The week of January 29 is looming large, emerging as one of the most pivotal periods in the financial calendar. The culmination of earnings, fiscal, and monetary policy events sets the stage for what looms on the horizon during the ensuing months.

Market Moving Events

This week, investors are bracing for a deluge of activity, with earnings releases from 5 of the Magnificent 7, an FOMC meeting, an array of economic data, and the quarterly refunding announcement from the US Treasury. The last time a similar confluence of cataclysmic information hit markets was during the week of October 27, which set off a stock market frenzy into year-end as rates plummeted and financial conditions relaxed.

The Borrowing Estimates

On January 29, all eyes are on the US Treasury’s announcement of its Marketable Borrowing Estimates. This is a pivotal moment wherein the Treasury communicates its intentions on borrowing for the January to March 2024 quarter. An estimate from the last announcement on October 29 revealed the Treasury anticipated the need to borrow $816 billion in privately-held net marketable debt for this quarter.

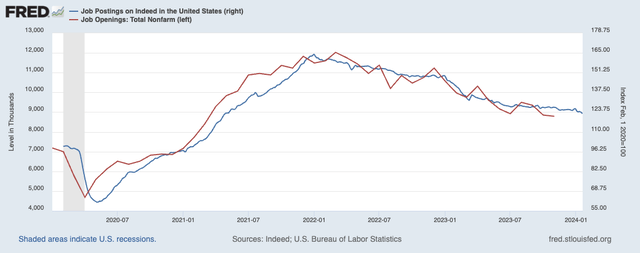

Job Openings and Earnings

January 30 brings a flurry of job opening data, with analysts predicting job openings to total 8.709 million in December. The day also culminates with earnings results from Advanced Micro Devices (AMD), Microsoft (MSFT), and Alphabet (GOOGL) (GOOG).

Treasury’s Quarterly Refunding Announcement

January 31 is marked by the Quarterly Refunding Announcement by the Treasury, preceding the start of the trading session. This announcement holds paramount importance, as it lays down the Treasury’s roadmap for issuing debt. The allocation of debt – whether it will be more front-loaded towards bills or back-end weighted towards duration, will undoubtedly influence long-end rates and financial conditions.

Looking back at November 1, the issuance weighted towards the billing side precipitated a significant drop in long-end rates, easing financial conditions, and catalyzing a risk-on rally in stocks in the ensuing months.

However, the landscape today may not favor an issuance weighted towards bills, as the year-end conditions have shifted notably. Yields on bills now marginally exceed the Fed’s overnight repo facility rate and have seen a substantial decline in cash levels. The shift in numerical dynamics poses a riddle for the Treasury’s upcoming decision on debt issuance.

There is a strong case for greater issuance of debt on the coupon side of the equation, given the cheaper cost to issue longer-term debt today. Nevertheless, it also poses a risk of causing a rigidity in financial conditions.

FOMC Meeting and its Implications

The Fed’s meeting later on January 31, while important, may pale in comparison to the market-shaping power of the Treasury’s decision. Economic data strength notwithstanding, a measured approach is incumbent upon the Fed to avoid premature rate cuts that could potentially exacerbate market dynamics.

Financial Forecast: Market Insights for the Week of Jan 31, 2025

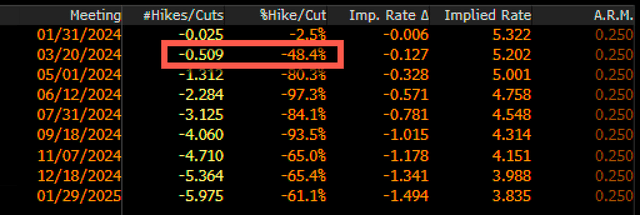

As the final week of January sets in, investors brace themselves for what could well be a watershed moment in the ever-evolving financial landscape. The Federal Reserve, in its ongoing mission to stave off economic stagnation and trigger inflation, will likely continue to resist market expectations for cuts. In refusing to bow to the six rate cuts currently priced into the Fed Funds futures through January 29, 2025, the Fed seems poised to maintain its steadfast stance, dashing hopes of imminent rate cuts despite market sentiment. Furthermore, the possibility of rate cuts in March, still holding a 50% chance according to market odds, could be in for a disappointing rebuff from the Fed.

February 1 – Earnings

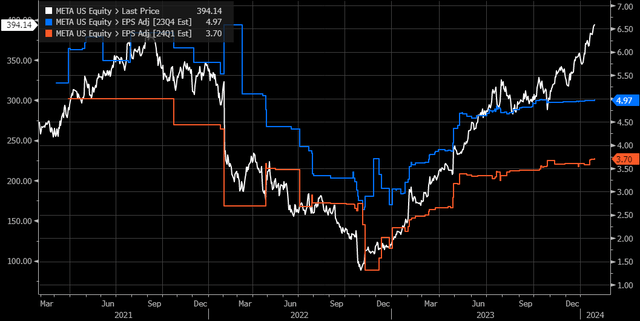

This week’s attention will rapidly refocus on earnings as tech giants Apple (AAPL), Amazon (AMZN), and Meta (META) are set to release their latest financial results after trading hours on February 1. Of particular interest will be Meta, which has experienced a meteoric rise in its stock value since its previous earnings release. Analysts note a flattening of earnings estimates for the fourth and first quarters, suggesting that the stock’s rally has been primarily fueled by an expansion of the earnings multiple, heightening expectations for a sustained surge in earnings growth, despite a lack of tangible evidence to support such anticipations.

February 2 – Jobs

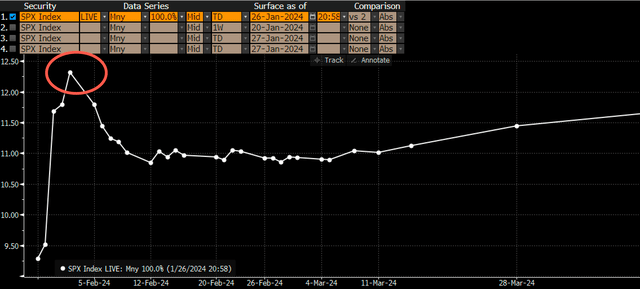

The week concludes with the much-anticipated job report, with analysts forecasting a slowdown in job growth to 180,000 from December’s 216,000, accompanied by a rise in the unemployment rate from 3.7% to 3.8%. Of even greater significance is the expected 0.3% m/m rise in average hourly earnings, down from 0.4% in December, while the y/y increase remains at 4.1%, mirroring the growth rate of the previous month. Intriguingly, despite potentially market-moving news throughout the week, the options market assigns the highest risk to the jobs report on February 2, as indicated by the peak implied volatility.

While it may seem just another week in January, the collective impact of the events during this week could potentially mark a pivotal moment in the financial cycle, altering the narrative that has unfolded over the past few months in unforeseen ways.

This is no week for a leisurely vacation.