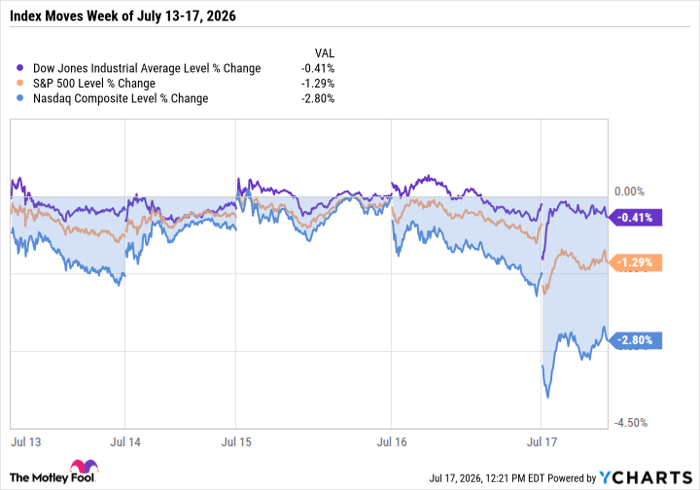

On July 17, 2026, major U.S. stock indexes experienced significant declines, with the S&P 500 down 0.87%, the Dow Jones Industrial Average falling 0.12%, and the Nasdaq 100 dropping 1.76%. The S&P 500 hit a one-week low, the Dow registered a 2.5-week low, and the Nasdaq fell to a five-week low. The downturn was exacerbated by a global selloff in chipmakers due to concerns surrounding artificial intelligence valuations, alongside a 3% drop in China’s Shanghai Composite and a 4% decline in Japan’s Nikkei-225. Additionally, WTI crude oil rose over 3% as geopolitical tensions escalated following U.S. military actions against Iran.

In economic data, the University of Michigan’s July consumer sentiment index increased to 54.4, a five-month high, exceeding expectations of 51.0. U.S. June housing starts rose by 19% month-over-month to 1.427 million, surpassing forecasts of 1.310 million, though building permits fell 3% to 1.367 million, below the expected 1.403 million. In contrast, U.S. manufacturing production was unchanged in June, underperforming predictions of a 0.1% increase.

Corporate insider selling reached $77.6 billion in the first half of the year, marking one of the highest figures in two decades. As markets anticipated a 10% chance of a 25 basis point rate hike at the upcoming FOMC meeting, major tech companies, including Meta and Alphabet, experienced losses. Cybersecurity stocks showed resilience, with significant gains in companies like Palo Alto Networks and Zscaler.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.