“`html

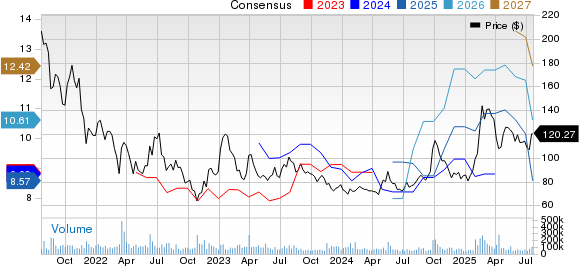

Alibaba Group reported a year-over-year revenue growth of 7% to RMB236.5 billion, but raised significant concerns over its financial health, particularly a free cash flow decline of 76% to RMB3.7 billion. The downward revision of the Zacks Consensus Estimate for fiscal 2026 earnings to $8.58 per share, an 18.1% reduction over the past month, signals market pessimism about Alibaba’s growth prospects.

The company’s deceleration in growth is evident as its overall revenue growth has slowed from historical double-digit rates, with competitive pressures from rivals like ByteDance and Tencent. Despite investments in artificial intelligence and cloud infrastructure, Alibaba’s performance in core segments like Taobao and Tmall has diminished, indicating a potential loss of market share. Furthermore, ongoing geopolitical tensions between the U.S. and China heighten risks for investors.

Amid these challenges, Alibaba’s current market valuation raises additional concerns, with results showing only 1.1% returns over the past three months. Given these factors, which include declining operational efficiency and substantial competition, analysts recommend avoiding Alibaba stock in 2025.

“`