“`html

Three Undervalued Stocks to Consider for Your Portfolio

Veteran investors recognize that the recent market weakness presents an opportunity rather than a threat. While stocks may not have reached their lowest point yet, they are likely closer to it than many think. In five years, the focus will be on the investment’s performance, not the precise moment of entry. This context sets the stage for a look at three stocks that have faced unwarranted declines. Each possesses its unique risk-reward profile, but all three could enhance any portfolio at their current prices.

Where to invest $1,000 right now? Our analyst team has identified the 10 best stocks to buy at this moment. Learn More »

In no particular order…

Image source: Getty Images.

1. Amazon

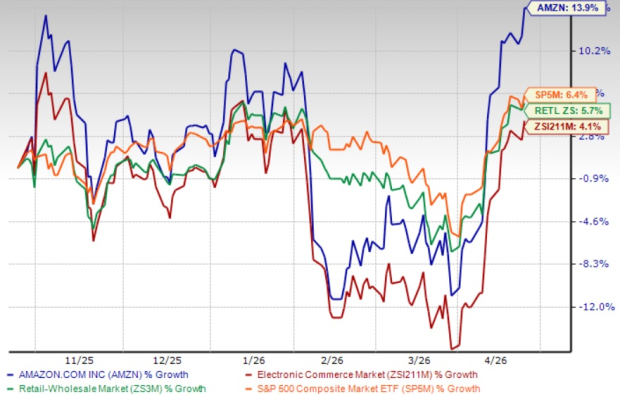

Amazon (NASDAQ: AMZN) reported better-than-expected first-quarter results, but its forward guidance disappointed investors. For the current quarter, the e-commerce giant anticipates revenue between $159 billion and $164 billion, which represents a 7% to 11% increase from the same quarter last year but falls short of the consensus estimate of $161.2 billion.

The expected operating income of $13 billion to $17.5 billion also did not meet the analysts’ average expectation of $17.6 billion, nor did it surpass last year’s figure of $14.7 billion. Performance from the crucial Amazon Web Services (AWS) segment also underwhelmed, leading to a dip in share prices.

However, it is important to maintain a broad perspective. Although guidance fell short, it still indicates growth, continuing a long-standing trend. Additionally, there is a strong argument that Amazon is managing expectations prudently.

Fundamentally, Amazon commands a significant presence in North America’s online marketplace, capturing nearly 40% of e-commerce sales. In comparison, Walmart holds a distant second place with just under 11% market share. The company’s dominance suggests that it will remain a formidable player in the space.

On the cloud computing front, while it faces competition from Microsoft and Alphabet, AWS still leads the market and continues to grow. According to Goldman Sachs, the global cloud services market is projected to expand at a 22% annual rate through 2030, benefiting Amazon’s most profitable segment.

In summary, despite a 20% drop in share prices leading up to the recent earnings report, Amazon shares have likely absorbed the worst of the declines without accounting for long-term potential. The current dip presents an advantageous long-term entry point for investors.

2. Iovance Biotherapeutics

Iovance Biotherapeutics (NASDAQ: IOVA) has a market cap of just over $1 billion, resulting in limited investor attention. However, its small size does not reflect its potential.

As a specialized biotech firm, Iovance primarily focuses on its flagship product, Amtagvi, which was approved early last year. The company also sells Proleukin, a drug designed to enhance Amtagvi’s efficacy.

Investing in a single-product company carries risk, yet Amtagvi holds promise as the world’s first tumor-infiltrating lymphocyte (TIL) treatment approved for certain skin cancers. The TIL market is expected to grow at an average annual rate of nearly 40% through 2032, while GlobalData projects that worldwide sales of Amtagvi could rise from $103.6 million last year to $1 billion by 2030.

Iovance is conducting multiple clinical trials to explore additional uses for Amtagvi. The stock has seen a decline of over 90% since its peak in early 2021, a common occurrence in the biotech sector after initial enthusiasm fades.

Nonetheless, the fundamentals are shifting; the company anticipates top-line growth of 176% this year and 66% next year, with plans to transition into profitability by 2027.

3. PepsiCo

Finally, consider PepsiCo (NASDAQ: PEP) in your investment strategy.

Interestingly, while Coca-Cola (NYSE: KO) has seen its shares reach record highs, PepsiCo’s stock is exploring new multiyear lows. This contrasting performance can be puzzling given the companies’ similar market positions.

“““html

PepsiCo Faces Stock Pressure Amid Earnings Guidance and Market Dynamics

PepsiCo’s recent stock struggles may be linked to its reduced earnings guidance for 2025, primarily due to tariff worries. However, it is essential to note that the stock’s decline began before these tariffs were introduced.

What accounts for this situation? The difference in investor perceptions of PepsiCo and Coca-Cola plays a significant role.

Although PepsiCo is a strong competitor, Coca-Cola has a more prominent brand presence. This allows Coca-Cola to effectively promote its diverse beverage range, including Gold Peak tea, Minute Maid juices, and Powerade sports drinks. Additionally, investors may view Coca-Cola’s reliance on third-party bottlers as a strategic advantage in today’s inflationary climate, contrasting with PepsiCo’s preference for in-house production.

Both companies’ operational structures have distinct advantages and drawbacks. Coca-Cola may find it challenging to handle cost-related pushbacks from its third-party bottlers in the future. Meanwhile, while maintaining its own production facilities can pressure PepsiCo’s profit margins, it allows the company complete control over its manufacturing processes. Should tariff-related challenges persist, this perceived weakness for PepsiCo could transform into a competitive benefit.

The distinctions between these business models are complex, with each possessing its nuances. Currently, the market may be overly favoring Coca-Cola’s strategy while underestimating PepsiCo’s long-term potential. This has resulted in PepsiCo’s forward-looking dividend yield rising to an attractive 4%, which is appealing for investors seeking solid returns among blue-chip stocks.

Investment Considerations

For investors contemplating how to allocate $1,000, expert insights can be valuable. Notably, Stock Advisor has achieved an impressive average return of 906%, significantly outperforming the S&P 500, which stands at 164%.

They recently disclosed their selections for the 10 best stocks to consider now, accessible to members joining Stock Advisor.

*Stock Advisor returns as of May 5, 2025

The views and opinions expressed herein belong to the author and do not necessarily reflect those of Nasdaq, Inc.

“`