APP delivered an impressive quarter with better-than-expected results as it continues to gain traction in the digital app monetization arena.

The company has also rebuffed various short-seller reports from earlier this year, showing resilience in its market position.

Despite its impressive performance, AppLovin remains on the higher-risk side of investments, as its valuation reflects this status.

As Wall Street renews its interest in growth sectors, including AI and innovative energy, APP appears to be a compelling buy, currently 30% off its all-time highs and 20% below its average price target according to Zacks.

Forecasts indicate strong double-digit growth in earnings and revenue for AppLovin in 2025 and 2026, as it diversifies beyond mobile gaming into sectors like media and finance.

Is AppLovin the Next Major Tech Player?

AppLovin’s extensive product range equips clients with crucial tools to succeed in the competitive digital app market.

Based in Palo Alto, the company’s AI-powered solutions help clients engage their target audiences “in-app, on mobile devices, across streaming TV, and beyond,” tapping into “1.4 billion daily active users.”

Image Source: Zacks Investment Research

Initially focused on mobile gaming, AppLovin has since broadened its reach to include finance, health, shopping, and more, aiming to be a central ad platform for direct-to-consumer businesses.

In 2021, APP nearly doubled its sales (+93%). However, growth slowed to 1% in 2022 as the digital ad market faced challenges, impacting major players like Meta.

Image Source: Zacks Investment Research

In Q2 2023, AppLovin launched its advanced AXON technology, leading to a 17% revenue increase and a shift to a profit of +$0.98 per share. Following that, APP recorded 43% sales growth in 2024, along with a 362% jump in EPS.

Growth and Profit Goals for the Future

AppLovin is focusing on five key areas for growth by 2025, including personalizing ad experiences using AI to create dynamic content tailored for individual users, enhancing engagement and response rates.

The company aims to transition from traditional “static” ads to a more dynamic, personalized advertising approach—an essential next step in the advertising industry’s evolution.

Additionally, AppLovin is committed to improving operational efficiency, with CEO Adam Foroughi stating a focus on optimizing headcount and harnessing growth opportunities.

Image Source: Zacks Investment Research

Through AI-driven automation and personalization efforts, AppLovin saw Q1 revenue rise by 40%, with adjusted earnings up by 150%, exceeding estimates.

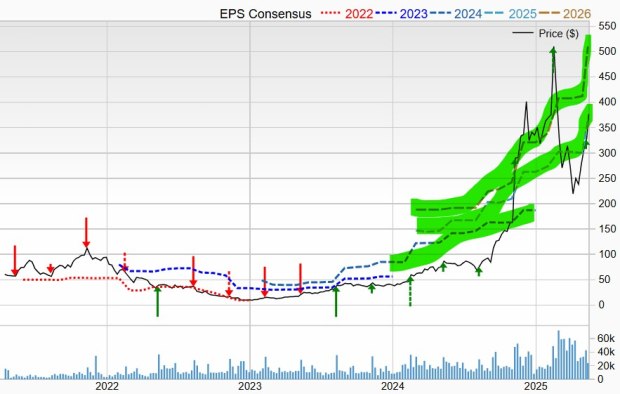

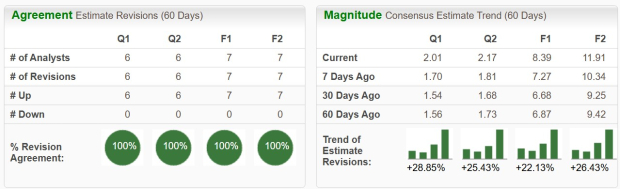

The Q2 earnings estimate for APP has surged 29% in recent months, with the 2026 forecast growing by 26%, earning the company a Zacks Rank #1 (Strong Buy). The EPS outlook has steadily improved over the past 18 months.

Projected revenue growth stands at 23% for 2025 and 21% for 2026, increasing from $4.71 billion in FY24 to $7 billion in FY26.

AppLovin Projects Strong Earnings Amid Short Seller Scrutiny

AppLovin’s Earnings Forecast

AppLovin is expected to see its earnings grow by 85% and 42% in the upcoming years, following a remarkable 362% growth in its bottom line in 2024. This trend is projected to increase AppLovin’s earnings per share (EPS) from $4.53 last year to $11.91 by FY26.

Short Seller Investigation

Recently, AppLovin has faced intense criticism from various short-seller reports that questioned the reliability of its AI-driven advertising platform. Reports from Fuzzy Panda Research and others surfaced between February and March, raising concerns.

These short sellers allege that the revenue generated by AppLovin is of poor quality, claiming it results from potentially illegal advertising practices.

In response, AppLovin has staunchly defended itself, asserting that it is “fully committed to defending the Company, its operations, and its reputation from those seeking to manipulate the market through false narratives.”

The company retained Alex Spiro from Quinn Emanuel Urquhart & Sullivan at the end of March to conduct an independent review and investigation into the short seller activity.

On May 7, while announcing its earnings, AppLovin disclosed it sold its mobile gaming segment to Tripledot Studios for $400 million, along with a 20% equity stake in Tripledot. This transaction allows AppLovin to shift focus to its higher-margin ad tech platform and streamline its operations amid ongoing scrutiny.

Investors might consider why AppLovin maintains a strong stock performance, with shares in the green for 2025 and a staggering 450% increase since its IPO, despite these allegations.

AppLovin’s Stock Performance Overview

Over the past two years, AppLovin’s stock skyrocketed 1,500%, rebounding after a steep decline in 2022, outpacing competitors like Nvidia, which saw a 360% increase, and Meta, which rose 170%. Since its April 2021 IPO, AppLovin’s stock has gained 460%, compared to tech’s overall 40% growth and Meta’s 100%.

The stock is currently up 12% in 2025, yet it remains 30% below its all-time highs and 20% beneath its average Zacks price target.

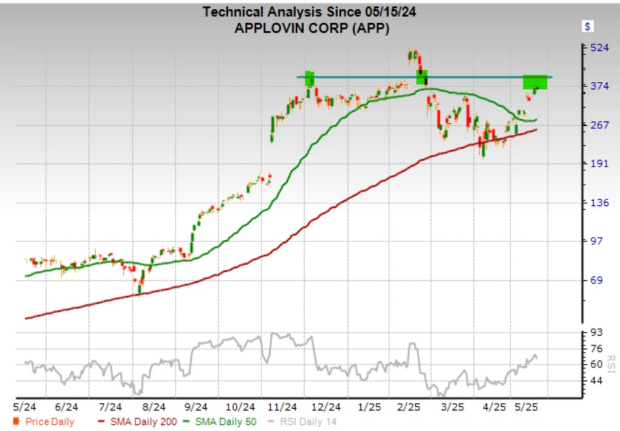

Image Source: Zacks Investment Research

If AppLovin can break above the previously mentioned trendline, it may reach new records. However, the stock is currently showing signs of being overheated on the RSI front, indicating it could decline to its 50-day or 200-day moving averages if market selling pressure mounts. A drop to those levels could present an attractive buying opportunity for investors and traders.

Image Source: Zacks Investment Research

From a valuation perspective, AppLovin’s stock is currently trading at a 90% discount to its historical highs and 50% below its recent peaks, at a forward P/E ratio of 41.8X. By comparison, the tech sector trades at 25.5X. Taking into account AppLovin’s significant earnings growth potential, its valuation aligns more closely with the sector’s Price/Earnings-to-Growth (PEG) ratio of 2.1, compared to the usual 1.7.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.