Delta Air Lines, a renowned global player in the aviation industry, is not just another airline ferrying passengers. It operates as a “plutonomy stock,” positioned to benefit from the prevailing trend of wealth concentration among the affluent elite in society.

While this phenomenon is subject to debate, the potential investment attractiveness of Delta warrants consideration for those anticipating the longevity of this trend.

The Trifecta Behind Delta’s Plutonomy Status

One compelling aspect is the acknowledgment by Delta’s management during its 2023 Investor Day that 75% of the aviation industry’s revenue is derived from households with an income exceeding $100,000, representing the top 40% of consumers in the country.

Delta’s strategic emphasis on the premium segment, rather than budget travel, positions it to consistently draw revenue from high-end clientele, presenting a stable investment proposition.

|

Delta Revenue |

2014 |

2019 |

2023 |

CAGR 2014-2023 |

CAGR 2019-2023 |

|---|---|---|---|---|---|

|

Loyalty & Other |

$8 billion |

$10.1 billion |

$14.5 billion |

6.8% |

9.4% |

|

Premium |

$9.6 billion |

$15 billion |

$19.1 billion |

7.9% |

6.2% |

|

Main Cabin |

$22.4 billion |

$22 billion |

$24.5 billion |

1% |

2.7% |

|

Total |

$40 billion |

$47.1 billion |

$58.1 billion |

4.2% |

5.4% |

Data source: Delta Air Lines SEC filings. CAGR=compound annual growth rate. Table by author.

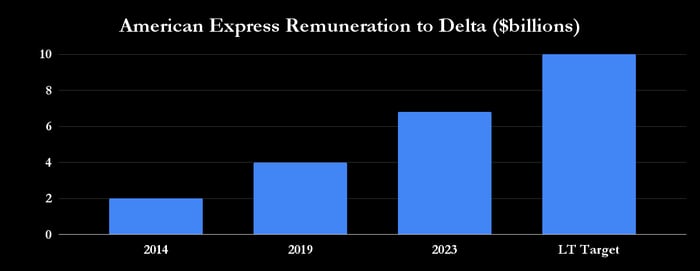

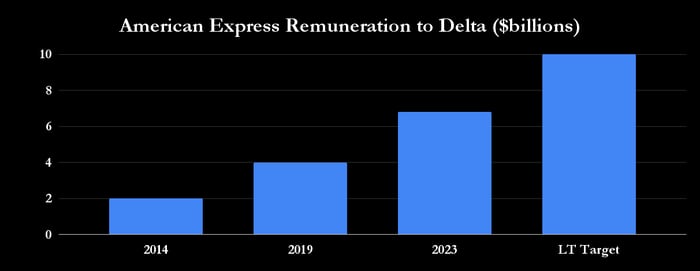

Furthermore, Delta’s robust SkyMiles program, in collaboration with American Express, has emerged as a significant revenue generator. Notably, the partnership with American Express has seen spending through Delta American Express credit cards equivalent to almost 1% of the U.S. GDP, with the remuneration from American Express showing significant growth potential.

According to management, this relationship is poised to reach a staggering $10 billion in the long run.

Data source: Delta Air Lines presentations.

Unveiling Delta Air Lines’ Ace in the Hole

When the threads of Delta’s premium focus, revenue growth strategy, and the SkyMiles program are interwoven, a potent secret weapon emerges. Should income inequality persist, the concentration of spending among higher-income demographics is likely to benefit companies adept at capturing these clientele—a feat Delta has seemingly achieved through its SkyMiles program.

By the latest count on Investor Day last June, Delta boasted 25 million active SkyMiles members, with 30% holding a co-branded credit card. The airline’s dedication to attracting younger, affluent customers through innovative offers like free Wi-Fi and partnerships with brands such as Starbucks has paid off.

Image source: Getty Images.

This has led to a decrease in the average age of new SkyMiles members, along with a surge in premium revenue contribution from the program, evidencing a shift to higher-margin premium services.

Challenges on the Horizon for Delta’s Growth Trajectory

Amidst the prospects of a slowing economy and air travel demand, Delta faces potential headwinds from heightened regulation in the credit card sector and increasing customer discontent with loyalty programs. The crux lies in customers investing in accruing miles without commensurate benefits in redemption options, threatening the sustainability of the SkyMiles program and co-branded card usage.

Image source: Getty Images.

An Opportunity to Seize?

Delta not only rides the wave of the aviation sector resurgence but strategically pivots towards serving premium demographics and loyalty-generated revenues. This makes it an enticing prospect for investors, especially with an estimated 2024 earnings multiple of just below 7 times.

Could this be the moment to invest in Delta Air Lines?

Before diving into Delta Air Lines’ stock, it’s prudent to note that while Delta appears promising, the Motley Fool Stock Advisor team has singled out 10 other stocks with the potential for significant returns in the foreseeable future—Delta Air Lines not being among them.

Stock Advisor equips investors with a comprehensive guide to building a successful portfolio, inclusive of frequent updates, expert insights, and bi-monthly new stock recommendations, significantly outperforming the S&P 500 since 2002*.

Explore the top 10 picks

*Stock Advisor returns as of March 25, 2024

Lee Samaha holds no positions in mentioned stocks. The Motley Fool has stakes in and endorses Starbucks. The Motley Fool advocates for Delta Air Lines. The Motley Fool abides by a disclosure policy.

The opinions expressed herein are solely those of the author and do not reflect Nasdaq, Inc.’s views and opinions.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.