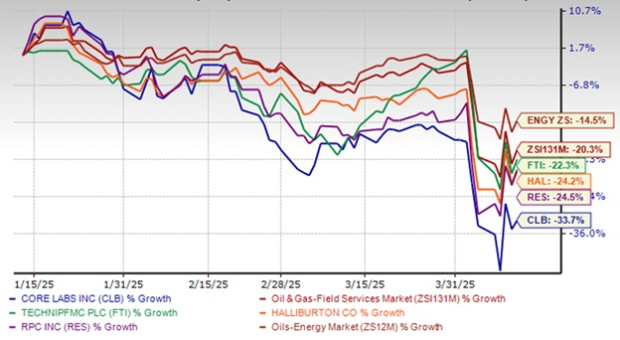

Core Laboratories Shares Drop 33.7% Amid Financial Challenges

Core Laboratories Inc. (CLB), a leading oilfield services provider operating in over 50 countries, has seen its share price plummet by 33.7% over the past three months. This decline has outpaced the wider oil and energy sector, which saw a 14.5% drop, as well as the Field Services sub-industry decline of 20.3%. Moreover, Core Laboratories has lagged behind its key competitors. Shares of TechnipFMC (FTI), Halliburton (HAL), and RPC, Inc. (RES) have declined by 22.3%, 24.2%, and 24.5%, respectively.

Overview of Stock Performance in the Last Quarter

Image Source: Zacks Investment Research

Upcoming Q1 Earnings Report

Core Laboratories is expected to announce its first-quarter earnings on April 23, after the market closes. The Zacks Consensus Estimate anticipates earnings of 15 cents per share and revenues of $124.06 million for the quarter. This anticipated earnings figure represents a sharp 34.8% year-over-year decline, while the revenue estimate suggests a decrease of 4.30% compared to the same quarter last year.

Keep track of the latest EPS estimates and surprises with Zacks here.

This substantial decline in share price raises a critical question for investors: Should they consider this a buying opportunity or a sign to steer clear of the stock?

Factors Driving the Decline in CLB’s Share Price

Disappointing Q4 Revenues: Core Laboratories’ fourth-quarter 2024 revenues totaled $129.2 million, marking a 4% sequential decrease from the third quarter of 2024. This figure fell short of the Zacks Consensus Estimate of $131 million by 1.4%, primarily due to reduced U.S. land drilling and completion activities, alongside disruptions from geopolitical sanctions affecting crude oil assay services.

Weak Performance in Production Enhancement Segment: The Production Enhancement segment of Core Laboratories recorded a 3% year-over-year revenue decline, along with a 7% sequential drop in Q4 2024, reflecting weakened U.S. onshore drilling activity. Pricing pressures and lower demand for well completion products continue to plague this segment.

Lower Guidance for Q1 2025: For the first quarter of 2025, Core Laboratories anticipates a reduction in operating margins to approximately 9%, down from 12% recorded in Q4 2024. This forecast indicates reduced earnings due to seasonal slowdowns, subdued U.S. onshore activity, and potential geopolitical risks that could further dampen investor confidence.

Minimal Dividend Yield: Although Core Laboratories generated solid free cash flow, its quarterly dividend remains at just 1 cent per share, offering a low yield compared to its competitors TechnipFMC, Halliburton, and RPC. The management’s focus on debt reduction and share repurchases may deter income-focused investors.

Geopolitical Risks Impacting Revenues: The escalation of U.S. sanctions in early 2025 has significantly affected crude assay laboratory services and product sales, particularly in essential international markets. Such disruptions could continue to hinder Reservoir Description revenues if sanctions persist.

Slow U.S. Oil & Gas Production Growth: The U.S. Energy Information Administration has predicted only a modest increase in U.S. oil production from 13.2 million barrels per day in 2024 to 13.5 million barrels per day in 2025. With drilling activity remaining flat to slightly declining, CLB’s Production Enhancement sector might struggle to regain lost revenues.

Challenges in Inventory and Supply Chain: Though inventory efficiency has improved, a 9% sequential decline in inventory levels in Q4 2024 reveals potential supply chain issues. Should demand unexpectedly surge, the company may have difficulty fulfilling orders, potentially affecting revenues and overall customer satisfaction.

Increased CapEx Could Affect Free Cash Flow: While free cash flow was robust in 2024, rising capital expenditures planned for 2025, such as rebuilding the Aberdeen facility post-fire, may temporarily diminish cash available for shareholder returns and debt repayment.

Valuation Concerns: Core Laboratories’ EV/EBITDA ratio stands at 8.26, notably higher than the Oil and Gas Field Services industry average of 5.62. This suggests potential overvaluation against competitors like TechnipFMC, Halliburton, and RPC. Should CLB’s earnings fail to meet future expectations, the stock could face a significant correction.

Image Source: Zacks Investment Research

Conclusion: Caution Advised for CLB Stock

This Zacks Rank #4 (Sell) company is grappling with various internal and external challenges. Revenue declines, shrinking margins, lackluster demand in critical segments, and geopolitical uncertainties are weighing heavily on its performance. Concerns regarding the company’s elevated valuation relative to industry peers further question the sustainability of its current stock prices. With a slight dividend return and rising capital expenditures, the near-term outlook for Core Laboratories remains uncertain. Until the company can demonstrate improved financial performance and operational stability, it is wise for investors to explore alternatives in the oil and gas sector.

You can access the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

These stocks have been selected by a Zacks expert as the #1 favorites expected to gain +100% or more in 2024. While not every pick may succeed, previous recommendations have seen gains of +143.0%, +175.9%, +498.3%, and +673.0%.

Most of these stocks are under the radar of Wall Street, presenting a great opportunity to invest early.

Discover These 5 Potential Home Runs >>

For the latest investment recommendations from Zacks Investment Research, download 7 Best Stocks for the Next 30 Days for free.

Halliburton Company (HAL): Free Stock Analysis Report

Core Laboratories Inc. (CLB): Free Stock Analysis Report

TechnipFMC plc (FTI): Free Stock Analysis Report

RPC, Inc. (RES): Free Stock Analysis Report

Originally published on Zacks Investment Research (zacks.com).

The views expressed here are those of the author and do not necessarily reflect the opinions of Nasdaq, Inc.