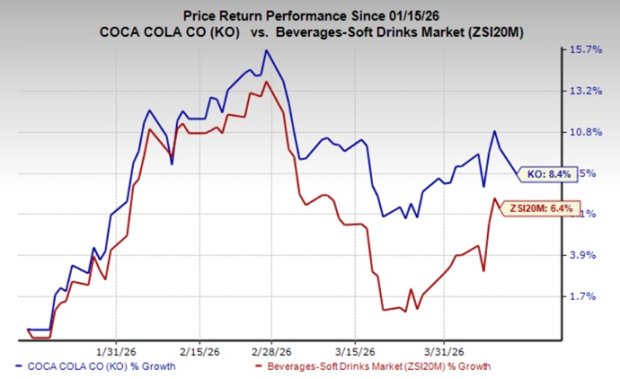

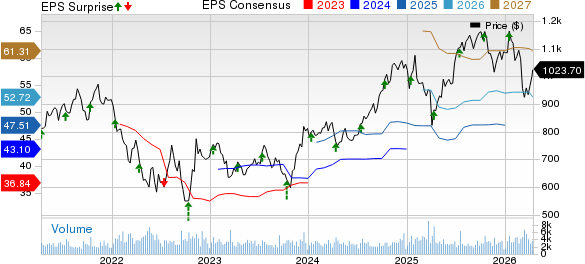

Many people are familiar with the phrase, “There’s more than one way to skin a cat.” The underlying principle, that there are often multiple ways to achieve a specific goal, rings true. In the realm of retirement savings, Americans have numerous options. Individual retirement accounts (IRAs) and health savings accounts (HSAs) are popular choices. However, there’s another account that stands out as a favorite for building a millionaire retirement.

Image source: Getty Images.

The Appeal of the Roth 401(k)

Contributing to various retirement accounts is a common practice. While maximizing contributions to a Roth IRA is one approach, a compelling alternative exists in the form of the Roth 401(k) plan.

The concept of 401(k) plans was introduced with the passage of the Revenue Act of 1978. Section 401(k) within this legislation enabled employees to receive a portion of their income as tax-deferred compensation.

In contrast to traditional 401(k) plans, where income taxes are deferred on contributions, the introduction of Roth 401(k) plans in 2006 came with a different tax structure. Contributions to Roth accounts require immediate tax payment, but subsequently, the account grows tax-free, with withdrawals becoming accessible at age 59 1/2 as long as the account has aged at least five years.

The Allure of Tax-Free Growth

The tax-free growth characteristic of Roth 401(k) plans is arguably the most appealing feature. Although taxes are paid on contributions to any 401(k) account, the absence of taxes on gains within a Roth account could potentially yield larger returns over time. This becomes especially significant in the context of potential tax hikes owing to the substantial U.S. debt burden.

An additional advantage comes in the form of the lack of required minimum distributions with Roth 401(k) plans, a feature not shared with traditional 401(k) plans, which mandate RMDs once the account holder reaches age 72.

Unlike IRAs, which cap annual contributions at $7,000 (or $8,000 for individuals over age 50) and HSAs, where contribution limits are set at $4,150 or $8,300 for family coverage (with an additional $1,000 contribution allowed for individuals over age 55), Roth and traditional 401(k) plans boast significantly higher employer contribution limits of $23,000. In addition, employers are often incentivized to match contributions to 401(k) accounts, constituting a valuable way to bolster retirement savings.

Retiring as a Millionaire

The prospect of retiring with a million-dollar-plus nest egg via a Roth 401(k) largely hinges on consistent contributions, a lengthy investment horizon, and the compounded annual growth rate. Attainment of a retirement account exceeding $1 million is realistically achievable for many individuals.

- Assuming a monthly contribution of $1,000 over a 35-year career

- With an average annual return of 7%

These conditions would result in an accumulated Roth 401(k) balance of over $1.8 million at the end of the 35-year period, exclusive of any employer matches.

Considering the Drawbacks

One drawback of Roth 401(k) plans is their non-uniform availability among employers. However, data from the Plan Sponsor Council of America indicates an encouraging trend, with over 89% of companies offering a Roth option as a part of their 401(k) plans, a notable increase from the 58.2% reported in 2013.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets”

The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.