Devon Energy (NYSE: DVN) initiated a groundbreaking trend in capital returns post its transformative merger with WPX Energy in early 2021. The company set forth a unique fixed-plus-variable dividend policy. This policy comprised a fixed base quarterly dividend and an additional variable dividend of up to 50% of its free cash flow.

Many oil stocks have since followed in Devon Energy’s footsteps by introducing parallel fixed-plus-variable dividend policies. Among them is Chord Energy (NASDAQ: CHRD), which is now emulating Devon’s playbook by entering into an agreement to acquire Enerplus (NYSE: ERF), a company that Devon itself had looked to purchase initially. Let’s delve into how this acquisition could benefit dividend investors and examine potential future prospects for Devon as it continues to drive its dividend payouts.

Deconstructing the Acquisition Deal

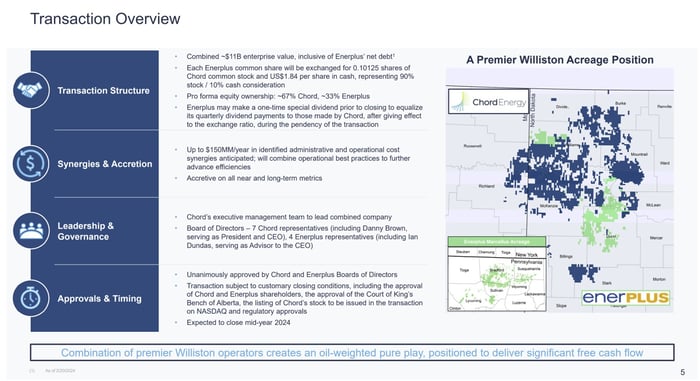

Chord Energy is set to acquire Enerplus through a mix of cash and stock, valuing the target at approximately $3.9 billion (including debt). The equity portion of $3.4 billion will be paid out in stock (0.10125 of Chord’s shares for each Enerplus share) with the remainder in cash ($1.84 per share), resulting in the formation of an $11 billion oil and gas entity in terms of enterprise value.

Enerplus fits seamlessly into Chord Energy’s strategy:

Image source: Chord Energy.

The transaction will expand Chord Energy’s acreage in the Williston Basin, consolidating their combined holdings to almost 1.3 million net acres with a daily production capacity of 279,000 barrels of oil equivalent (BOE/d), thereby making them the top regional producer. This increased scale forms the foundation for up to $150 million in annual cost synergies. With Enerplus also holding non-operated interests in the Marcellus shale, Chord may explore divesting these assets to strengthen their financial position.

The anticipated cost efficiencies from the merger are projected to amplify Chord’s free cash flow. The merged entity targets generating about $1.2 billion in free cash flow for the year (up from $800 million pre-merger). Chord plans to allocate 75% of these funds to shareholders through base dividends, variable dividends, and share buybacks.

Exploring Alternative Paths for Devon

As reported by Reuters, Devon had advanced an acquisition proposal to Enerplus. An acquisition of Enerplus would have significantly bolstered Devon’s footprint in the Williston Basin, where it currently operates at a smaller scale compared to Enerplus (54,000 BOE/d versus Enerplus’ 78,000 BOE/d).

Furthermore, Devon was among the contenders exploring a potential acquisition of CrownRock before Occidental Petroleum‘s $12 billion agreement. CrownRock could have further strengthened Devon’s existing premier position in the Delaware Basin. Discussions were also held regarding a merger between Devon and Marathon Oil. However, negotiations ceased due to differing terms.

Keeping pace with the consolidation wave in the oil sector, Devon is just one name amidst many seeking to engage. Starting with Exxon‘s takeover of Pioneer Natural Resources for over $60 billion last year, the trend was followed by Chevron‘s acquisition of Hess for roughly $60 billion and Diamondback Energy‘s $26 billion acquisition of privately-held Endeavor Energy Resources.

Despite several targets being claimed, Devon still possesses ample options. It could reevaluate a potential merger with Marathon or explore possibilities with Permian Resources, a strong contender in the Delaware Basin like Devon, or Matador Resources, operating in the Delaware and Eagle Ford Basins alongside the gas-rich Haynesville Shale and Cotton Valley formations. The key lies in identifying a target that complements Devon’s scale and cash flow, empowering the company to augment free cash flow and thus enhance dividend payments.

Awaiting the Ideal Opportunity

Devon Energy’s merger with WPX Energy heralded significant value creation for its shareholders in 2021. The resultant boost in free cash flow provided the impetus for the adoption of their widely acclaimed fixed-plus-variable dividend policy, a strategy that has inspired others, including Chord Energy. As Chord now proceeds to acquire the same firm Devon had set its sights on, this move promises a bright future for dividend recipients.

Nevertheless, missing out on another acquisition bid does not signal defeat for Devon. With ample opportunities amidst the ongoing industry consolidation wave, the company can unlock further value creation once the right deal materializes.

Thinking about investing in Devon Energy?

Before making any investment in Devon Energy, it’s crucial to consider the following:

The Motley Fool Stock Advisor team recently singled out what they believe are the 10 top stocks for investors to explore now… and Devon Energy wasn’t one of them. These chosen stocks present the possibility of substantial returns in the foreseeable future.

Stock Advisor furnishes investors with a clear-cut roadmap for success, offering insights on portfolio development, regular analyst updates, and two fresh stock recommendations monthly. Since 2002, the Stock Advisor service has outperformed the S&P 500 returns by over threefold*.

Discover the top 10 stocks

*Stock Advisor returns as of February 20, 2024

Matt DiLallo holds positions in Chevron. The Motley Fool has stakes in and endorses Chevron and Enerplus. The Motley Fool suggests Occidental Petroleum and Pioneer Natural Resources. The Motley Fool follows a strict disclosure policy.

The expressed views and opinions in this piece are the author’s own and do not necessarily align with those of Nasdaq, Inc.