Investment Profile

The Trade Desk (NASDAQ:TTD) has carved a remarkable path in the digital advertising industry, leveraging its innovative programmatic advertising techniques and its exclusive focus on the demand side platform (‘DSP’). The company’s stronghold in the Connected-TV (‘CTV’) and Retail Media sectors position it favorably. Amidst the evolving digital landscape following Google’s shift away from ‘Cookies’, The Trade Desk’s identity solution, UID2, has a golden opportunity to capture a substantial market share. Despite its exceptional performance and resilient competitive position, TTD currently trades at 40x EV/EBITDA, significantly higher than the industry average of approximately 10x. This premium valuation, coupled with a slowdown in growth and competitive ambiguities, presents a cautionary tale for potential investors, reinforced by my fair value estimate in the mid-$30s.

The Evolving Digital Advertising Landscape

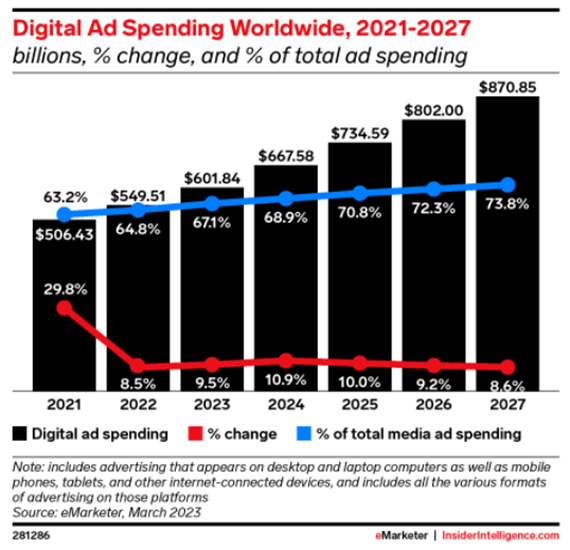

The digital advertising domain has experienced exponential growth over the past decade, with an annual surge of nearly 20% from 2011 to 2021, surpassing traditional advertising. Despite a post-pandemic normalization in growth, global digital ad spend surpassed $600 billion in 2023 and is projected to close in on the $1 trillion mark by 2030.

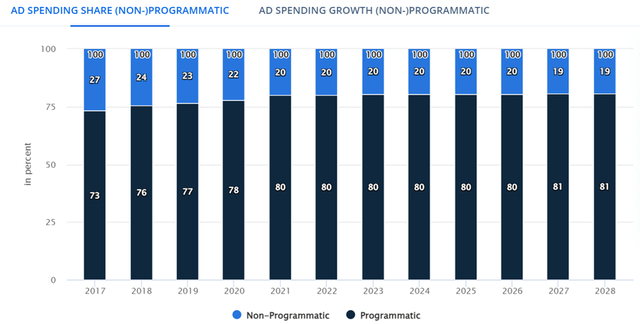

Innovations in the mid-2000s precipitated the emergence of programmatic advertising, harnessing consumer data and machine learning to assist advertisers in identifying and acquiring optimal media placements, thereby enhancing return-on-ad-spend (‘ROAS’) and refining campaign efficacy. The surge in the number of internet users and digital media consumption propelled the explosive growth of programmatic advertising, capturing a substantial 80% of ad expenditures, a trend likely to endure.

With the widespread adoption of programmatic technology, the competitive landscape has expanded, although major players such as Google, Facebook (META), and Amazon (AMZN) wield significant control. Google has long dominated the advertising sphere, particularly in video and search ads. The impending phase-out of Google’s legacy internet identity solution, Cookies, announced in 2020, is poised to trigger a monumental upheaval in digital advertising. Despite the maturity of the digital advertising industry, ample demand remains untapped – an arena where The Trade Desk stands tall.

The Trade Desk Strategy & Prospects

Turning our focus to the realm of identity, The Trade Desk was an early advocate for developing an alternative identity solution to Cookies, unveiling the Unified ID (‘UID’) in 2018, eventually advancing to UID 2.0. UID2 allows users to voluntarily share data and employs basic identifiers such as emails and phone numbers to facilitate precise ad targeting. The technology’s omnichannel capacity to capture these identifiers across diverse online platforms, alongside robust encryption measures, positions it as a favorable alternative with the impending obsolescence of Cookies.

Although UID2 does not currently yield direct revenue for The Trade Desk, its ascension as the preferred identity solution could catalyze an influx of advertisers and publishers to its platform, streamlining data aggregation and enhancing its market foothold.

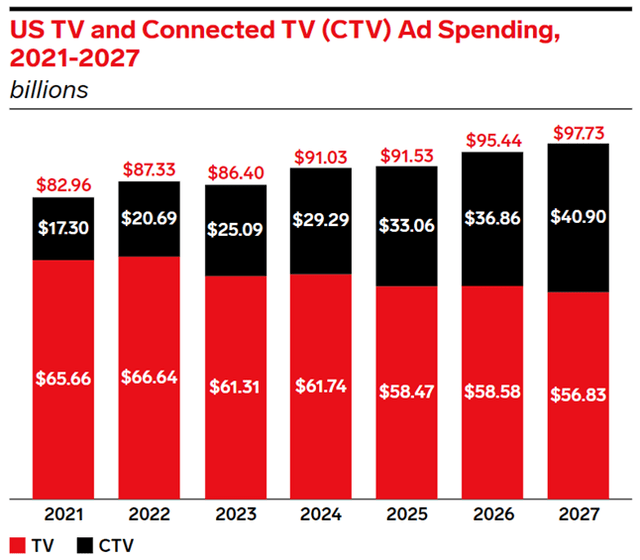

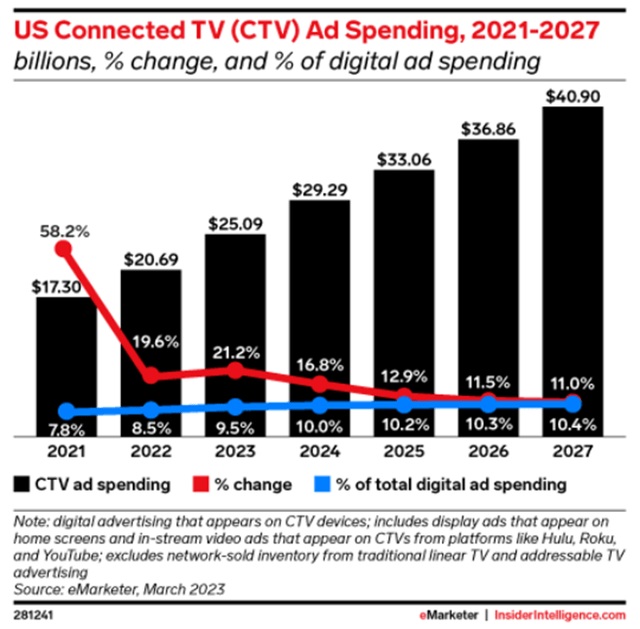

With the advent of Connected-TV (‘CTV’) and Retail Media, The Trade Desk is stoking its growth engines. Traditional TV viewership has dwindled below 50%, with streaming accounting for nearly 40% of total viewership, primarily through CTV. Recognizing this trend, The Trade Desk swiftly capitalized on the burgeoning CTV domain, and its prescience has paid dividends, with approximately 40% of its revenues stemming from Video, predominantly composed of CTV. Furthermore, the exponential growth of the e-commerce sector has propelled the rapid expansion of Retail Media networks, providing a fertile ground for The Trade Desk’s future expansion, evident through partnerships with large retailers such as Walmart and Target.

The Trade Desk’s foray into these evolving markets and its proactive stance on identity solutions position it as a prospective long-term victor amidst a dynamic and competitive landscape.

The Trade Desk: Breaking Barriers in Programmatic Advertising

Can The Trade Desk continue to compete against industry titans like Google, Adobe, and Amazon? There’s no ignoring TTD’s impressive track record with a 36% annual revenue growth over the past 5 years, outperforming the industry, and a stock surge of 390%. These figures hint at existing (or potential) competitive advantages.

Economic Moat

The Trade Desk established itself as a programmatic advertising pioneer, laying the groundwork for early adopters like Google and Facebook. Founded in 2009, the company’s success is attributed to its top-notch offerings and the difficulties faced by competitors in replicating them. Leveraging machine learning techniques and data, The Trade Desk’s early entry into this technical domain has bestowed it with a natural advantage, resulting in superior models and data as the business expands. The platform’s excellence is affirmed by its highest rating against peers on Gartner, underscoring its quality.

Furthermore, The Trade Desk’s independence as a demand-side platform separates it from the likes of Google and Facebook, which often straddle both supply and demand of ad-inventory. The latter companies’ dominance in both supply and demand has come under scrutiny, with antitrust suits and allegations of market consolidation and collusion. In contrast, The Trade Desk’s exclusive focus on demand-side operations has earned it the trust of advertisers by putting their interests at the forefront. A recent introduction of sub-floor bidding tactics serves to strengthen this trust and reduce costs for advertisers, giving the company a competitive edge.

Fundamental Drivers & Valuation

Following a 24% dip in TTD shares after its Q3 release in November, the company cited lower Q4 revenue guidance than anticipated by analysts. While YoY growth rates have cooled since Q1 2022, full-year 2023 growth is projected to remain in the low 20s. The management has attributed the slowdown to tougher YoY comparables and macro challenges but remains optimistic about the future, foreseeing opportunities over the next two years.

Wall Street analysts are anticipating an average annual revenue growth of approximately 20% for the next five years. A base case revenue forecast predicts a 16% annual growth through 2032, leveraging CTV and Retail Media demand as well as a growing share of the identity market. The Trade Desk has maintained strong gross margins in the low 80s, bolstered by its capital-light model and economies of scale. However, the company has seen operating margins and returns on capital dwindle due to increased operating expenses, particularly in general & admin expenses which have almost doubled to 33% of revenues in the last 5 years. An increase in headcount by 15-17% in 2024 is expected to further amplify operating spend, challenging the company’s historically strong revenue growth and indicating a lack of operating leverage.

Despite these challenges, The Trade Desk’s strong reputation, proven track record, and continuous innovation position it as a formidable force in the programmatic advertising arena. As the company forges ahead, investors will be watching closely to see how it navigates the complex digital advertising landscape and maintains its competitive edge.

The Trade Desk: A Glimpse Into the Wild World of Digital Advertising

The State of Affairs

As an investor or observer, it’s infinitely fascinating to peek behind the curtain of a company and behold its innermost workings. The Trade Desk, a prominent player in the digital advertising landscape, has laid bare an intriguing landscape thriving with potential and risks in equal measure. The illustrious company has voyaged through choppy waters, charting a course through competition from digital titans such as Google, Amazon, and Facebook. The nature of the digital advertising industry is resoundingly dynamic, fraught with uncertainty due to regulatory reforms, technological shifts, and legal challenges. The depreciation of Cookies, Apple’s stringent data privacy measures, and antitrust lawsuits have undoubtedly loomed large, casting shadows of uncertainty.

Challenges & Triumphs

Amid the tumultuous terrain, The Trade Desk has emerged as a stalwart, navigating these treacherous waters for over a decade and demonstrating the resilience required to withstand the tempest of change. The company has deftly surfed the undulating waves of the digital advertising realm, perpetually in tune with the pulse of the consumer. Yet, an adversarial macroeconomic climate can imperil the adorning crown of the advertising industry. A constricting economic backdrop can strain advertiser budgets, potentially impacting The Trade Desk’s performance. Notwithstanding, the company has exhibited commendable resilience through the trials of 2022 and 2023, culminating in impressive growth and stock price performance.

Risks & Uncertainty

The digital advertising industry isn’t a tranquil oasis; it’s a battleground fraught with perils and chock-full of risks. The Trade Desk faces a litany of external and internal threats, from the might of behemoths like Google, Amazon, and Facebook to internal fissures such as excessive stock-based compensation. Regulatory entanglements and structural upheavals have only added to the complexity of the company’s operating environment. Moreover, the alluring promise of digital advertising is intricately intertwined with the fluctuations of the consumer sphere, where a contracting macroeconomic backdrop can potentially cast a shadow on The Trade Desk’s performance.

Moreover, the internal dynamics of The Trade Desk present their own set of challenges. The specter of excessive stock-based compensation (‘SBC’) has long been a source of contention, posing a tangible cost to shareholders. Although share buybacks have served as a bulwark against the dilutive effects of SBC, it continues to account for a substantial 27% of TTM revenues. Furthermore, founder and CEO Jeff Green wields a formidable 48% voting power, engendering the specter of key person risk. Nonetheless, Green’s stewardship has been exemplary, steering the company through turbulent waters and signaling a continued trajectory of robust leadership.

Conclusion

The journey of The Trade Desk is veritably a saga of triumphs and tribulations, an odyssey through the capricious currents of the digital advertising universe. The company has sprawled its wings, outshining the broader digital advertising industry, and solidifying its stature as a preeminent DSP. The alluring promise of the burgeoning CTV, Retail Media, and Identity segments augurs well for the company’s long-term prospects. However, in the unforgiving realm of investments, the allure of a great company does not always translate to a sound investment. While The Trade Desk stands as an illustrious beacon, casting its luminous glow over the digital advertising landscape, its lofty valuation, coupled with waning growth and burgeoning operational expenses, has given pause to astute investors.