Newmark Group Faces Challenges but Shows Potential for Growth

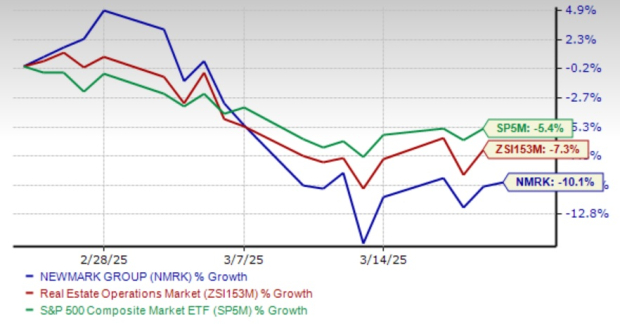

Newmark Group, Inc. (NMRK) has seen its stock decrease by 10.1% over the past month, closing at $12.58 on Thursday. This decline is underperforming both the Zacks Real Estate – Operations industry and the S&P 500 composite.

Recent macroeconomic uncertainty, issues related to tariffs, and expectations of sustained high interest rates have impacted the overall market. The commercial real estate sector has not been exempt from these challenges, leading to delayed transactions as investors adopt a more cautious approach.

Such circumstances have affected NMRK, contributing to its current underperformance. Nonetheless, the company’s results in recent years demonstrate its strategic strengths. It is crucial for investors to carefully assess NMRK’s growth potential and determine whether current market concerns will have a significant impact on its future performance.

One-Month NMRK Stock Price Performance

Image Source: Zacks Investment Research

Key Drivers for Growth in Newmark’s Stock

Capital Markets Performance and Market Share Growth: Newmark is experiencing robust capital markets performance and has gained market share. In the fourth quarter of 2024, it reported a 20.0% increase in capital markets revenues, extending a streak of five consecutive quarters with double-digit growth. Excluding the impactful fourth-quarter 2023 Signature transactions, Newmark outperformed the industry with a remarkable 113% rise in total capital markets notional volumes last quarter. Key contributors included a 209% increase in Mortgage Brokerage and Debt Placement, an 85% boost in GSE/FHA origination, and a 71% rise in Investment Sales. Notably, the company achieved a record $9.2 billion in industrial volumes due to demand growth from hyperscale AI users in data centers.

From 2015 to 2024, Newmark’s share of U.S. investment sales climbed from 3.3% to 8.7%. Additionally, its share of total U.S. debt market volume grew from 1.5% to 8.9%. With $2.1 trillion in commercial and multifamily mortgage maturities expected by 2027—25% of which could be troubled, per Newmark Research—the company appears poised to benefit from increased transaction activity. This anticipated volume also positions Newmark to enhance its other services, including leasing, property management, and valuation & advisory.

Growth in Management and Servicing Revenues: Newmark’s management services and servicing sector provide a steady revenue foundation. The company aims to elevate its total revenues from these services to over $2 billion within the next five years. Between 2017 and 2024, fees from these operations surged by 219%, and total revenues increased by 190%, marking them as Newmark’s fastest-growing service lines since its IPO.

Strong Financial Position and Cash Flow: Newmark boasts a robust financial position, enabling it to invest in growth while maintaining stability. Its capital-light business model, which does not involve property ownership, and low leverage (a net leverage ratio of 1.1 as of December 31, 2024), paired with a solid interest coverage ratio of 7.9, supports its cash flow generation. The company generated $437.6 million in operating cash flow in 2024.

With no near-term debt maturities and leverage significantly below its long-term target of ≤1.5X, Newmark is Strategically positioned to withstand any potential market disruptions.

International Expansion for Long-Term Growth: Newmark has recently expanded into Europe, launching capital markets and leasing operations in Germany during the fourth quarter of 2024 and adding skilled personnel in France, the U.K., and other regions. This strategic move allows it to seize growth opportunities.

Its non-U.S. revenues climbed from 0.9% of total revenues in 2017 to 13.3% in 2024, demonstrating a compound annual growth rate of approximately 59%. With international revenue only accounting for 13.3% of its total, compared to 28-46% for its full-service U.S. peers, Newmark has significant potential for further growth.

Analysts Favor Newmark with Revised Estimates

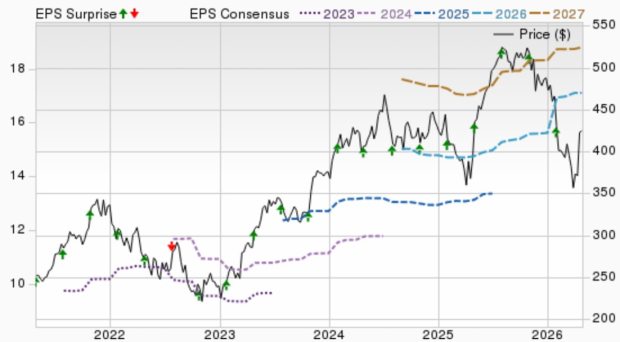

Analysts appear optimistic about Newmark Group’s future, as reflected in the upward revisions of the Zacks Consensus Estimate for EPS for both 2025 and 2026 over the past two months. These estimates suggest growth rates of 17.9% and 14.8% for 2025 and 2026, respectively.

Image Source: Zacks Investment Research

Explore the latest EPS estimates and surprises on Zacks Earnings Calendar.

From a valuation standpoint, Newmark Group shares offer an attractive investment opportunity. Currently trading at a forward price-to-earnings ratio of 8.40X, NMRK is undervalued relative to the industry average of 15.47X and below its one-year median of 9.62X. This stock is also trading at a discount compared to its peers, such as CBRE Group, Inc. with a P/E of 20.75X and Jones Lang LaSalle Incorporated with a P/E of 14.61X.

Forward 12-Month Price-to-Earnings (P/E) Ratio

Image Source: Zacks Investment Research

Conclusion on Newmark’s Future

Newmark Group has shown considerable operational momentum through market share expansion, strategic financial investments, and a resilient business strategy. While the company faces macroeconomic uncertainties, its robust capital markets platform, servicing business, and strong cash flow indicate it is well-prepared for future growth.

Analysts’ positive outlook on Newmark reinforces the potential for recovery and growth in its stock’s value.

Why Investing in This Zacks #1 Stock Makes Financial Sense

Recent upward estimate revisions and a favorable valuation suggest that taking a position in this Zacks Rank #1 (Strong Buy) stock is a wise move. Investors may want to act quickly, as the price may shift significantly from its current level. For further insights, you can access the complete list of today’s Zacks #1 Rank stocks here.

Access Zacks’ Stock Recommendations for Just $1

We’re serious about this offer.

In a bold move several years ago, we provided our members with 30 days of access to all our stock picks for just $1, with no further financial obligation. Thousands of individuals took advantage of this unique opportunity, but some hesitated, suspecting a hidden catch.

Our goal is to introduce you to our portfolio services that include Surprise Trader, Stocks Under $10, Technology Innovators, and others. In 2024 alone, these offerings closed 256 positions with impressive double- and triple-digit gains.

Check out these companies for more detailed insights:

- Newmark Group, Inc. (NMRK): Free Stock Analysis Report

- Jones Lang LaSalle Incorporated (JLL): Free Stock Analysis Report

- CBRE Group, Inc. (CBRE): Free Stock Analysis Report

This article was originally published on Zacks Investment Research, which you can access here.

The views and opinions expressed herein are the author’s own and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.