Super Micro Computer, publicly traded as Super Micro Computer (NASDAQ: SMCI), has become a Wall Street behemoth, quintupling its value since the dawn of 2024. This mountainous climb translates to a 400% surge in stock value, transforming a $1,000 investment into a staggering $4,000 bounty.

With a meteoric rise propelling its market capitalization from $15 billion at the onset of the year, the perennial question looms large – Is it time to buy, hold tight, or sell?

Delving into the realm of Supermicro reveals a narrative that could rival the grandeur of epics; let’s evaluate if this apex marks the summit or merely the foothills of a grander journey.

Riding the AI Wave to the Zenith

Supermicro luxuriates in the surging demand for computing infrastructure, fueled by the insatiable hunger for artificial intelligence (AI) processing. While GPUs are the backbone of AI computations, the intricate network of servers necessitates a mosaic beyond mere graphic processors.

Standing tall amidst competitors like IBM and Hewlett Packard, Supermicro’s forte lies in its bespoke solutions. Clients can tailor their computing arsenals based on needs and size, marking Supermicro as the quintessence of customizability in its domain.

The splendid Q2 financial performance for fiscal 2024, concluding on Dec. 31, showcased a remarkable 103% year-over-year revenue surge, escalating to $3.67 billion. Yet, this seems but the nascent ember. Projections for the upcoming quarter waver between $3.7 billion to $4.1 billion in revenue, indicating exponential growth ranging from 188% to 219%. With a visionary outlook for fiscal 2024, an anticipated revenue of $14.5 billion echoes what Supermicro envisions as a tryst with destiny – a $25 billion annual revenue oasis.

A glimpse into this expanse might indicate that Supermicro’s narrative is far from over. Still, could this eminence already be ingrained in the stock’s valuation?

A Pricy Ticket to Stock Valhalla

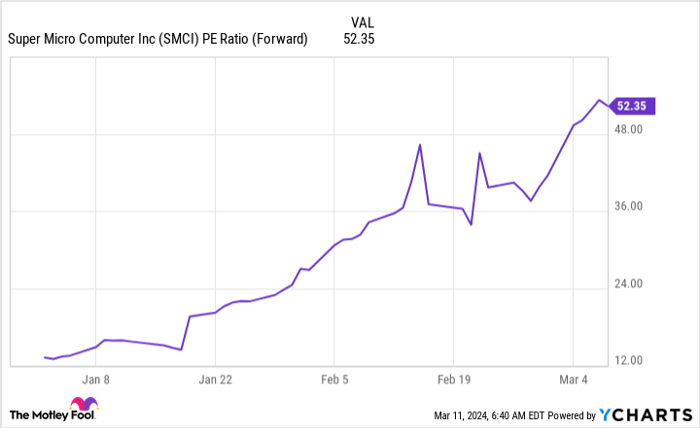

Part of the stock’s meteoric ascension stemmed from its undervalued entry into 2024. Initially traded at 13 times forward earnings, it laid the ground for a spectacular surge. Yet, perched at 52 times forward earnings, Super Micro Computer transcends to a realm beyond, espousing a more opulent valuation than AI overlord, Nvidia, trading at 36 times forward earnings.

SMCI PE Ratio (Forward) data by YCharts

Revisiting historical benchmarks, Supermicro’s decade-long standard rested at around 19 times trailing earnings, spotlighting the chasm it faces to realign. To revert to its historical valuation, a staggering growth trajectory awaits Supermicro.

Pressures mount as Supermicro endeavors to reach the $25 billion revenue summit while maintaining its 8% profit margin. Should this lofty ambition crystallize, an annual profit of $2 billion beckons. With the current market capitalization of $64 billion divided by the hypothetical earnings, a price-to-earnings (P/E) ratio of 32 emerges – a significant premium over traditional valuation thresholds.

While the whims of the stock market may continue to usher Supermicro towards the heavens, the exigencies underlying its current valuation paint a tentative future.

Considering the assumptions tethered to Super Micro Computer’s stock fervor, an air of uncertainty lingers. As a prospective shareholder, the prudent course seems to be selling to secure the gains attained thus far.

Is Super Micro Computer’s stock a worthy investment for you?

Before diving into Super Micro Computer’s stock, contemplate this:

The analyst squadron of Motley Fool Stock Advisor unveiled their chosen elite – the 10 best stocks poised for exponential growth, with Super Micro Computer missing the cut. These 10 chosen equities harbor the potential for monumental returns in the years ahead.

Stock Advisor ushers investors into a terrain laced with success blueprints, offering counsel on crafting portfolios, periodic analyst updates, and two fresh stock picks monthly. Since 2002, the Stock Advisor service has eclipsed S&P 500 returns by triple folds*.

Explore the 10 stocks deemed worthy

*Stock Advisor statistics as of March 11, 2024

Keithen Drury abstains from any holdings in the stocks discussed. The Motley Fool maintains a neutral stance on the discussed equities. The Motley Fool upholds a transparency policy.

The expressions and viewpoints articulated herein are representative solely of the author and do not necessarily resonate with Nasdaq, Inc.