Unexpected Fiscal Q2 2024 Guidance

Super Micro Computer (NASDAQ:SMCI) has delivered a new fiscal Q2 2024 guidance that has taken investors by surprise. The company is anticipating remarkable growth with revenues expected to soar by more than 100% y/y to approximately $3.7 billion.

With a net cash position of approximately $400 million, this hyper-growth business is priced at 14x non-GAAP EPS, offering investors a compelling risk-reward despite some notable risk factors.

Historical Perspective

Back in September, a bullish analysis emphasized Super Micro Computer’s potential due to its specialization in high-performance and energy-efficient computer systems for AI markets. Despite challenges like potential commoditization and pricing competition, the company’s strong cash flow and innovation capabilities were noted as promising.

Since then, the share price has moved slightly higher, but the delivery of such a strong return has exceeded investor expectations.

The Strength of Super Micro Computer

Super Micro Computer specializes in designing high-performance and energy-efficient computer systems for various markets such as data centers, cloud computing, and AI. The company’s dedication to resource-saving architecture and its success in providing complete rack-scale solutions to major AI innovators position it well in the growing AI market.

Given this background, let’s delve into SMCI’s new guidance.

Astounding Revenue Growth Rates

The company’s fiscal Q2 2024 guidance exceeds expectations, with revenues projected to grow by over 100% y/y. This level of growth was not widely anticipated, particularly given the challenges posed by the previous fiscal quarter. The company’s newly found growth appears to position it for a strong performance in the coming fiscal H2 2024.

With the high end of its guidance pointing to $3.7 billion for fiscal Q2 2024, SMCI seems to be on a path towards $17 billion in revenues in the coming 12 months—a significant surge beyond analysts’ expectations.

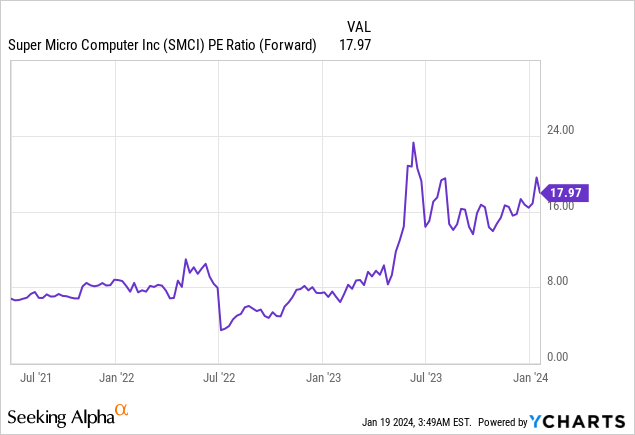

SMCI Stock Valuation—Impressive Forward EPS

At the high end, SMCI is guiding for $5.55 of EPS, indicating a potential run-rate of $25 over the next twelve months. This brings SMCI’s stock price to about 14x forward EPS, a compelling investment considering the estimated growth of +80% over the next 12 months.

Despite the expectation that such growth rates are not sustainable in the long term, the current 14x forward EPS valuation seems favorable given the company’s strong growth prospects.

Consideration of Risk Factors

Unforeseen Triumph: Super Micro Computer Inc.’s Fiscal Q2 2024 Guidance Surpasses Expectations

Super Micro Computer Inc. (SMCI) has remarkably defied expectations by unveiling an impressive fiscal Q2 2024 guidance, much to the awe of investors.

Customer Concentration and Risk Assessment

SMCI has formed critical collaborations with industry giants such as NVIDIA (NVDA), AMD (AMD), and Intel (INTC), leading to amplified customer concentration. Notably, in the fiscal Q1 2023, one customer accounted for 25% of the net sales for that quarter. This customer stronghold poses a significant risk, making SMCI particularly vulnerable when it comes to renegotiating contracts, thereby exposing the company to the whims of its prominent clientele.

Moreover, the sustainability of SMCI’s accelerated growth and the risk associated with continued breakneck expansion are crucial factors to consider. The company’s ability to maintain its extraordinary growth rates over the long term remains uncertain.

The Bright Side

Despite the aforementioned risk factors, SMCI boasts a net cash position of approximately $400 million and anticipates an exceptional over 100% year-over-year revenue surge, aiming to reach around $3.7 billion in fiscal Q2 2024. Coupled with a forward EPS valuation of 14x, the company’s solid financial foundation makes it an appealing investment opportunity. With a projected +80% growth over the next 12 months, SMCI’s unexpected acceleration in revenue trajectory presents an enticing and compelling prospect in the market.