Hims & Hers Sees Mixed Short-Term Gains Amid Growth Strategy

Hims & Hers Health, Inc. (HIMS) investors have recently observed short-term gains, though these are significantly lower than returns noted until mid-February. Based in San Francisco, the health and wellness platform’s stock performance has been turbulent since then. HIMS managed a 5.8% increase, outperforming the industry, which saw a 2.1% decline during the same period. Comparatively, the S&P 500 and broader sector experienced declines of 10.4% and 5.2%, respectively.

Recent Developments in Business Strategy

In February, two noteworthy developments occurred: the announcement of its promising fourth-quarter 2024 results and the acquisition of a peptide facility located in California. This buyout aims to enhance HIMS’ domestic supply chain, addressing the rising demand for personalized healthcare solutions among Americans.

During the earnings call, management confirmed the closure of a deal for an at-home whole-body lab testing provider. This capability will allow HIMS to test a variety of critical biomarkers related to heart, hormone, liver, thyroid, and prostate health, facilitating the proactive identification of disease risks.

Earnings Performance and Future Expectations

Despite these positive initiatives, HIMS reported earnings per share that fell short of the Zacks Consensus Estimate by a penny in the latest quarter. Additionally, the gross margin contracted, reflecting higher product costs, which is a concern for investors.

Looking ahead, Hims & Hers is slated to announce its first-quarter 2025 results on May 5, 2025, after market close.

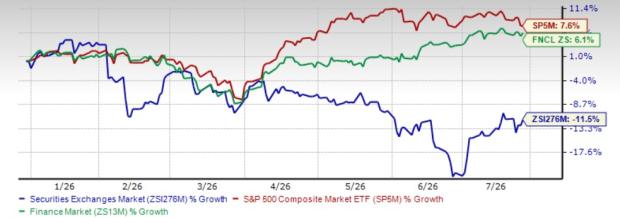

HIMS Three Months Price Comparison

Image Source: Zacks Investment Research

Over the past three months, HIMS has shown strong stock performance compared to peers such as Teladoc Health, Inc. (TDOC). In this timeframe, Teladoc shares fell by 22.1%, while Abbott Laboratories (ABT) shares rose by 10.8%. HIMS’ performance highlighted its competitive edge within the market, despite some challenges.

Even with several hurdles facing the health and wellness industry, including workforce-related challenges and health threats, positive forecasts suggest HIMS may sustain its market momentum.

For the first quarter of 2025, HIMS anticipates revenues between $520 million and $540 million, reflecting an uptick of 87-94% year over year. For the full year, the expected revenue range is $2.3 billion to $2.4 billion, which indicates a growth rate of 56-63% compared to 2024 levels. The Zacks Consensus Estimate for quarterly revenues stands at $537.9 million, while the full year estimate is $2.33 billion. Current estimates for earnings per share are 14 cents and 72 cents for the quarter and the full year, respectively.

HIMS’ Strong Fundamentals

Hims & Hers is receiving positive market acceptance for its curated range of health and wellness products. The company focuses on providing affordable, quality, personalized solutions, which significantly boosts its net subscriber numbers.

Hims & Hers believes that the growing demand for personalized options, along with the maturation of various customer demographics benefiting from favorable pricing, is enhancing retention rates. The firm is successfully acquiring customers via cost-effective channels as awareness of its brand expands.

In the fourth-quarter earnings call last month, management noted that average monthly revenue per subscriber grew by 38% year over year, primarily driven by the scaling of GLP-1 offerings and a shift towards premium personalized products. Management also highlighted that significant investments made in the previous quarter may lead to future economies of scale.

Expanding Product Offerings

Hims & Hers continues to enhance its weight loss product offerings. In November 2024, the company announced doorstep delivery for meal replacement bars and shakes, helping customers achieve their health goals.

Furthermore, in September, HIMS introduced access to commonly compounded GLP-1 subscriptions for $99 monthly, targeting eligible U.S. military personnel, veterans, teachers, nurses, and first responders. Such efforts to facilitate product access could broaden its customer base, promising positive growth.

Potential Challenges Moving Forward

Hims & Hers has faced challenges, particularly due to a widespread shortage of semaglutide, a prescription medication. This shortage accelerated the compounding of semaglutide in the U.S., allowing patients to access weight loss drugs during branded product shortages. However, the FDA announced in February that the semaglutide injection product shortage has been resolved, ending a nearly three-year scarcity. As compounding drugs are federally restricted, this may present challenges for Hims & Hers, which benefited from the prior shortage.

During the fourth quarter of 2024, Hims & Hers experienced a gross margin contraction of 594 basis points due to climbing revenue costs, highlighting the importance of cost control for the company moving forward.

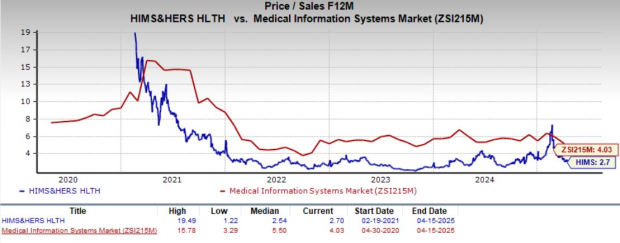

Stock Valuation Insights

HIMS’ forward 12-month price-to-sales (P/S) ratio is currently 2.7X, which is below the industry average of 4X but above its five-year median of 2.5X.

Image Source: Zacks Investment Research

In comparison, Teladoc and Abbott currently have forward 12-month P/S ratios of 0.5X and 4.8X, respectively.

Hims & Hers’ Estimate Movement

Over the past two months, estimates for Hims & Hers’ 2025 earnings have risen by 38.5% to 72 cents per share.

Hims & Hers Emerges as Strong Investment Choice Amid Growth Potential

Hims & Hers is well-positioned, displaying core business strength, substantial earnings potential, a solid financial foundation, and numerous global opportunities. The company, holding a Zacks Rank #2 (Buy), boasts impressive growth prospects, making it an attractive pick for investors right now. For a comprehensive overview of today’s top Zacks #1 Rank (Strong Buy) stocks, click here.

Valuation Insights and Industry Comparison

Investors looking to enhance their portfolios will find that Hims & Hers offers superior performance expectations compared to its industry peers. Currently, the company’s valuation is lower than the industry average, indicating potential for growth if it aligns more closely with market performance trends. Additionally, Hims & Hers carries a favorable Zacks Style Score with a Growth Score of A, implying a likely upward trajectory in its stock price.

Zacks Highlights Promising Semiconductor Stock

One noteworthy investment opportunity emerging in the semiconductor sector is a stock that is significantly smaller than NVIDIA, which has experienced a remarkable rise of over +800% since its recommendation. Although NVIDIA remains strong, this new top chip stock has substantial room for growth.

The semiconductor market is increasingly vital, driven by strong earnings growth and an expanding customer base that caters to rising demands in Artificial Intelligence, Machine Learning, and the Internet of Things. Projections indicate that global semiconductor manufacturing could surge from $452 billion in 2021 to $803 billion by 2028.

Discover This Stock Now for Free >>

Abbott Laboratories (ABT) : Free Stock Analysis Report

Teladoc Health, Inc. (TDOC): Free Stock Analysis Report

Hims & Hers Health, Inc. (HIMS) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are solely those of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.