What the Widening Gap Suggests for the S&P 500

Over time, the stock market reflects a company’s financial performance. While this seems reasonable, short-term market sentiment often takes the wheel. Positive sentiment can drive stock prices beyond their earnings, while negativity can pull them down.

Assessing the Concerning Gap

Examining a 10-year chart depicting the S&P 500’s price and the estimated 12-month earnings per share, a glaring disparity catches the eye.

This stark contrast is the second widest in the last decade. What happened the last time such a gulf emerged? The S&P’s price plummeted during the 2022 bear market, a correction that better reflected the actual earnings.

Revisiting the “Toxic Trifecta”

From late July to late October, the S&P suffered an 8% blow, and the Nasdaq dropped by 12%. This slump was attributed to the “Toxic Trifecta” – the climbing 10-year treasury yield, the strengthening U.S. dollar, and rising oil prices.

However, following cooler inflation readings and expectations of a rate-cut bonanza in 2024, the S&P and the Nasdaq bounced back, registering a 22% and 26% surge, respectively.

Resurgence of the Toxic Trifecta

Despite laying dormant since late December, the Toxic Trifecta has shown signs of a resurgence, casting a shadow on the market’s outlook.

The higher the 10-year treasury yield climbs, the more it strains the market. A stronger U.S. dollar creates currency headwinds for international companies and dents their stock prices. Additionally, rising oil prices lead to increased expenses for businesses, eating into profits.

The Impact of the “Toxic Trifecta” on Investors

Preceding the Toxin Trifecta’s emergence, global markets had their eyes peeled for the merging of the toxic threesome: the 10-year Treasury yield, the strength of the dollar, and the oil market amid all the talk about a degree of inflationary pressure. Since late December, their worst suspicions have been realized.

The 10-Year Treasury Yield Surge

Within a matter of weeks, the 10-year Treasury yield has made dramatic progress, jumping from about 3.78% to around 4.30%. If looked at from a historical standpoint, this leap is markedly fast and impacts the wider economy, particularly the housing and stock markets. What does this tell us? Investors, buckle up, stay sharp, and get your risk assessment tools handy.

The Mighty Dollar’s Ascent

In one of the most jaw-dropping hikes, the dollar has ascended from around 100 to nearly 105. Its vigor reflects the market’s sensitivity, an impending sign of hesitation and possible skepticism, as traders weigh their moves cautiously.

The Unrelenting Oil Market

Meanwhile, the oil market has made its presence known, climbing from the upper 60s to the upper 70s. This steady surge is yet another addition to the brewing toxic cocktail, likely casting a shadow of unease among market participants.

Stocks’ Resilience Amid Turmoil

While these unsettling developments might prompt any investor to brace for impact, the stock market has remained remarkably resilient. Notably, though the S&P and the Nasdaq encountered a disconcerting dip between Christmas and early January, they soon regained foothold and even reached all-time highs. All this while, continuing to climb against the undertow of the Toxic Trifecta..

Why hasn’t the strengthening of the Toxic Trifecta dampened stock prices?

In truth, Wall Street has been unwavering in its belief that the year 2024 would usher in a succession of hurried and aggressive rate cuts, refusing to acknowledge cautionary cues from Federal Reserve members.

Wall Street has virtually turned a blind eye to the formidable Toxic Trifecta, adamantly convinced that the looming threat posed by the Fed’s “higher for longer” mantra was nothing more than empty talk. The prevailing optimism is that the positive impetus of lower rates would outmuscle any adverse factors.

The Truth Behind the Latest CPI Data

Upon closer inspection, yesterday’s Consumer Price Index (CPI) reading wasn’t as dire as one might infer. The numbers indicate a continuing downward trajectory for inflation. So why did the market spiral into turmoil?

The data came in slightly hotter than expected, shattering hopes of substantial rate cuts commencing this spring. This unexpected turn jolted Treasury yields, casting doubt on whether the Federal Reserve would be able to execute multiple rate cuts over the coming months, a key element to Wall Street’s bull case for the equity market.

Mid-December witnessed an upsurge in positive sentiments after the Fed updated its Dot Plot, with Wall Street pricing in a promising scenario entailing six quarter-point cuts in 2024, a number twice as high as the Dot Plot showed. However, the subsequent tough-toned narratives from Fed members compelled futures traders to revise their forecasts, scaling down their expectations.

In a post-CPI print scenario, the December 2024 fed funds target range, with the highest likelihood, ranged between 4.25% – 4.50%. This represented four expected quarter-point hikes for the year. Such high odds and forecast shifts vividly illustrate the delicate balance that the market is attempting to strike amid the challenging economic landscape.

The Federal Funds Rate Dilemma: Wall Street’s Reluctance to Recalibrate

Amidst the complex web of financial markets, futures traders have finally realigned their expectations for rate cuts. However, the Street’s steadfast refusal to reassess stock prices is bewildering. Only last Friday, the S&P triumphed at its apex of 5,026.61. As of today, equities exhibit resilience in the face of recent pullbacks, evoking skepticism.

Repricing Stocks: A Lagging Story

Amidst the whirlwind of market activity, the expectation had loomed that December 2024 would herald a target range of 3.50% – 3.75%, a staggering seven quarter-point cuts below today’s anticipated range. The discrepancy is alarming—futures traders have made strides to calibrate their anticipation, yet Wall Street exhibits inertia in denting stock evaluations.

An Impervious Stance

- The Fed remains resolute in its reluctance to adopt a precipitate approach towards rate reduction and the extent thereof.

- There exists a palpable divergence between the S&P’s valuation and the anticipated 12-month S&P earnings.

The challenge persists: the confluence of factors favoring recessionary market conditions fails to dampen the bullish fervor. It is disquieting to witness an environment of recalibration bereft of any discernible impact on stock valuations.

Maintaining a Balanced Perspective

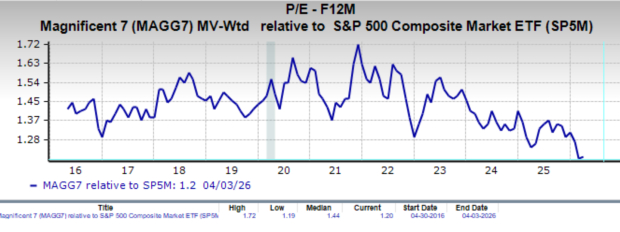

Given the overvaluation of the select “Magnificent Seven” stocks, and the danger inherent in broad market assessments, prudence calls for a meticulous review of one’s portfolio. A critical examination is essential: How does one’s portfolio navigate stocks with inflated valuations? How sustainable are stocks that rely on rate cuts for performance?

While exercising caution, it is imperative to explore potential opportunities that may arise should the market undergo substantial correction. Amid forebodings of market volatility, it is prudent to prepare one’s watch list for investment prospects.

An array of top-tier AI stocks, extending beyond the stratosphere of the Magnificent Seven, holds promise. Should a market downturn materialize, it may unravel compelling investment prospects in the domain of small- and mid-cap AI stocks.

Addressing the mounting headwinds facing the S&P, investors must brace themselves for oscillations within their existing portfolio, practice vigilance over deteriorating stocks, and prepare to capitalize on the emergence of sound investment opportunities.

Wishing you an insightful evening,

Jeff Remsburg