Tesla Faces Criticism from Analyst Over Revenue Growth Assumptions

CEO of GLJ Research LLC and Tesla Inc. TSLA bear Gordon Johnson challenged optimistic projections from investors on Wednesday, questioning the belief that the company is “more than a car company.”

Recent Statements:

In a post on the social media platform X, Johnson remarked, “2025E appears set to disappoint the Wall Street bulls taking up their price targets on the idea ‘$TSLA is not a car company’—i.e., despite the fact that ~88% of its revs came from selling cars in 4Q24.”

Revenue Breakdown:

Although Johnson asserted that 88% of Tesla’s revenue stemmed from automotive sales, the actual figure was lower. In its fourth-quarter report, Tesla disclosed total revenue of $25.71 billion, with automotive revenue reaching $19.8 billion—approximately 77%. The company also generates income from its energy generation, storage, and service sectors.

Market Concerns:

Johnson pointed out, “$TSLA is a company valued for exponential growth that has not grown in its most profitable market—California, which represents 33% of $TSLA’s 2024 US sales of ~691K—for five consecutive quarters.” He added that demand is also plummeting in Europe and Canada.

California Vehicle Registrations:

Referring to a recent report by the California New Car Dealers Association (CNCDA), Johnson noted that Tesla had 203,221 vehicle registrations in California for 2024, a nearly 12% decline from the previous year. In the fourth quarter alone, registrations fell by 7.8%, while the total for 2024 was down 11.6%. Tesla’s market share in the zero-emission vehicle sector decreased to 52.5%, down from 60.1% in 2023.

Political Influence:

Johnson attributed this decline in registrations partly to Elon Musk’s political alignment with Republican President Donald Trump, noting that California tends to lean Democratic.

Analyst Perspectives:

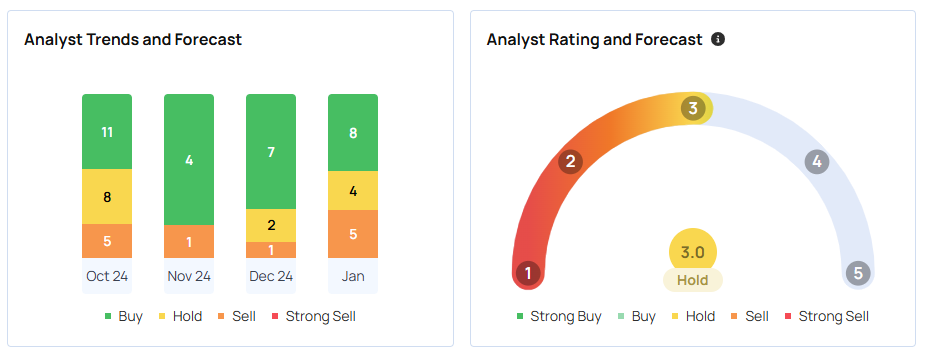

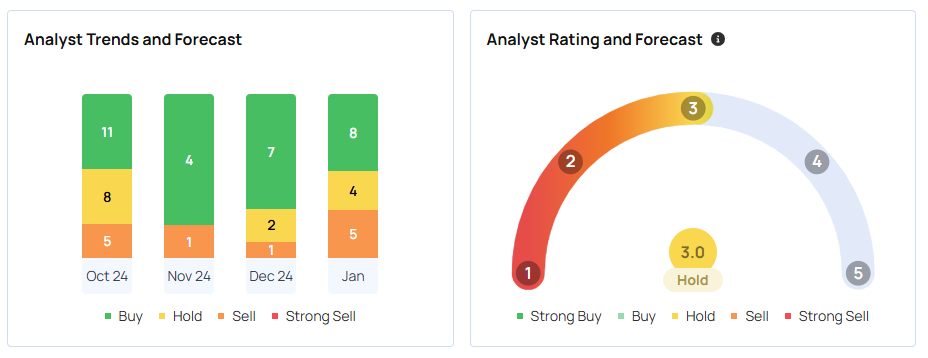

Wedbush Securities analyst Dan Ives often emphasizes that Tesla is an AI and robotics company rather than just a car manufacturer, aligning with Musk’s broader vision. Wedbush maintains a price target of $550 for Tesla and holds an “outperform” rating. In contrast, GLJ Research has a “sell” rating with a price target of $24.86. The overall consensus price target for Tesla stands at $320.75, based on assessments from 32 analysts tracked by Benzinga.

Delivery Trends:

In a notable shift, Tesla experienced its first decline in vehicle deliveries in over a decade. The company reported global deliveries of 1.79 million vehicles in 2024, down from 1.81 million in 2023. Consequently, revenue from the automotive sector decreased 6% to $77.07 billion, while revenue from energy generation and storage saw a significant increase, rising 67% to $10.09 billion, which helped stabilize overall revenue.

Stock Performance:

Tesla’s shares closed up 2.22% at $392.21 on Tuesday and have risen nearly 117% over the past year, according to Benzinga Pro data.

For more insight into the future of mobility, explore additional coverage from Benzinga.

Read Next:

Photo courtesy: Tesla

Market News and Data brought to you by Benzinga APIs