U.S. Stock Market Bounces Back After Sharp Selloff

The S&P 500 Index ($SPX) (SPY) is up +0.92%, the Dow Jones Industrials Index ($DOWI) (DIA) is up +0.97%, and the Nasdaq 100 Index ($IUXX) (QQQ) is up +0.66%. December E-mini S&P futures (ESZ24) have risen +0.74%, while December E-mini Nasdaq futures (NQZ24) are up +0.40%.

Market Recovery Following Economic Signals

Today, stock indexes are showing moderate gains, recovering some of the losses from Wednesday’s selloff. This downturn occurred after the Federal Open Market Committee (FOMC) hinted at lowering interest rates by only 50 basis points (bp) in the coming year, a decrease from the previously projected 100 bp. Recent positive indicators regarding the U.S. economy are encouraging for stocks, as the Q3 GDP was unexpectedly revised upward.

Challenges from a Strong Labor Market

However, a robust U.S. labor market poses challenges for stocks. This strength is considered hawkish for Federal Reserve policy, resulting in rising bond yields. Today, the 10-year Treasury note yield reached a 6-1/2 month high after weekly U.S. jobless claims fell significantly more than anticipated.

Specifically, the Q3 GDP has been revised upward to 3.1% (quarter-over-quarter annualized), exceeding the expected 2.8%.

Moreover, weekly initial unemployment claims decreased by -22,000 to 220,000, indicating a stronger job market than the expected 230,000 claims.

Compounding this, the December Philadelphia Fed business outlook survey unexpectedly dropped -10.9 points to a 20-month low of -16.4, contrasting sharply with predictions of an increase to 2.8.

Looking ahead, key inflation data is set to be released on Friday, focusing on the November core PCE price index—the Federal Reserve’s preferred measure of inflation—which is anticipated to rise to +2.9% year-over-year from +2.8% in October.

Market Expectations for Interest Rate Cuts

The markets currently assess the probability of a -25 bp rate cut at the upcoming January 28-29 FOMC meeting to be about 9%.

Global Market Trends

International stock markets are seeing declines today. The Euro Stoxx 50 has fallen to a two-week low, down -1.14%. China’s Shanghai Composite Index also dropped to a 2-1/2 week low, closing down -0.36%. Additionally, Japan’s Nikkei Stock 225 fell to a 2-1/2 week low, decreasing by -0.69%.

Interest Rates: Recent Developments

March 10-year Treasury notes (ZNH25) are down -8 ticks today, with the 10-year T-note yield rising +3.8 bp to 4.552%. March T-notes hit a 6-1/2 month low today, as the 10-year T-note yield climbed to 4.558%. These movements follow the upward revision of U.S. Q3 GDP and a notable drop in jobless claims, reflecting economic resilience that leans toward a hawkish Fed stance.

In Europe, government bond yields are also on the rise. The 10-year German bund yield has climbed to a 3-1/2 week high of 2.315%, while the 10-year UK gilt yield increased to a 13-3/4 month high of 4.651%.

In more economic updates, Eurozone new car registrations fell -1.9% to 869,816 units. Meanwhile, Germany’s January GfK consumer confidence index rose +1.8 to -21.3, better than expected.

Central Bank Decisions and Expectations

The Bank of England (BOE) has maintained its benchmark rate at 4.75%. Governor Andrew Bailey emphasized the need for a “gradual approach” to future cuts, indicating uncertainty about the timeline and extent of any reductions through 2025.

Swaps are currently indicating a 100% chance of a -25 bp rate cut by the European Central Bank (ECB) at its January 30 policy meeting, alongside a 12% chance for a -50 bp cut.

U.S. Stock Movers to Watch

Leading gainers in the S&P 500, Darden Restaurants (DRI) surged more than +12% after reporting Q2 sales of $2.89 billion, exceeding the consensus forecast of $2.86 billion. The company also raised its 2025 sales estimate to $12.1 billion, surpassing the previous range of $11.8 billion-$11.9 billion and the projected consensus of $11.94 billion.

Accenture Plc (ACN) rose more than +7% following a Q1 revenue report of $17.69 billion, which was better than the $17.15 billion consensus. CarMax (KMX) garnered more than +5% after reporting Q3 net sales of $6.22 billion, exceeding expectations of $6.04 billion.

Palantir Technologies (PLTR) gained over +4% after extending its contract with the U.S. Army for the Vantage data analytics program, valued up to $618.9 million. In the Dow Jones Industrials, American Express (AXP) led with a +2% increase after Morgan Stanley raised its price target from $252 to $305. Hewlett Packard Enterprise (HPE) also see gains of +2% after being upgraded to buy from hold by Deutsche Bank with a $25 price target.

Additionally, SentinelOne (S) climbed over +3% following a buy rating upgrade from Jeffries, which set a price target of $30, while Fortinet (FTNT) rose more than +2% after being upgraded by KeyBanc Capital Markets.

Stocks Under Pressure

On the downside, Lamb Weston Holdings (LW) fell -17% after posting a Q2 adjusted EPS of 66 cents, significantly below the consensus of $1.02. The firm also reduced its 2025 adjusted EPS forecast to $3.05-$3.20 from a prior estimate of $4.15-$4.35, weaker than the consensus of $4.23.

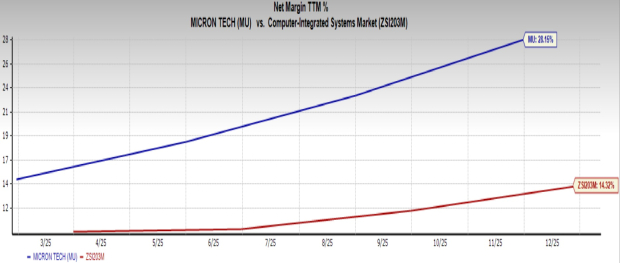

Micron Technology (MU) dropped over -16% after forecasting a Q2 adjusted revenue between $7.7 billion and $8.1 billion, falling short of the consensus estimate of $8.99 billion. Homebuilders are facing challenges, with Lennar (LEN) down -4% following its report of Q4 new orders that missed expectations. Other major builders like DR Horton (DHI) and PulteGroup (PHM) also registered losses.

Vertex Pharmaceuticals (VRTX) saw a decline of more than -12% after its mid-stage pain trial revealed results similar to its placebo, while Western Digital (WDC) fell over -3% following a downgrade from Benchmark Company LLC.

Conagra Brands (CAG) is down more than -3% after lowering its yearly adjusted EPS forecast to $2.45-$2.50 from $2.60-$2.65, below the consensus of $2.58. Lastly, Worthington Steel (WS) is off more than -15% after announcing Q2 revenue of $739 million, representing a -9% decline from the same quarter last year.

Earnings Reports (12/19/2024)

Look out for earnings reports from Accenture PLC (ACN), CarMax Inc (KMX), Cintas Corp (CTAS), Conagra Brands Inc (CAG), Darden Restaurants Inc (DRI), FactSet Research Systems Inc (FDS), FedEx Corp (FDX), Lamb Weston Holdings Inc (LW), NIKE Inc (NKE), and Paychex Inc (PAYX).

On the date of publication, Rich Asplund did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.