Fabrinet: A Hidden Gem in Tech with Strong Growth Potential

https://www.youtube.com/watch?v=TmiqQSqBRQU[/embed>

FabrinetFN is a key player for major tech companies, such as Nvidia, providing precision components used in AI data centers and telecommunications.

Over the past six years, FN has achieved an average revenue growth of 13%. Its earnings trajectory has been impressive, with Nvidia, a leader in AI data center chips, among its top clients, while a significant partnership with Amazon was established in mid-March.

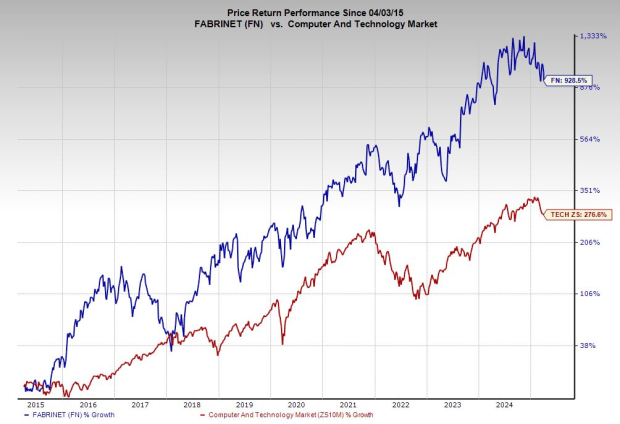

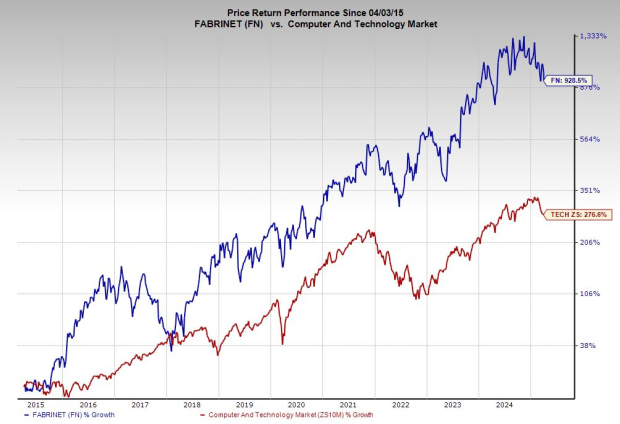

Since its IPO in 2010, Fabrinet has significantly outperformed the tech sector, tripling the sector’s returns. In the last three years, FN’s stock surged by 82% compared to the broader tech market’s 29% growth, all while trading at a discount relative to its sector, despite strong near-term and long-term performance.

Currently, Fabrinet is aiming to stabilize at a long-term moving average and is trading 30% below its all-time high.

Solid Reasons to Consider Fabrinet a Strong Buy

Fabrinet excels in advanced optical packaging, as well as electro-mechanical and electronic manufacturing services for original equipment manufacturers producing complex goods. Its products play a critical role as other tech firms strive to create intricate components needed for their devices.

In the backdrop of the growing demand from AI hyperscalers, Fabrinet’s technology enables rapid data transmission, essential for running AI programs effectively.

Image Source: Zacks Investment Research

NvidiaNVDA accounts for nearly 35% of Fabrinet’s FY24 sales. Other major clients include Cisco Systems and optical components leader Lumentum.

Recently, Fabrinet and AmazonAMZN formed a deal allowing Amazon to purchase warrants for up to 381,922 shares at $208.4826 each, encouraging Fabrinet to enhance its role in Amazon’s AI supply chain.

Over the past six years, FN has continuously enjoyed a revenue growth rate of 13%. Projections indicate an 18% revenue growth for FY25, followed by 12% growth in FY26, escalating from $2.88 billion in FY24 to an estimated $3.78 billion by FY26.

Image Source: Zacks Investment Research

Following its Q2 FY24 results, the consensus earnings estimates for Fabrinet have increased, leading to a strong Zacks Rank #1 (Strong Buy) for FN.

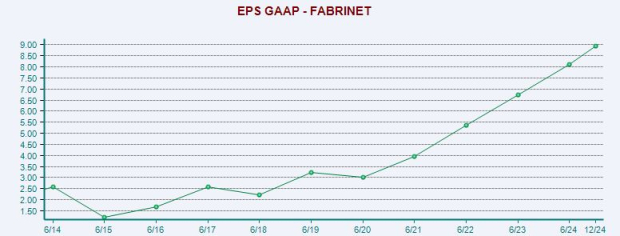

Expected adjusted earnings growth for Fabrinet is 16% in FY25 and 11% in FY26, following a 16% growth last year. FN has consistently exceeded earnings per share estimates.

Seize the Opportunity with Fabrinet Shares Now

Fabrinet’s stock has surged by 930% over the past decade, outperforming the Zacks Tech sector and matching Amazon’s impressive trajectory. Since its IPO in 2010, FN has jumped 1,700%, compared to a 590% increase in the tech sector.

Image Source: Zacks Investment Research

In the last three years, Fabrinet has risen by 82%, dwarfing the performance of the tech sector once again.

Despite this growth, investors now have the chance to acquire FN shares at a 30% discount from its previous highs. The company is working to establish support near its 21-month moving average, with Relative Strength Index (RSI) readings indicating some of the most oversold conditions seen since 2018.

Image Source: Zacks Investment Research

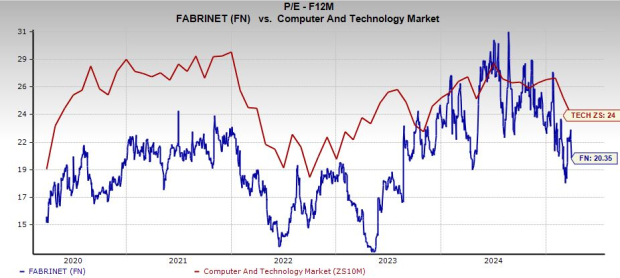

Valuation-wise, Fabrinet trades at a 15% discount to the tech sector and 35% below its all-time highs at 20.4X forward 12-month earnings. The stock, at its five-year median valuation in terms of forward earnings, has increased by 270%.

Fabrinet: A Key Player in the AI Technology Space

Fabrinet Positioned for Growth Amid AI Market Uncertainty

Fabrinet plays a vital role in the booming data center industry and the ongoing artificial intelligence (AI) revolution, which is expected to last for decades. Following a long-awaited selloff in AI stocks, investors now have the opportunity to purchase shares of Fabrinet (FN) at a more attractive price and valuation.

The company’s close connections with industry giants Nvidia and Amazon are likely to be advantageous as these firms continue to drive the AI arms race. Additionally, Fabrinet boasts a strong operational framework, as reflected in its balanced financial health. The company holds $935 million in cash and equivalents, significantly exceeding its total liabilities of $699 million.

Investment Insights: Market Projections and Future Opportunities

Zacks recently identified a top semiconductor stock, which is only 1/9,000th the size of NVIDIA. Since Zacks recommended NVIDIA, its stock surged more than 800%. While NVIDIA remains a strong player, this newly identified chip stock has greater potential for future growth.

With robust earnings growth and a widening customer base, this stock is well-positioned to cater to the soaring demand for artificial intelligence, machine learning, and the Internet of Things. The global semiconductor manufacturing market is forecasted to grow from $452 billion in 2021 to an impressive $803 billion by 2028.

For those interested in the latest stock recommendations from Zacks Investment Research, you can now download the report on the “7 Best Stocks for the Next 30 Days.”

Click here to access this free report.

For further analysis, you can find free stock reports on major players like Amazon.com, Inc. (AMZN), NVIDIA Corporation (NVDA), and Fabrinet (FN).

This article was originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.