Suncor Energy Readies to Release Earnings: What to Expect

Suncor Energy SU will announce its fourth-quarter earnings on February 5, after the market closes. The Zacks Consensus Estimate for earnings sits at 82 cents per share, while revenues are expected to reach $8.56 billion.

Check out the latest EPS estimates and surprises on Zacks Earnings Calendar.

Before we dive deeper into Suncor’s anticipated performance, it’s useful to review the company’s results from the previous quarter.

Review of Suncor’s Q3 Results and Earnings Trend

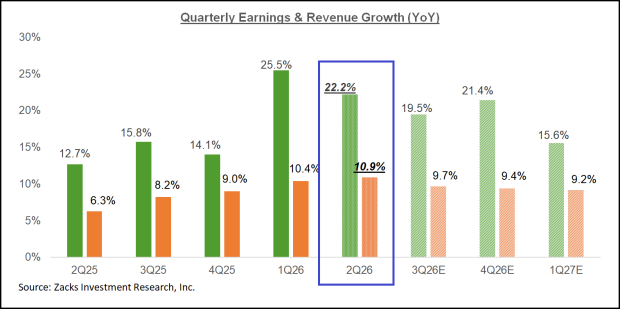

In the last reported quarter, Suncor Energy, an integrated oil and gas company based in Alberta, exceeded earnings expectations. The firm reported an earnings per share (EPS) of $1.08, surpassing the Zacks Consensus Estimate by 20 cents. This strong performance was driven by increased oil sands production, robust refining results, and effective cost management. Suncor’s operating revenues reached $9.6 billion, beating the consensus estimate by 11.7%. Impressively, Suncor has consistently beaten earnings estimates over the past four quarters, achieving an average earnings surprise of 19.87%. This is depicted in the graph below:

Suncor Energy Inc. Price and EPS Surprise

Suncor Energy Inc. price-eps-surprise | Suncor Energy Inc. Quote

Trends in Earnings Estimates

The earnings consensus for the fourth-quarter of 2024, currently at 82 cents per share, has increased by 7.8% over the past month. However, this figure marks a decline of 17.54% compared to the same quarter last year. Additionally, revenue estimates show a decrease of 11.83% year-over-year.

Key Considerations for Suncor’s Q4 Earnings

Suncor Energy profits from three primary segments: Oil Sands, Exploration and Production, and Refining and Marketing. The Oil Sands division extracts and processes oil from Canada’s oil sands, while the Exploration and Production segment focuses on offshore oil and gas fields. In Refining and Marketing, Suncor converts crude oil into gasoline, diesel, and other products, which are distributed through retail channels.

Positive indicators suggest that Suncor may report record quarterly production of 874,000 barrels per day (bbls/d), reflecting an increase from previous quarters. Additionally, refinery throughput could also reach new highs at 487,000 bbls/d as all refineries operated above 100% capacity. These results highlight the company’s operational efficiency and strong asset performance, enhancing its competitive edge in the energy market. Notably, Suncor has met its $8 billion net debt target nine months ahead of schedule, showcasing prudent capital management and a robust balance sheet.

On the flip side, challenges in profitability may arise due to market factors. Weaker oil prices or margins in refining could offset revenue growth, impacting earnings. Moreover, fluctuations in refining crack spreads and demand for fuel may exert pressure on downstream margins, limiting the benefits of high throughput levels. Inflationary pressures could also escalate operational costs, as rising expenses for inputs and labor impact profitability.

Insights from the Earnings Model

The Zacks model indicates uncertainty regarding an earnings beat for Suncor this quarter. Typically, a positive Earnings ESP combined with a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) signals a higher likelihood of surpassing earnings estimates—but this does not apply here.

Earnings ESP of SU: The Earnings ESP, which reflects the difference between the Most Accurate Estimate and the Zacks Consensus Estimate, currently stands at 0.00%. To find top stocks to buy or sell ahead of their reports, utilize our Earnings ESP Filter.

SU’s Zacks Rank: Suncor currently holds a Zacks Rank of #3.

Alternative Stocks for Consideration

While Suncor’s prospects appear uncertain, several other companies in the energy sector may warrant attention:

California Resources CRC features an Earnings ESP of +2.59% and a Zacks Rank of #1. The company is set to report its earnings on March 3, with a Zacks Consensus Estimate indicating 8.03% year-over-year growth for its 2025 EPS. Currently valued at approximately $4.67 billion, CRC’s shares have dipped 0.1% over the past year.

EQT EQT has a favorable Earnings ESP of +4.50% and holds a Zacks Rank of #3. Its earnings release is anticipated on February 18, with a 146.51% year-over-year earnings growth projected for 2025. Valued at around $29.77 billion, EQT’s stock has appreciated by 42% in the past year.

Energy Transfer ET exhibits an Earnings ESP of +4.23% and is ranked #3. Its earnings report is expected on February 11, with a 6.08% year-over-year growth forecast for 2025 EPS. Currently valued at about $69.68 billion, ET’s shares have increased by 41.3% over the past year.

Five Stocks Poised for Doubling Potential

These stocks have been selected by Zacks experts for their potential to gain +100% or more in 2024. While not every recommendation may be successful, past suggestions have seen impressive returns of +143.0%, +175.9%, +498.3%, and +673.0%.

Many of these stocks remain under the radar of Wall Street, presenting an opportunity for early investment.

Analyzing the Potential of Energy Stocks: Key Reports You Shouldn’t Miss

Discover Top Stock Picks for the Coming Weeks

Today, See These 5 Potential Home Runs >>

Get Insightful Free Stock Analysis Reports

EQT Corporation (EQT): Free Stock Analysis Report

Suncor Energy Inc. (SU): Free Stock Analysis Report

Energy Transfer LP (ET): Free Stock Analysis Report

California Resources Corporation (CRC): Free Stock Analysis Report

For an in-depth analysis of Suncor Energy’s upcoming earnings, click here.

The views expressed here are those of the author and do not necessarily represent the opinion of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.