Tesla Shares Rise Despite Troubling Sales and Market Outlook

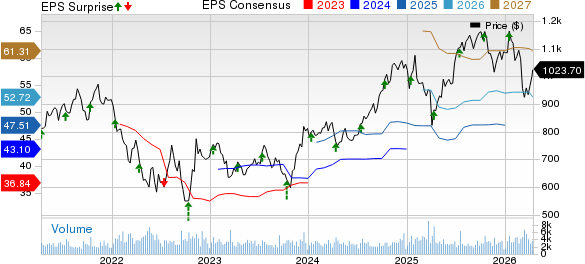

Shares of Tesla (NASDAQ: TSLA) experienced a rebound even after the electric vehicle (EV) manufacturer withdrew its guidance for the year. Currently, the stock is down over 35% in 2025, yet it has risen about 80% over the past year, despite a series of disappointing quarterly earnings reports.

This uptick can largely be linked to CEO Elon Musk’s commitment to concentrate more on Tesla’s operations rather than his role in the Department of Government Efficiency (DOGE). Furthermore, Musk continues to promote Tesla’s ambitions in robotaxis and artificial intelligence (AI).

Struggles in Core Auto Business

Musk’s prior engagements have negatively impacted Tesla’s brand image, distancing potential EV buyers. While it’s positive that he intends to refocus on Tesla, the fallout appears significant.

First-quarter data revealed drops in both auto deliveries and revenue. Deliveries fell 13% to 336,681, and auto revenue decreased 20% to $14 billion. Notably, Model 3 and Model Y deliveries also declined by 13%, and other models saw a 24% drop, indicating challenges with selling the Cybertruck.

This decline does not seem to be a temporary issue. Management retracted its full-year guidance, citing difficulties in assessing the impacts of shifting global trade policies on the automotive and energy supply chain. CFO Vaibhav Taneja acknowledged ongoing brand-image challenges during the earnings call.

Despite Musk’s assertion that the company’s issues stem from macroeconomic factors, real data suggests otherwise. For instance, while Tesla noticed a nearly 9% decline in U.S. deliveries, overall U.S. EV deliveries rose by more than 10%. Additionally, global EV sales increased by 29% in the first quarter, with Europe and China experiencing gains of 22% and 36%, respectively. This indicates Tesla is losing market share in a strong EV market.

Image source: Getty Images

Questionable Future Promises

He announced plans to begin offering paid robotaxi rides in Austin, Texas, starting in June with a fleet of 10 to 20 vehicles, with intentions to expand rapidly into other cities by year-end. Musk expressed confidence that the robotaxi segment would significantly impact revenues by mid-2026.

However, questions remain regarding the feasibility of this timeline. Currently, Tesla operates at Level 2 automation, which requires a driver to remain engaged at all times. Achieving Level 4 automation, necessary for fully autonomous vehicles, is a significant leap that would bypass Level 3, where vehicles can manage most tasks but still require human intervention under certain conditions.

Details on achieving Level 4 automation were scant, and Tesla’s choice to forgo lidar technology in favor of a vision-only approach has left it trailing behind competitors. Past promises in autonomous driving have often met skepticism, raising doubts as to whether the June timeline is realistic.

Even if Tesla successfully launches a robotaxi service, it may not resolve the company’s overarching issues. Alphabet’s Waymo currently leads the robotaxi market in the U.S., and Tesla’s brand reputation problems could affect its robotaxi operations as well. Moreover, many robotaxi services would likely cater to urban areas, which typically lean more liberal.

Rohan Patel, former head of business development and policy at Tesla, noted in an interview that internal analyses suggest slow payback for its robotaxi ambitions.

High Stock Valuation Concerns

Tesla’s stock has consistently enjoyed a premium valuation tied to the optimistic narratives Musk presents, which now diverges significantly from economic realities.

Currently, the company faces declining market share and revenue. It trades at a forward price-to-earnings ratio (P/E) exceeding 100 based on 2025 estimates, while profitable U.S. automotive peers have multiples below 10. In contrast, despite interest in the robotaxi prospect, Alphabet’s established robotaxi business does not command a similar valuation premium.

Considering Tesla’s valuation and the observed brand damage, there is reason to believe the stock could continue to fall.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.