As economic activity regains traction and consumer spending sees an upswing, there’s a positive outlook for retail and consumer sectors. A forthcoming rate cut combined with easing inflation is expected to spur higher consumer spending. With the prospect of more affordable mortgages and auto loans on the horizon, consumers will have extra room for discretionary purchases. This economic shift directly bodes well for restaurant stocks.

With pleasant anticipation of leisurely summer days, school holidays, and an increase in dining out, consumers are gearing up to allocate funds, with dining expenses reigning high. As consumer wallets grow heavier, the restaurant industry is poised to thrive. For investors aiming to capitalize on this surge in consumer spending, the time is ripe to explore these seven tantalizing restaurant stocks.

Facing the Golden Arches: McDonald’s (MCD)

Securing McDonald’s (NYSE:MCD) stock at a sub-$300 price point stands as an astute move as the company grapples with a recent slowdown in growth per management signals. This year, the stock has seen a 7% decline but has rebounded from $257 to its current standing at $300 over the last half-year. Despite facing a plateau in sales growth, McDonald’s continues to exhibit profitability. By excelling in the franchising realm, the company manages to maintain low operating costs while fostering revenue uplift. An impressive 9% climb in comparable store sales was recorded in 2023. McDonald’s, although currently navigating a growth deceleration, remains a profit-generating entity. With a strategic Krispy Kreme partnership on the cards to introduce doughnuts to its menu, McDonald’s dividend yield at 2.42% and a remarkable 48-year streak of consistent dividend growth further sweeten the investment proposition.

Navigating the Coffee Culture: Starbucks (SBUX)

The renowned global coffee chain, Starbucks (NASDAQ:SBUX), has etched its name firmly in consumer consciousness. Acknowledged for its brand prestige, Starbucks is currently expanding its global footprint, eyeing a lofty goal of 55,000 stores worldwide by 2030, a sharp rise from its existing 36,000 outlets. Presently positioned near its yearly low, Starbucks stock has faced a 4% dip in recent times, trading at $88. While a current sales slump partly contributed to this decline, the setback is viewed as temporary. Despite reports of reduced consumer footfall in the U.S., Starbucks continues to demonstrate financial resilience. Global comparable store sales saw a 5% upswing, fueled by a 3% surge in consumer visits and a 2% increase in average consumer spending. Efforts to slash costs and introduce innovative products are underway to bolster sales. Boasting robust cash flow to support consistent dividend payouts, Starbucks stock currently offers a dividend yield of 2.57%, presenting an attractive window for investment at a discounted valuation.

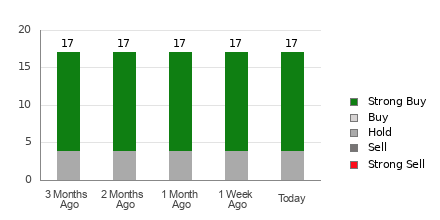

Pizza Empire’s Rise: Domino’s Pizza (DPZ)

Source: Ken Wolter / Shutterstock.com

Rising to its 52-week peak, Domino’s Pizza (NYSE:DPZ) stock has been on a soaring trajectory. With a 22% year-to-date surge and a remarkable 53% uptick over the past year, Domino’s Pizza stands out as a frontrunner in the fast-food domain. Operating as the globe’s largest pizza conglomerate, Domino’s continual market expansion, revenue growth, and widening market share accentuate its appeal. Pizzas, a timeless culinary delight, ensure the company remains ever pertinent. A staggering 99% of its sites are franchised, enabling Domino’s to amass royalties and fees sans operational expenses. This model has fueled speedy outlet expansions in recent years, with profitable franchisees paving the way for fresh setups in novel territories. With a lean-margin and asset-light operational structure, Domino’s emerges as a perennially lucrative investment proposition. Priced at $505 and poised to soar higher amidst improving consumer spending, the stock couples a 1.19% dividend yield with sustainable dividend disbursements.

The Consumable Conglomerate: PepsiCo (PEP)

Source: FotograFFF / Shutterstock

PepsiCo (NASDAQ:PEP) commands a top spot among restaurant stocks owing to its vast portfolio of brands. This juggernaut extends beyond beverage realms, boasting hefty revenue streams from Frito-Lay and Quaker Oats within North America. Championing as a global icon with a rich legacy, PepsiCo has adeptly diversified to align with evolving consumer preferences. Scaling heights via diversification into snacks and health-focused fare, the company stands poised to capitalize on enhanced consumer spending and the forthcoming summer surge. Profiting from a robust international presence and a diversified operational framework, PepsiCo is poised for another year of commendable growth in 2024. Despite soda consumption ebb, the snack segment serves as a reliable revenue driver for PepsiCo, ensuring sustained profitability.

Embracing the Flavorful Stocks in the World of Dining

Chipotle Mexican Grill (CMG)

Chipotle Mexican Grill (NYSE:CMG), a titan in the fast-food landscape, is akin to an artisan dish – meticulously crafted and highly sought after. With over 3,400 locations and ambitious plans for expansion, Chipotle’s taste resonates with investors, even at a hefty price of $2,895 per share.

The stock, much like a succulent meal, has left investors craving for more, delivering a 28% return year-to-date and a wholesome 66% growth over the past year. Basking in the afterglow of impressive quarterly results, Chipotle enjoyed a 15.4% year-over-year revenue surge to $2.5 billion, coupled with a 27% surge in earnings per share, reaching $10.21.

Not resting on its laurels, the company proclaimed a 50-for-1 stock split, an appetizing move poised to lure in more investors as Wall Street anticipates a continuing streak of earnings growth.

Shake Shack (SHAK)

Engaging the palates of consumers far and wide, restaurant chain Shake Shack (NYSE:SHAK) is on a culinary conquest, now eyeing the Canadian market. Renowned for its delectable burgers and unique offerings, Shake Shack stands out amidst its contemporaries.

Trading at $102, SHAK stock has sizzled with a 39% year-to-date surge, akin to a dish that keeps getting better with every bite. From $68 at the year’s onset to over $100 presently, Shake Shack’s upward trajectory has been a feast for shareholder’s eyes.

Bolstered by a 2.8% uptick in same-store sales and a savory 20% revenue climb to $286.2 million, Shake Shack’s earnings per share of $0.02 heralds a flavorful turnaround from the previous year’s loss. With consumer spending on the rise, Shake Shack’s rally appears poised for a sustained surge.

Restaurant Brands International (QSR)

For investors seeking a slice of the consumption sentiment pie, Restaurant Brands International (NYSE:QSR) emerges as a delectable choice. A juggernaut encompassing a suite of prestigious brands including Burger King, Tim Hortons, Popeye’s, and Firehouse Subs, QSR stands tall as a world-class entity.

Priced at $76, QSR stock exudes an aura of undervaluation, garnished with a robust 3.03% dividend yield to attract passive income enthusiasts. With aspirations to burgeon to over 40,000 locations by 2028, enhanced by a formidable cash flow profile facilitating consistent dividend payouts, QSR embodies an investment recipe for sustained growth.

Through strategic refurbishments at Burger King outlets and proactive marketing initiatives, QSR is poised to nurture steady sales growth. Representing a diversified entity, QSR offers investors a gateway to not just growth but also a stream of passive income, akin to savoring a long, satisfying meal.

On the date of publication, Vandita Jadeja did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.