Warren Buffett’s investment prowess has long been the stuff of legends. His strategic move to accumulate shares in Apple for Berkshire Hathaway back in 2016 and 2017 has proven to be a financial juggernaut. Apple has blossomed into the conglomerate’s largest stock position, with the current stake valued at an impressive $175 billion. Share prices have surged over 500% since the inception of 2017, solidifying Apple as one of Buffett’s best investments. However, basking in past glory doesn’t guarantee future success.

An Apple a Day Doesn’t Guarantee Growth

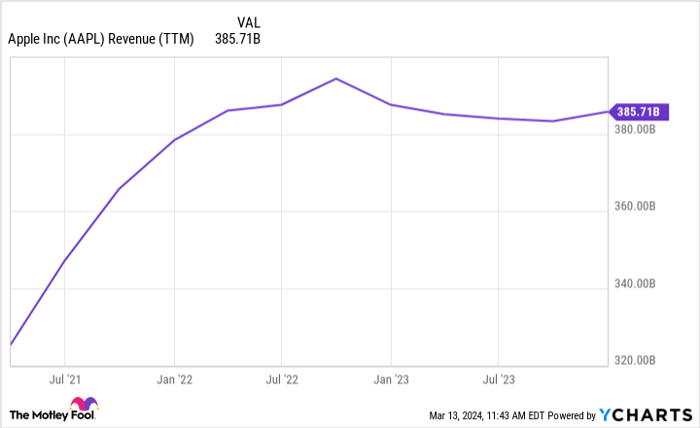

The revenue landscape at Apple is showing signs of stagnation. Despite the rampant inflation across the globe, Apple’s trailing-12-month revenue has dipped since mid-2022. Adjusted for inflation, this downturn is a hard pill for Apple to swallow. While the iPhone segment managed to notch up sales to $70 billion in fiscal Q1 of 2024, a jump from $66 billion the previous year, it remains the only hardware category witnessing growth. The era of meteoric iPhone sales growth seems to have reached its zenith.

Apple must now scout for a new catalyst to propel revenue. The Vision Pro mixed reality headset was supposed to be the harbinger of this growth. With a lofty price tag of $3,500, it was seen as a potential game-changer. Unfortunately, initial signs point to a flop. Dissatisfied buyers returning the device coupled with dwindling regular usage paint a bleak picture. For Apple to reignite sales growth, Vision Pro needs to become a global sensation. However, the path to this seems murky, with the current iteration far from replicating the iPhone’s success story.

Geopolitical Storm Clouds Gathering Over Cupertino

Apple’s woes don’t end at revenue stagnation. Regulatory thunderstorms loom large, threatening to upend some of the company’s cash cows. Take China’s clampdown on Apple products, for instance. With the Chinese government tightening the noose by expanding the iPhone ban across its agencies, Apple’s lucrative 17.4% sales slice from China faces jeopardy.

While some see solace in Apple’s robust services segment, recent assaults by authorities on the App Store have sent ripples of uncertainty. The E.U.’s hefty $2 billion fine on Apple for anti-competitive music streaming practices sets a daunting precedent. The 30% cut on digital transactions that oils Apple’s revenue wheels is also under governmental scrutiny globally.

A potentially catastrophic blow could arise from the mounting debate in U.S. courts over the annual $20 billion payment from Google to retain the default search engine spot on Apple devices. If deemed anti-competitive, this financial windfall could evaporate in a legal blink, ravaging Apple’s $118 billion in yearly operating earnings.

Not All That Glitters Is Gold: Unattractive Valuation

Glancing at Apple’s stock price reveals an unflattering valuation for a tepid-growth entity. With a trailing P/E ratio of 27, Apple stands at a premium to sprinting competitors like Alphabet, the Google Search parent. Moreover, this valuation snapshot fails to mirror the impending threats on the horizon – from China uncertainties to a Vision Pro fiasco and services revenue squeeze. When all these harbingers of trouble coalesce, Apple emerges as the shakiest runner among the Magnificent Seven stocks in 2024.

Are you contemplating a $1,000 plunge into Apple shares? Think again.

Before diving into the Apple stock pool, ponder this:

The Motley Fool Stock Advisor pros have unveiled their top picks for investors to dive into and guess what – Apple didn’t make the cut. These ten stocks are poised to churn out mammoth returns in the coming years.

Stock Advisor extends a ready-made roadmap to success, offering counsel on portfolio construction, regular analyst updates, and a fresh pair of stock picks monthly. Since 2002, the Stock Advisor has tripled the S&P 500 returns*.

Discover the top 10 stocks

*Stock Advisor returns as of March 11, 2024

Suzanne Frey, an executive at Alphabet, sits on The Motley Fool’s board of directors. Brett Schafer houses positions in Alphabet. The Motley Fool also boasts positions in and recommends Alphabet, Apple, and Berkshire Hathaway. The Motley Fool abides by a strict disclosure policy.

The opinions articulated herein are exclusively those of the author and might not align with Nasdaq, Inc.’s viewpoints.